Question: Section 2 - Multiple choice based question. Question #2 (0.5 mark each) 1. The gross profit margin earned on an item which cost $1,000

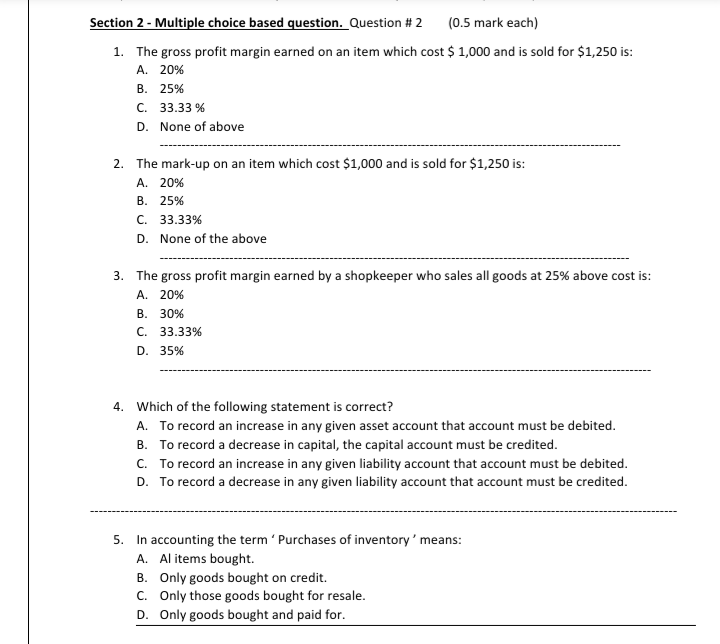

Section 2 - Multiple choice based question. Question #2 (0.5 mark each) 1. The gross profit margin earned on an item which cost $1,000 and is sold for $1,250 is: A. 20% B. 25% C. 33.33% D. None of above 2. The mark-up on an item which cost $1,000 and is sold for $1,250 is: A. 20% B. 25% C. 33.33% D. None of the above 3. The gross profit margin earned by a shopkeeper who sales all goods at 25% above cost is: A. 20% B. 30% C. 33.33% D. 35% 4. Which of the following statement is correct? A. To record an increase in any given asset account that account must be debited. B. To record a decrease in capital, the capital account must be credited. C. To record an increase in any given liability account that account must be debited. D. To record a decrease in any given liability account that account must be credited. 5. In accounting the term 'Purchases of inventory' means: A. Al items bought. B. Only goods bought on credit. C. Only those goods bought for resale. D. Only goods bought and paid for.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts