Question: Section 2. Interest Rate Risk Hedging (10 points) A manager of Belleville Bank is trying to make a decision to hedge its interest rate risk

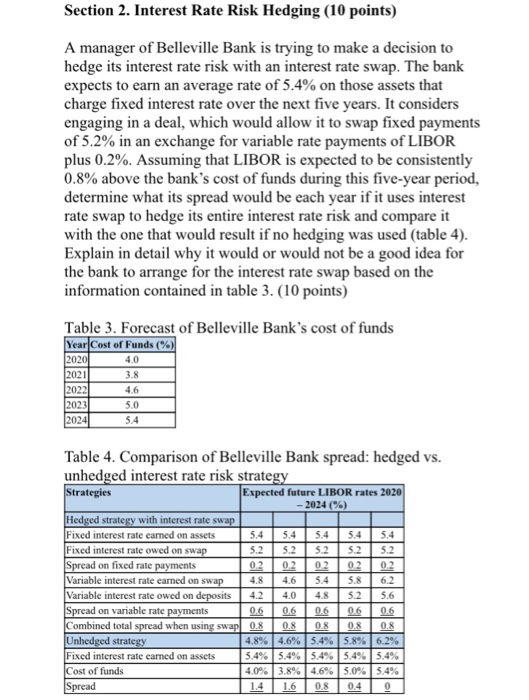

Section 2. Interest Rate Risk Hedging (10 points) A manager of Belleville Bank is trying to make a decision to hedge its interest rate risk with an interest rate swap. The banlk expects to earn an average rate of 5.4% on those assets that charge fixed interest rate over the next five years. It considers engaging in a deal, which would allow it to swap fixed payments of 5.2% in an exchange for variable rate payments of LIBOR plus 0.2%. Assuming that LIBOR is expected to be consistently 0.8% above the bank's cost of funds during this five-year period. determine what its spread would be each year if it uses interest rate swap to hedge its entire interest rate risk and compare it with the one that would result if no hedging was used (table 4) Explain in detail why it would or would not be a good idea for the bank to arrange for the interest rate swap based on the information contained in table 3.(10 points) Table 3. Forecast of Belleville Bank's cost of funds Year Cost of Funds (%) 4.0 4.6 5.0 20 Table 4. Comparison of Belleville Bank spread: hedged vs. unhedged interest rate risk strate Expected future LIBOR rates 2020 -2024 (%) with interest rate sw Fixed interest rate earned on assets Fixed interest rate owed on sw 5.4 54 54 54 5.4 5.2 5.2 5.2 52 5.2 02 0.2 02 02 0.2 4.8 4.6 54 5.8 6.2 4.2 4.0 4.8 5.2 5.6 06 | 06 | 06 | 06 06 0.8 0.8 0.8 0.8 0.8 4.8% 4.6% 5.4% 5.8% 6.2% on fixed rate Variable interest rate earned on s Variable interest rate owed on ad on variable rate payments ombined total nhed ixed interest rate earned on assets ost of funds when usi ead

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts