Question: Section 1 Problem-solving 1. Suppose you are a portfolio manager using the capital asset pricing model for making recommendations to her clients. You have the

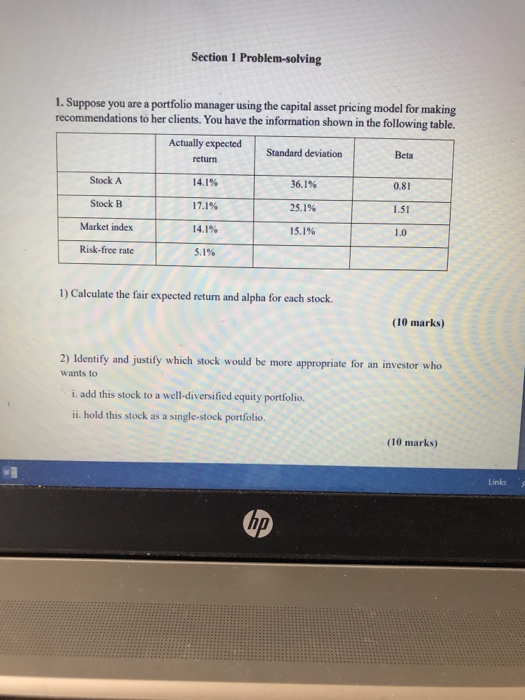

Section 1 Problem-solving 1. Suppose you are a portfolio manager using the capital asset pricing model for making recommendations to her clients. You have the information shown in the following table. Actually expected Standard deviation Beta 0.81 1.51 1.0 return Stock A Stock B Market index Risk-free rate 36. 196 25.1% 15.1% 14.1% 14.1% 5.1% 1) Calculate the fair expected return and alpha for each stock. (10 marks) 2) Identify and justify which stock would be more appropriate for an investor who wants to i. add this stock to a well-diversified equity portfolio. ii. hold this stock as a single-stock portfolio. (10 marks) Links 5 hp

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock