Question: second year auditing Background information - Q1 You are a final-year registered candidate auditor at Zolani Paulina and Khabzela Inc (ZPK), a Johannesburg-based firm of

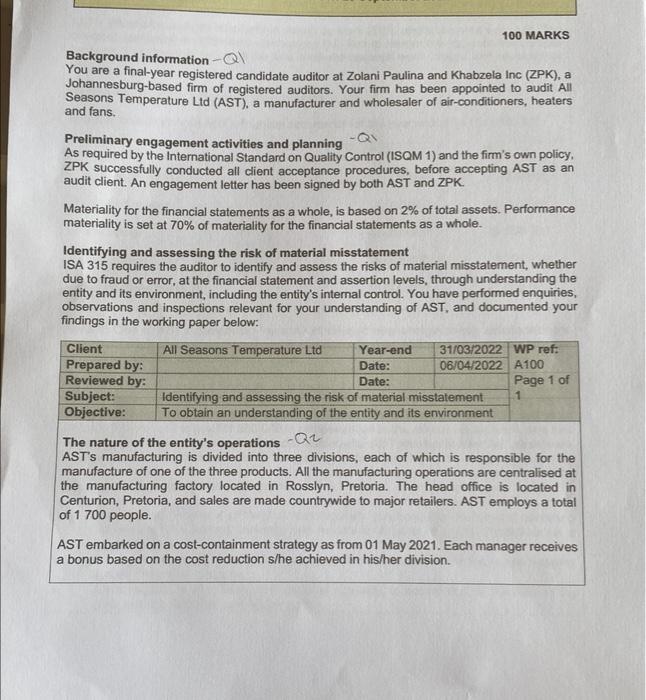

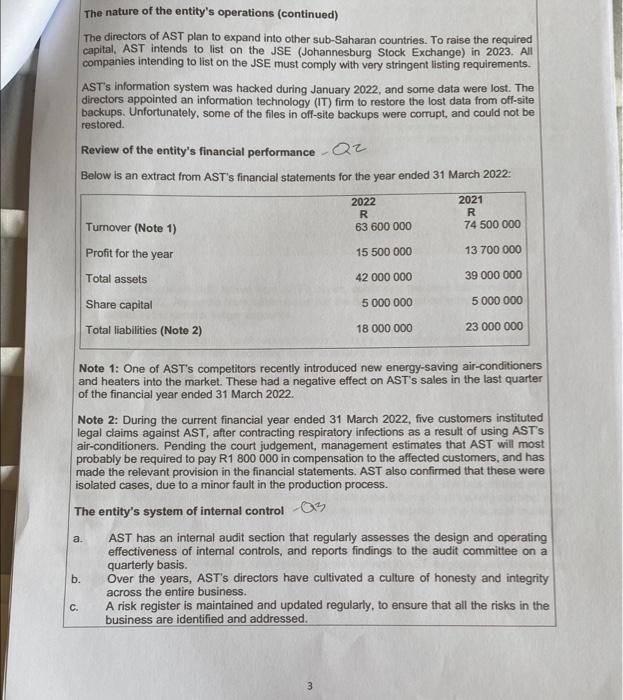

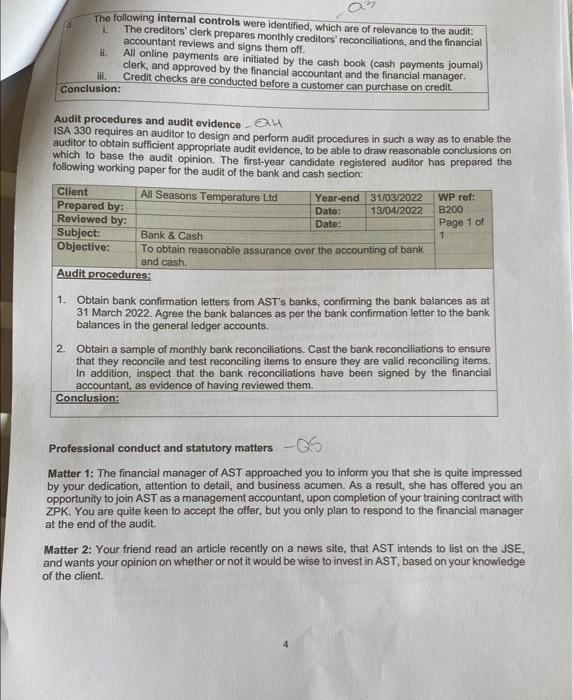

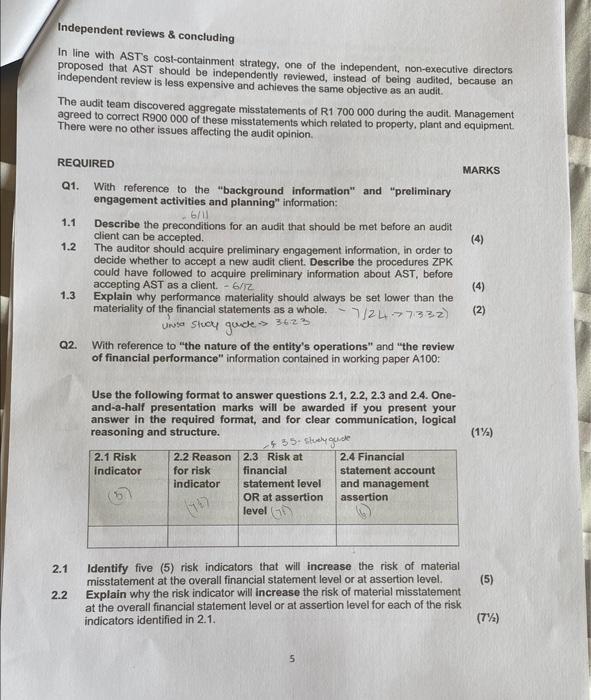

Background information - Q1 You are a final-year registered candidate auditor at Zolani Paulina and Khabzela Inc (ZPK), a Johannesburg-based firm of registered auditors. Your firm has been appointed to audit All Seasons Temperature Ltd (AST), a manufacturer and wholesaler of air-conditioners, heaters and fans. Preliminary engagement activities and planning Q1 As required by the International Standard on Quality Control (ISQM 1) and the firm's own policy. ZPK successfully conducted all client acceptance procedures, before accepting AST as an audit client. An engagement letter has been signed by both AST and ZPK. Materiality for the financial statements as a whole, is based on 2% of total assets. Performance materiality is set at 70% of materiality for the financial statements as a whole. Identifying and assessing the risk of material misstatement ISA 315 requires the auditor to identify and assess the risks of material misstatement, whether due to fraud or error, at the financial statement and assertion levels, through understanding the entity and its environment, including the entity's internal control. You have performed enquiries, observations and inspections relevant for your understanding of AST, and documented your findings in the working paper below: The nature of the entity's operations Q2 AST's manufacturing is divided into three divisions, each of which is responsible for the manufacture of one of the three products. All the manufacturing operations are centralised at the manufacturing factory located in Rosslyn. Pretoria. The head office is located in Centurion, Pretoria, and sales are made countrywide to major retailers. AST employs a total of 1700 people. AST embarked on a cost-containment strategy as from 01 May 2021. Each manager receives a bonus based on the cost reduction s/he achieved in his/her division. The nature of the entity's operations (continued) The directors of AST plan to expand into other sub-Saharan countries. To raise the required capital, AST intends to list on the JSE (Johannesburg Stock. Exchange) in 2023. All companies intending to list on the JSE must comply with very stringent listing requirements. AST's information system was hacked during January 2022, and some data were lost. The directors appointed an information technology (IT) firm to restore the lost data from off-site backups. Unfortunately, some of the files in off-site backups were comupt, and could not be restored. Review of the entity's financial performance 2 Below is an extract from AST's financial statements for the year ended 31 March 2022: Note 1: One of AST's competitors recently introduced new energy-saving air-conditioners and heaters into the market. These had a negative effect on AST's sales in the last quarter of the financial year ended 31 March 2022 . Note 2: During the current financial year ended 31 March 2022, five customers instituted legal claims against AST, after contracting respiratory infections as a result of using AST's air-conditioners. Pending the court judgement, management estimates that AST will most probably be required to pay R1 800000 in compensation to the affected customers, and has made the relevant provision in the financial statements. AST also confirmed that these were isolated cases, due to a minor fault in the production process. The entity's system of internal control O47 a. AST has an intemal audit section that regularly assesses the design and operating effectiveness of intemal controls, and reports findings to the audit committee on a quarterly basis. b. Over the years, AST's directors have cultivated a culture of honesty and integrity across the entire business. c. A risk register is maintained and updated regularly, to ensure that all the risks in the business are identified and addressed. The following internal controls were identified, which are of relevance to the audit: 1. The creditors' clerk prepares monthly creditors' reconciliations, and the financial accountant reviews and signs them off. ii. All online payments are initiated by the cash book (cash payments joumal) clerk, and approved by the financial accountant and the financial manager. iii. Credit checks are conducted before a customer can purchase on credit. Conclusion: Audit procedures and audit evidence - 84 ISA 330 requires an auditor to design and perform audit procedures in such a way as to enable the auditor to obtain sufficient appropriate audit evidence, to be able to draw reasonable conclusions on which to base the audit opinion. The first-year candidate registered auditor has prepared the following working paper for the audit of the bank and cash section: 1. Obtain bank confirmation letters from AST's banks, confirming the bank balances as at 31 March 2022. Agree the bank balances as per the bank confirmation letter to the bank balances in the general ledger accounts. 2. Obtain a sample of monthly bank reconciliations. Cast the bank reconciliations to ensure that they reconcile and test reconciling items to ensure they are valid reconciling items. In addition, inspect that the bank reconciliations have been signed by the financial accountant, as evidence of having reviewed them. Conclusion: Professional conduct and statutory matters Matter 1: The financial manager of AST approached you to inform you that she is quite impressed by your dedication, attention to detail, and business acumen. As a result, she has offered you an opportunity to join AST as a management accountant, upon completion of your training contract with ZPK. You are quite keen to accept the offer, but you only plan to respond to the financial manager at the end of the audit. Matter 2: Your friend read an article recently on a news site, that AST intends to list on the JSE, and wants your opinion on whether or not it would be wise to invest in AST, based on your knowledge of the client. Independent reviews \& concluding In line with AST's cost-containment strategy, one of the independent, non-executive directors proposed that AST should be independently reviewed, instead of being audited, because an independent review is less expensive and achieves the same objective as an audit. The audit team discovered aggregate misstatements of R1 700000 during the audit. Management agreed to correct R900 000 of these misstatements which related to property, plant and equipment. There were no other issues affecting the audit opinion. REQUIRED MARKS Q1. With reference to the "background information" and "preliminary engagement activities and planning" information: 1.1 Describe the preconditions for an audit that should be met before an audit client can be accepted. 1.2 The auditor should acquire preliminary engagement information, in order to decide whether to accept a new audit client. Describe the procedures ZPK could have followed to acquire preliminary information about AST, before accepting AST as a client. - 6rr 1.3 Explain why performance materiality should always be set lower than the materiality of the financial statements as a whole. 7/2L73322) Q2. With reference to "the nature of the entity's operations" and "the review of financial performance" information contained in working paper A100: Use the following format to answer questions 2.1, 2.2, 2.3 and 2.4. Oneand-a-half presentation marks will be awarded if you present your answer in the required format, and for clear communication, logical reasoning and structure. 2.1 Identify five (5) risk indicators that will increase the risk of material misstatement at the overall financial statement level or at assertion level. 2.2 Explain why the risk indicator will increase the risk of material misstatement at the overall financial statement level or at assertion level for each of the risk indicators identified in 2.1. (7/2) 5 2.3 Indicate, for each risk indicator identified in 2.1, whether the risk pertains to a risk of material misstatement at financial statement level OR a risk of material misstatement at assertion level. 2.4 Indicate, for each of the risk indicators pertaining to a risk of material misstatement at assertion level, the relevant financial statement account AND management assertion affected. You should indicate "Not Applicable" for risks of material misstatements at financiai statement level. Q3. With reference to the information under "entity's system of internal control contained in working paper A100; 3.1 For each of the control aspects described in a-d, indicate the component of the system of internal control that is applicable. 3.2 Use the following format to answer question 3.2. One-and-a-half presentation marks will be awarded if the solution is presented in the required format, as well as for clear communication, logical reasoning and structure. 4.1 For each of the audit procedures (1-2) relating to bank and cash, indicate whether the procedure is a test of control or a substantive procedure. 4.2 For each of the audit procedures (12) relating to bank and cash, indicate (3) which management assertion(s) will be addressed by the audit procedure. Note that each procedure could address more than one management assertion. Q5. For each of Matter 1 and Matter 2 under "professional conduct and statutory matters" information: Use the following format to answer questions 5.1, 5.2 and 5.3. One-and-a-half presentation marks will be awarded if the solution is presented in the required format, as well as for communication, logical reasoning and structure. (1%) 5.1 Identify the type of threat to the fundamental principles of the SAICA Code of Professional Conduct. 5.2 Identify the fundamental principle(s) being threatened. (3) (3) 5.3 Provide a possible safeguard to eliminate or reduce the threat to an acceptable level. (3) Q6. With reference to the "independent reviews and concluding" information: 6.1 Discuss whether or not you agree with the proposal put forward by the nonexecutive director, and provide reasons to motivate your answer. 6.2 Evaluate the effect of the uncorrected misstatements and conclude whether or not the uncorrected misstatements should be regarded as material. Also indicate whether ZPK can issue an unmodified audit opinion

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts