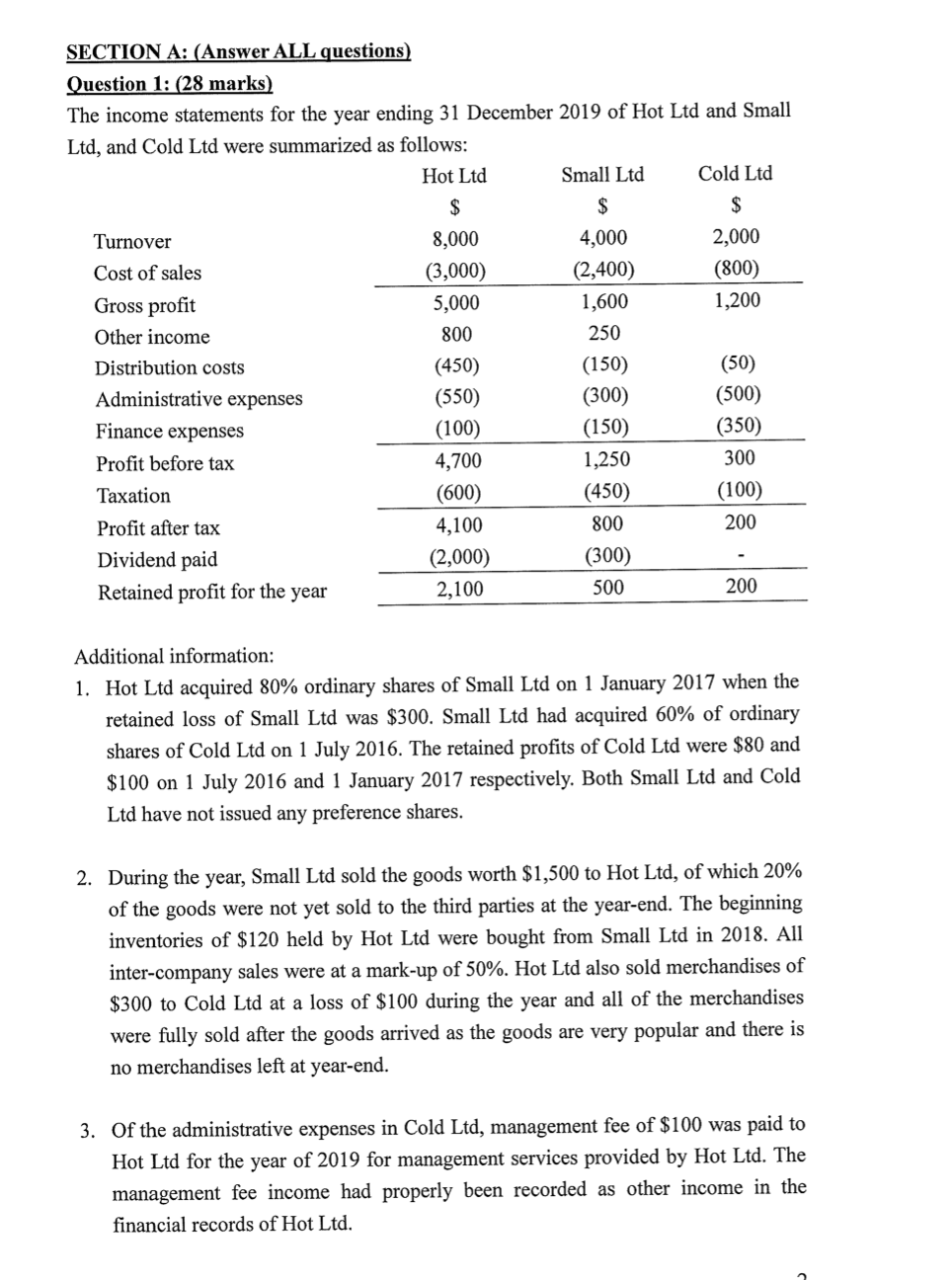

Question: SECTION A: (Answer ALL questions) Question 1: (28 marks) The income statements for the year ending 31 December 2019 of Hot Ltd and Small Ltd,

SECTION A: (Answer ALL questions) Question 1: (28 marks) The income statements for the year ending 31 December 2019 of Hot Ltd and Small Ltd, and Cold Ltd were summarized as follows: Hot Ltd Small Ltd Cold Ltd $ $ $ Turnover 8,000 4,000 2,000 Cost of sales (3,000) (2,400) (800) Gross profit 5,000 1,600 1,200 Other income 800 250 Distribution costs (450) (150) Administrative expenses (550) (300) (500) Finance expenses (100) (150) (350) Profit before tax 4,700 1,250 300 Taxation (600) (450) (100) Profit after tax 4,100 800 200 Dividend paid (2,000) (300) Retained profit for the year 2,100 500 200 (50) Additional information: 1. Hot Ltd acquired 80% ordinary shares of Small Ltd on 1 January 2017 when the retained loss of Small Ltd was $300. Small Ltd had acquired 60% of ordinary shares of Cold Ltd on 1 July 2016. The retained profits of Cold Ltd were $80 and $100 on 1 July 2016 and 1 January 2017 respectively. Both Small Ltd and Cold Ltd have not issued any preference shares. 2. During the year, Small Ltd sold the goods worth $1,500 to Hot Ltd, of which 20% of the goods were not yet sold to the third parties at the year-end. The beginning inventories of $120 held by Hot Ltd were bought from Small Ltd in 2018. All inter-company sales were at a mark-up of 50%. Hot Ltd also sold merchandises of $300 to Cold Ltd at a loss of $100 during the year and all of the merchandises were fully sold after the goods arrived as the goods are very popular and there is no merchandises left at year-end. 3. Of the administrative expenses in Cold Ltd, management fee of $100 was paid to Hot Ltd for the year of 2019 for management services provided by Hot Ltd. The management fee income had properly been recorded as other income in the financial records of Hot Ltd. 4. On 1 January 2018, in order to transfer more profit to Small Ltd, Hot Ltd sold a machine for administrative purpose costing $1,500 to Small Ltd for $1,020 and the machine is to be used by Small Ltd for 6 years with zero residual value. Small Ltd provides the depreciation using a straight-line method. 5. The dividend paid of Small Ltd during the year was out of the profit for 2017. Hot Ltd recorded it under the heading of Other income. 6. The non-controlling interest was stated at fair value of the acquisition date. The total goodwill of Small Ltd at 1 January 2017 was $3,000 and the goodwill of Small Ltd of subsequent years were: 31 December 2017 $2,400 31 December 2018 $2,500 31 December 2019 $2,000 7. There was no impairment for goodwill of Cold Ltd since its acquisition. 8. On 1 January 2017, the fair value of depreciable non-current assets used for "distribution purpose of Small Ltd exceeded the carrying amount of those assets by $2,000. The remaining useful life remained unchanged at 10 years. Small Ltd has not recorded such adjustment in its book and record. You can assume that the book value of other net assets was equal to the fair value of those assets at the date of acquisition 9. The retained profits of Hot Ltd, Small Ltd, and Cold Ltd at 1 January 2019 were $5,800, $1,200, and $300 respectively. Required: a. Prepare the consolidated income statement of Hot Ltd and its subsidiaries for the year ended 31 December 2019 on the assumption that both Small and Cold Ltd are controlled by Hot Ltd directly and indirectly. (16 marks) b. Prepare the statement of retained profit of the Hot Ltd's company shareholders (i.e. retained profit attributable to parent company's shareholders) (12 marks) Note: All working must be shown. No marks can be given without details if the final figures are wrong. 3 SECTION A: (Answer ALL questions) Question 1: (28 marks) The income statements for the year ending 31 December 2019 of Hot Ltd and Small Ltd, and Cold Ltd were summarized as follows: Hot Ltd Small Ltd Cold Ltd $ $ $ Turnover 8,000 4,000 2,000 Cost of sales (3,000) (2,400) (800) Gross profit 5,000 1,600 1,200 Other income 800 250 Distribution costs (450) (150) Administrative expenses (550) (300) (500) Finance expenses (100) (150) (350) Profit before tax 4,700 1,250 300 Taxation (600) (450) (100) Profit after tax 4,100 800 200 Dividend paid (2,000) (300) Retained profit for the year 2,100 500 200 (50) Additional information: 1. Hot Ltd acquired 80% ordinary shares of Small Ltd on 1 January 2017 when the retained loss of Small Ltd was $300. Small Ltd had acquired 60% of ordinary shares of Cold Ltd on 1 July 2016. The retained profits of Cold Ltd were $80 and $100 on 1 July 2016 and 1 January 2017 respectively. Both Small Ltd and Cold Ltd have not issued any preference shares. 2. During the year, Small Ltd sold the goods worth $1,500 to Hot Ltd, of which 20% of the goods were not yet sold to the third parties at the year-end. The beginning inventories of $120 held by Hot Ltd were bought from Small Ltd in 2018. All inter-company sales were at a mark-up of 50%. Hot Ltd also sold merchandises of $300 to Cold Ltd at a loss of $100 during the year and all of the merchandises were fully sold after the goods arrived as the goods are very popular and there is no merchandises left at year-end. 3. Of the administrative expenses in Cold Ltd, management fee of $100 was paid to Hot Ltd for the year of 2019 for management services provided by Hot Ltd. The management fee income had properly been recorded as other income in the financial records of Hot Ltd. 4. On 1 January 2018, in order to transfer more profit to Small Ltd, Hot Ltd sold a machine for administrative purpose costing $1,500 to Small Ltd for $1,020 and the machine is to be used by Small Ltd for 6 years with zero residual value. Small Ltd provides the depreciation using a straight-line method. 5. The dividend paid of Small Ltd during the year was out of the profit for 2017. Hot Ltd recorded it under the heading of Other income. 6. The non-controlling interest was stated at fair value of the acquisition date. The total goodwill of Small Ltd at 1 January 2017 was $3,000 and the goodwill of Small Ltd of subsequent years were: 31 December 2017 $2,400 31 December 2018 $2,500 31 December 2019 $2,000 7. There was no impairment for goodwill of Cold Ltd since its acquisition. 8. On 1 January 2017, the fair value of depreciable non-current assets used for "distribution purpose of Small Ltd exceeded the carrying amount of those assets by $2,000. The remaining useful life remained unchanged at 10 years. Small Ltd has not recorded such adjustment in its book and record. You can assume that the book value of other net assets was equal to the fair value of those assets at the date of acquisition 9. The retained profits of Hot Ltd, Small Ltd, and Cold Ltd at 1 January 2019 were $5,800, $1,200, and $300 respectively. Required: a. Prepare the consolidated income statement of Hot Ltd and its subsidiaries for the year ended 31 December 2019 on the assumption that both Small and Cold Ltd are controlled by Hot Ltd directly and indirectly. (16 marks) b. Prepare the statement of retained profit of the Hot Ltd's company shareholders (i.e. retained profit attributable to parent company's shareholders) (12 marks) Note: All working must be shown. No marks can be given without details if the final figures are wrong. 3

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts