Question: Second Round Electronics: A Case for Critical Thinking Nathalie Johnstone, Brandy Mackintosh, and Fred Phillips ABSTRACT: This instructional case requires students to provide advice to

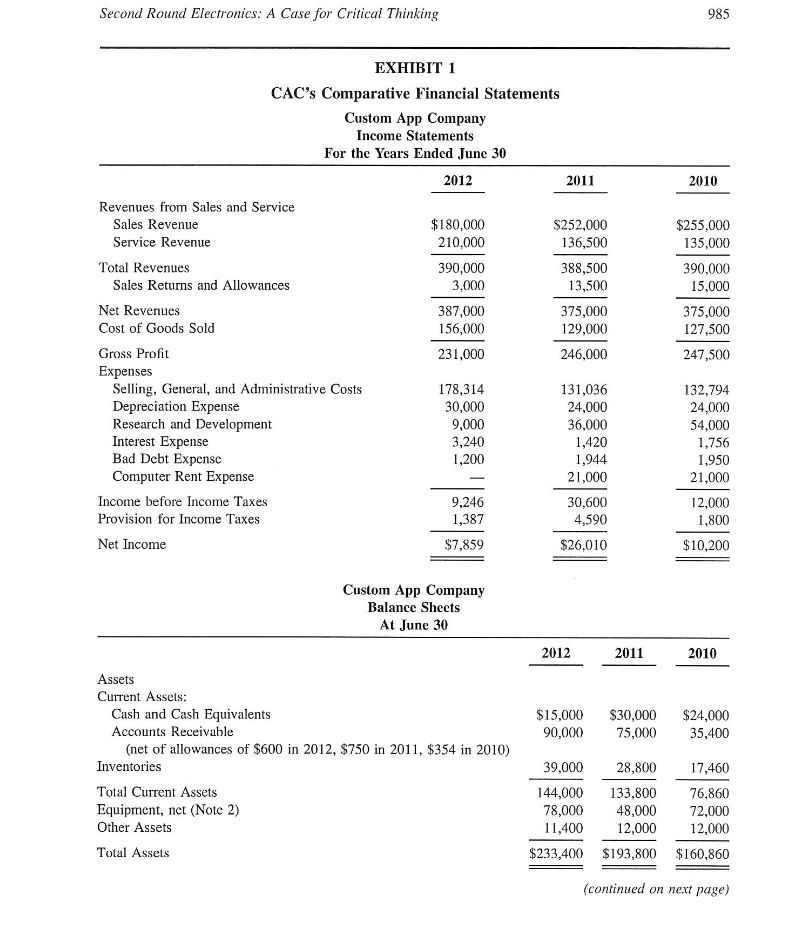

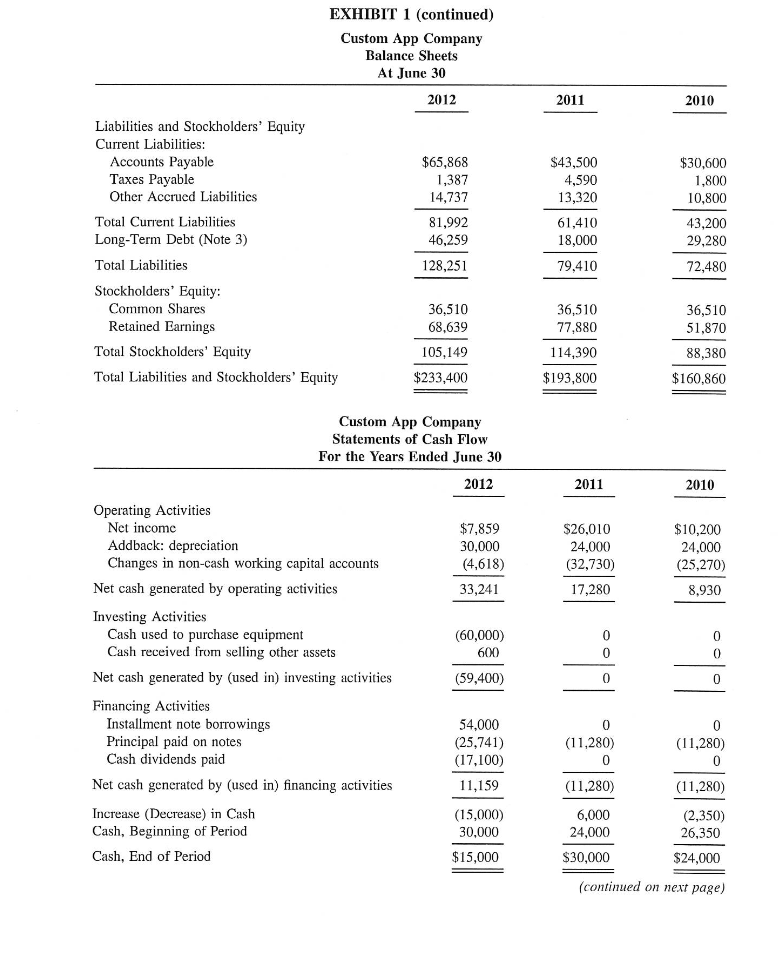

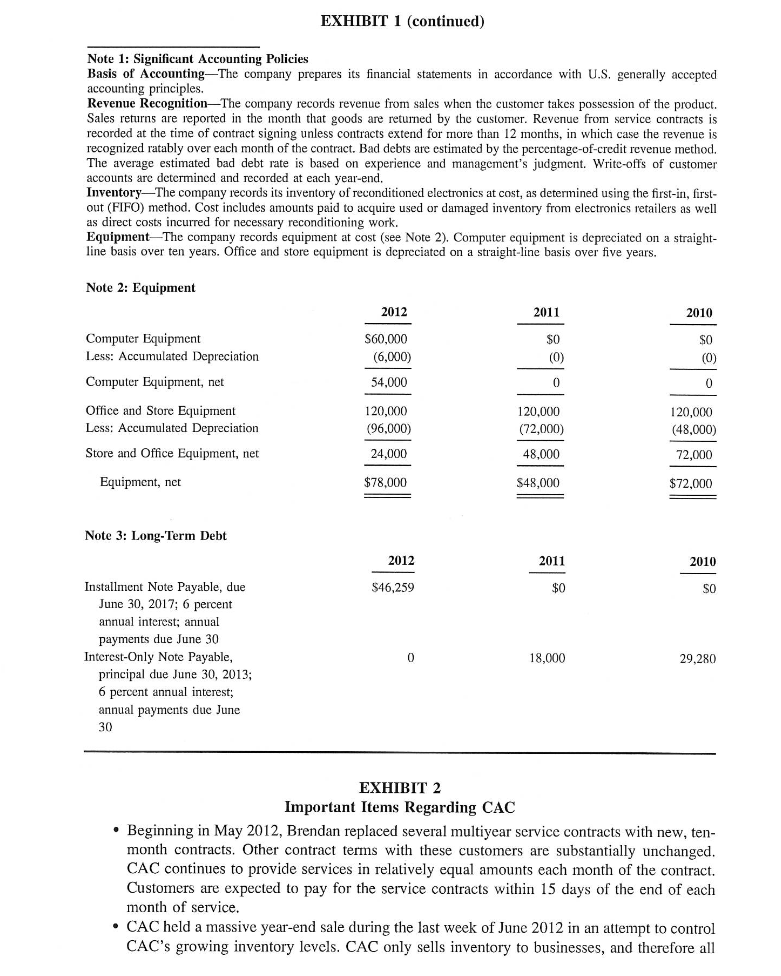

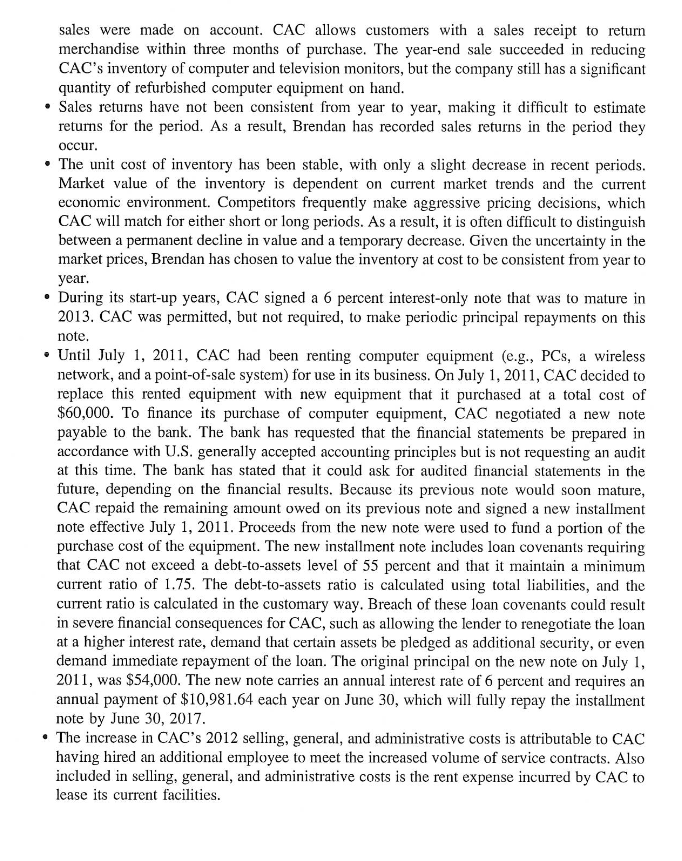

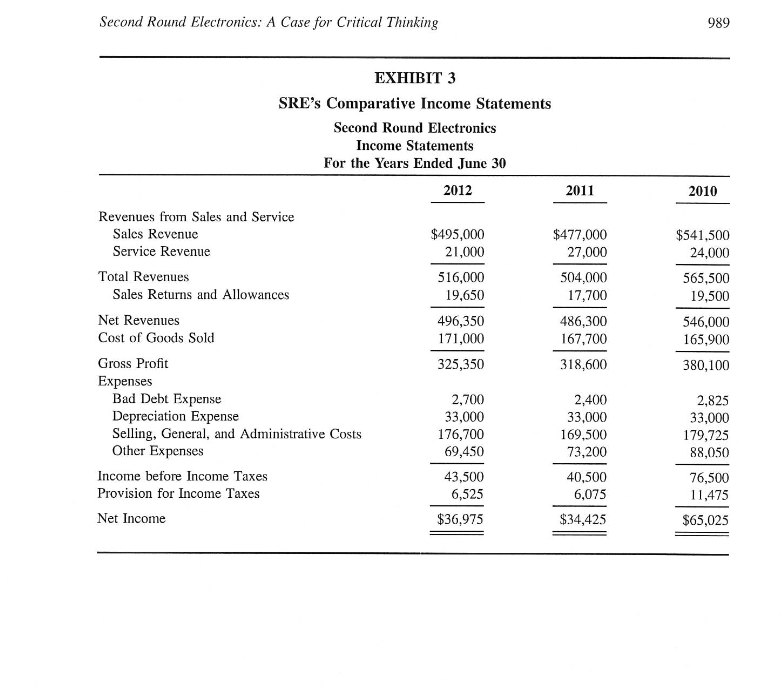

Second Round Electronics: A Case for Critical Thinking Nathalie Johnstone, Brandy Mackintosh, and Fred Phillips ABSTRACT: This instructional case requires students to provide advice to a client who is currently the sole owner of a for-profit company that reconditions and sells used electronics. The client is considering purchasing a similar company with the vision of expanding into the sales and service of emerging technologies. The target company's unaudited financial statements contain questionable accounting choices and judgments that appear to enable the company to meet external financial reporting constraints. In their role as financial advisers, students are expected to use critical thinking skills to identify and evaluate questionable choices in the target company's financial statements. This case is suitable for use in introductory and intermediate financial accounting as well as introductory auditing and assurance courses, and can be used as a context for in- class discussion, as a basis for exam questions, and/or as a writing assignment. Assessment rubrics and Teaching Notes accompany the case for use by instructors. Keywords: financial accounting; policy choices; loan covenants; ratio analysis. THE CASE S econd Round Electronics (SRE) is a privately owned company that reconditions and sells used consumer electronics. Its product offerings include home and car audio systems, televisions, and other devices with touch-sensitive monitors, such as smartphones and computer tablets. SRE's sole owner, Jeff Hasting, started the company 15 years ago after obtaining a degree in electronics repair at a local college. Jeff has been very happy with SRE's results to date. SRE has developed into a successful company with relatively stable profits and a solid financial condition. Jeff is a very competitive person, however, and he feels that SRE could be even more successful, so he would like to see his company expand into selling and servicing emerging technologies for corporate customers. Jeff has been working closely with Rachel Becker, SRE's controller, to explore opportunities for SRE to become a bigger player in the local electronics market and increase its profitability. An idea that they have been tossing around is to acquire a company that produces complementary technologies for SRE's products. Such an acquisition could lead to synergies that increase SRE's market presence and drive greater profitability. Jeff has asked you to analyze a company that he and Nathalie Johnstone and Brandy Mackintosh are Assistant Professors and Fred Phillips is a Professor, all at the University of Saskatchewan.Rachel believe could be a good acquisition. Jeff makes it clear that he does not want you to advise him on business strategy; that is something he prides himself on having well in hand. Rather, he wants from you an insightful, focused financial analysis of the potential acquisition target. Somewhat out of character, he quietly admits that he and Rachel "know SRE's accounting inside and out, but we're not that familiar with the accounting choices made by other companies and how it affects their financial results. We realize that accountants make all kinds of judgments and choices when preparing financial statements, and we would value your input on identifying and evaluating how these professional judgments may have affected the financial reporting for our target company. Our banker suggested that a financial due diligence report would help us to become aware of the financial risks that may exist at the potential acquisition target, and that is why we have asked for your assistance." Background Information on the Potential Acquisition Target The company at the top of Jeff and Rachel's potential acquisition list is Custom App Company (CAC). Like SRE, CAC operates in reconditioned electronics. But rather than focus on selling consumer products, CAC also provides corporate installation, training, and custom programming services. CAC is smaller than SRE, with only a few employees, but CAC is known for its innovative work. CAC is a private company, owned by Brendan Zamble. CAC neither is required to have an external audit nor does it make its financial statements readily available to outside users. CAC's only external financial statement users are the Internal Revenue Service and CAC's bank Jeff has been in discussions with Brendan, CAC's president, over the past year about a potential buyout, so he has obtained excerpts from CAC's financial statements for the years ended June 30, 2012, 2011, and 2010. Jeff and Rachel believe CAC offers the kind of performance that SRE could use to boost its own market presence and profits. Jeff has provided you with excerpts from CAC's financial statements (see Exhibit 1). He also has provided you with notes from his discussion with Brendan (see Exhibit 2). These notes convey information relevant to various accounting policy alternatives from which the management at CAC has adopted the specific accounting policies described in the notes to the financial statements. At the risk of overloading you with information, Jeff also gives you a copy of SRE's income statements (see Exhibit 3) to use as a benchmark when evaluating CAC. Although CAC has been in business for only five years, it has reported good growth in net revenues, with better growth than SRE in 2012. Your Task SRE's executives, Jeff Hasting and Rachel Becker, realize that acquiring another company is a complex process that requires careful decision-making and analysis. Anticipating that Mr. Zamble may be overly optimistic when judging the value of his company and the strength of its financial position, Mr. Hasting and Ms. Becker have asked you to prepare a financial due diligence report that analyzes the financial situation at Custom App Company (CAC). To ensure that Mr. Hasting and Ms. Becker understand the scope of this work, you clarify that due diligence does not involve a formal audit. Rather, the focus of your work and your report will be on identifying and explaining in detail key financial concerns that Mr. Hasting and Ms. Becker should be aware of before proceeding with acquisition negotiations. This focus will lead you to evaluate the appropriateness of CAC's accounting policies and identify any observations that suggest CAC's policies may not best portray the company's financial condition. Finally, you will raise in your report any imminent concerns about CAC's financial condition that arise from CAC's accounting policy choices, including any consequences that would arise if CAC were to make alternative accounting choices. You reiterate that your report will not provide a generic financial statement analysis but instead will focus on evaluating CAC's specific accounting choices and judgments. Mr. Hasting and Ms. Becker agree to these terms, so you begin to analyze the information available to you.Second Round Electronics: A Case for Critical Thinking 985 EXHIBIT 1 CAC's Comparative Financial Statements Custom App Company Income Statements For the Years Ended June 30 2012 2011 2010 Revenues from Sales and Service Sales Revenue $180,000 $252,000 $255,000 Service Revenue 210,000 136,500 135,000 Total Revenues 390,000 388,500 390,000 Sales Returns and Allowances 3.000 13,500 15.000 Net Revenues 387,000 375,000 375,000 Cost of Goods Sold 156,000 129,000 127,500 Gross Profit 231,000 246,000 247,500 Expenses Selling, General, and Administrative Costs 178,314 131,036 132,794 Depreciation Expense 30,000 24,000 24,000 Research and Development 9,000 36,000 54,000 Interest Expense 3,240 1,420 1,756 Bad Debt Expense 1,200 1,944 1,950 Computer Rent Expense 21,000 21,000 Income before Income Taxes 9,246 30,600 12,000 Provision for Income Taxes 1,387 4,590 1,800 Net Income $7,859 $26,010 $10,200 Custom App Company Balance Sheets At June 30 2012 2011 2010 Assets Current Assets: Cash and Cash Equivalents $15,000 $30,000 $24,000 Accounts Receivable 90,000 75,000 35,400 (net of allowances of $600 in 2012, $750 in 2011, $354 in 2010) Inventories 39,000 28,800 17,460 Total Current Assets 144,000 133,800 76,860 Equipment, net (Note 2) 78,000 48,000 72,000 Other Assets 11.400 12,000 12,000 Total Assets $233,400 $193,800 $160,860 continued on next page)EXHIBIT 1 [continued] Custom App Company Balance Sheets At June 30 2013 201] 3010 Liabilities and Stockltolders' Equity Current Liabilities: Accounts Payable $65,363 $43,500 $30,600 Taxes Payable 1.33?r 4,590 1.300 Other Accrued Liabilities 10.337Ir 13.320 10,300 Total Cunent Liabilities 31.992 61.410 43.200 LongvTerm Debt (Note 3} 46.259 13,000 29.230 Total Liabilities 123.251 "19,410 "12.430 Stockholders' Equity: Common Shares 36.510 36.510 36,510 Retained Earnings 68.639 31.330 51.330 Total Stockholders' Equity 105.149 114.390 38,330 Total Liabilities and Stockholders' Equity $233,400 0193.300 $160,360 Custom App Company Statements of Cash Flou-r For the Years Ended June 30' 2012 2011 2010 Operating Activities Net income 61.659 326.010 $10,200 Addbaclt: depreciation 30.000 24.000 24,000 Changes in non-cash working capital accounts (4.613] [32,130] {25.210} Net cash generated by operating activities 33,241 13,230 3,930 Investing Activities Cash used to purchase equipment (60,000} 0 0 Cash received from selling other assets 600 0 0 Net cash generated by [used in} investing activities {59.400} 0 0 Financing Activities Installment note bon'owings 54.000 0 0 Principal paid on notes {25.141} {11.230} {11,230} Cash dividends paid (11100} 0 0 Net cash generated by [used in} nancing activities 11.159 {11.230} [11.2303 lite-tease {Dementia} in Cash [15.000] 0.000 (2,350) Cash. Beginning of Period 30.000 24.000 26.350 Cash. End of Period $15,000 $30,000 $24,000 {remained on next page) EXHIBIT 1 (continued) Note 1: Significant Accounting Policies Basis of Accounting-The company prepares its financial statements in accordance with U.S. generally accepted accounting principles Revenue Recognition-The company records revenue from sales when the customer takes possession of the product. Sales returns are reported in the month that goods are returned by the customer. Revenue from service contracts is recorded at the time of contract signing unless contracts extend for more than 12 months, in which case the revenue is recognized ratably over each month of the contract. Bad debts are estimated by the percentage-of-credit revenue method. The average estimated bad debt rate is based on experience and management's judgment. Write-offs of customer accounts are determined and recorded at each year-end. Inventory-The company records its inventory of reconditioned electronics at cost, as determined using the first-in, first- out (FIFO) method. Cost includes amounts paid to acquire used or damaged inventory from electronics retailers as well as direct costs incurred for necessary reconditioning work. Equipment-The company records equipment at cost (see Note 2). Computer equipment is depreciated on a straight- line basis over ten years. Office and store equipment is depreciated on a straight-line basis over five years. Note 2: Equipment 2012 2011 2010 Computer Equipment $60,000 $0 $0 Less: Accumulated Depreciation (6,000) (0) (0) Computer Equipment, net 54,000 0 0 Office and Store Equipment 120,000 120,000 120,000 Less: Accumulated Depreciation (96,000) (72,000) (48,000) Store and Office Equipment, net 24,000 48,000 72,000 Equipment, net $78,000 $48,000 $72,000 Note 3: Long-Term Debt 2012 2011 2010 Installment Note Payable, due $46,259 $0 June 30, 2017; 6 percent annual interest; annual payments due June 30 Interest-Only Note Payable, 0 18,000 29,280 principal due June 30, 2013; 6 percent annual interest; annual payments due June 30 EXHIBIT 2 Important Items Regarding CAC . Beginning in May 2012, Brendan replaced several multiyear service contracts with new, ten- month contracts. Other contract terms with these customers are substantially unchanged. CAC continues to provide services in relatively equal amounts each month of the contract. Customers are expected to pay for the service contracts within 15 days of the end of each month of service. CAC held a massive year-end sale during the last week of June 2012 in an attempt to control CAC's growing inventory levels. CAC only sells inventory to businesses, and therefore allsales were made on account. CAC allows customers with a sales receipt to return merchandise within three months of purchase. The year-end sale succeeded in reducing Q3105; inventory oF computer and television monitors, but the company still has a signicant quantity of refurbished computer equipment on hand. Sales returns have not been consistent from year to year, making it difcult to estimate returns for the period. As a result, Brendan has recorded sales returns in the period they occur. The unit cost of inventory has been stable, with only a slight decrease in recent periods, Market value of the inventory is dependent on current market trends and the current economic environment. Competitors frequently make aggressive pricing decisions. which CAC will match for either short or long periods. As a result, it is often difcult to distinguish between a permanent decline in value and a temporary decrease. Given the uncertainty in the market prices, Brendan has chosen to value the inventory at cost to be consistent from year to year. During its start-up years, CAC signed a a percent interest-only note that was to mature in 21013. CAC was permitted, but not required, to make periodic principal repayments on this note. Until July 1, Ell. CAD had been renting computer equipment (o.g., PCs, a wireless network, and a pointof-sale system) for use in its business. On July 1. Bill 1, CHE decided to replace this rented equipment with new equipment that it purchased at a total cost of $6,. To nance its purchase of computer equipment, can: negotiated a new note payable to the bank. The hank has requested that the nancial statements he prepared in accordance with 11.3. generally accepted accounting principles but is not requesting an audit at this time. The bank has stated that it could aslr. for audited nancial statements in the future, depending on the nancial results. Because its previous note would soon mature, CAC repaid the remaining amount owed on its previous note and signed a new installment note effective July 1, 2011. Proceeds from the new note were used to fund a portion of the purchase cost of the equipment. The new installment note includes loan covenants requiring that {SAC not exceed a debtto-assets level of 55 percent and that it maintain a minimum current ratio of LTS. The debt-to-assets ratio is calculated using total liabilities, and the current ratio is calculated in the customary way. Breach of these loan covenants could result in severe nancial consequences for GAE, such as allowing the lender to renegotiate the loan at a higher interest rate, demand that certain assets be pledged as additional security, or even demand immediate repayment of the loan. The original principal on the new note on July I, 2311, was $54,El. The new note carries an annual interest rate of 6 percent and requires an annual payment of $l,981.4 each year on June 3B, which will fully repay the installment note by June 3U, EDIT. The increase in CAC's EDIE selling, general. and administrative costs is attributable to CAC having hired an additional employee to meet the increased volume of service contracts. Also included in selling, genera], and administrative costs is the rent expense incurred by CAC to lease its current facilities. Second Round Electronics: A Case for Critical Thinking 989 EXHIBIT 3 SRE's Comparative Income Statements Second Round Electronics Income Statements For the Years Ended June 30 2012 2011 2010 Revenues from Sales and Service Sales Revenue $495,000 $477,000 $541,500 Service Revenue 21,000 27,000 24,000 Total Revenues 516,000 504,000 565,500 Sales Returns and Allowances 19,650 17,700 19,500 Net Revenues 496,350 486,300 546,000 Cost of Goods Sold 171,000 167,700 165,900 Gross Profit 325,350 318,600 380,100 Expenses Bad Debt Expense 2,700 2,400 2,825 Depreciation Expense 33,000 33,000 33,000 Selling, General, and Administrative Costs 176,700 169,500 179,725 Other Expenses 69,450 73,200 88,050 Income before Income Taxes 43,500 40,500 76,500 Provision for Income Taxes 6,525 6,075 11,475 Net Income $36,975 $34,425 $65,025

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!