Question: SECTION [A]: COMPULSORY QUESTION Question (1): The following is the trial balance before final adjustments of Sunshine Ltd for the year ended to 30th of

![SECTION [A]: COMPULSORY QUESTION Question (1): The following is the trial](https://s3.amazonaws.com/si.experts.images/answers/2024/09/66dff3104b92b_78366dff30fa025d.jpg)

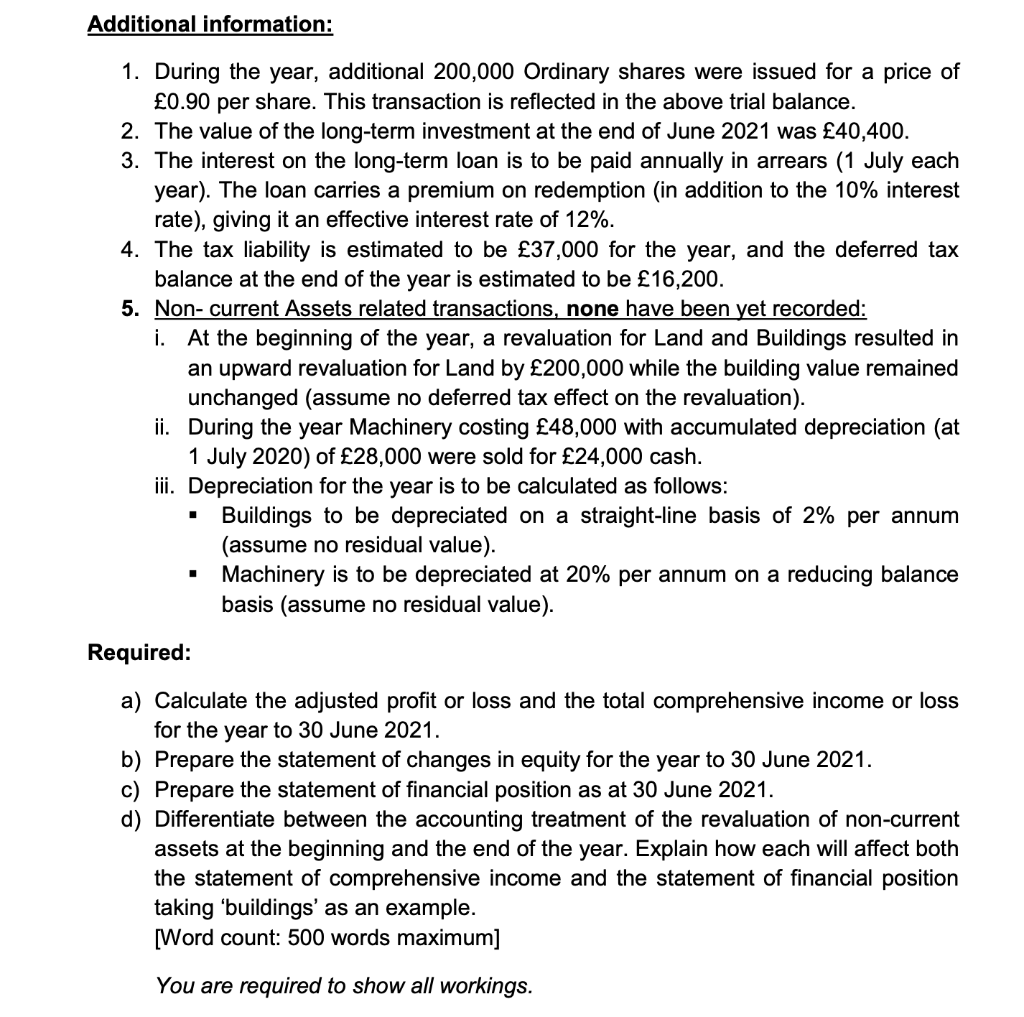

SECTION [A]: COMPULSORY QUESTION Question (1): The following is the trial balance before final adjustments of Sunshine Ltd for the year ended to 30th of June 2021: 124,400 124,360 Inventory (as at 30 June 2021) Trade payables Trade receivables Deferred tax liability (1 July 2020) 144,940 16,800 Bank 434,720 1,400,000 Land 1,400,000 116,000 135,000 60,500 39,600 Buildings (at Cost) Accumulated Depreciation-Buildings (1 July 2020) Machinery (at Cost) Accumulated Depreciation- Machinery (1 July 2020) Long-term Investments (1 July 2020) Share Capital (0.50 each) Share premium Revaluation Surplus (1 July 2020) Retained Earnings (1 July 2020) 10% Loan (repayable in 2029) Profit for the year (subject to items in the additional information) 1,000,000 200,000 600,000 1,080,000 160,000 321,000 3,678,660 3,678,660 Additional information: 1. During the year, additional 200,000 Ordinary shares were issued for a price of 0.90 per share. This transaction is reflected in the above trial balance. 2. The value of the long-term investment at the end of June 2021 was 40,400. 3. The interest on the long-term loan is to be paid annually in arrears (1 July each year). The loan carries a premium on redemption (in addition to the 10% interest rate), giving it an effective interest rate of 12%. 4. The tax liability is estimated to be 37,000 for the year, and the deferred tax balance at the end of the year is estimated to be 16,200. 5. Non-current Assets related transactions, none have been yet recorded: i. At the beginning of the year, a revaluation for Land and Buildings resulted in an upward revaluation for Land by 200,000 while the building value remained unchanged (assume no deferred tax effect on the revaluation). ii. During the year Machinery costing 48,000 with accumulated depreciation (at 1 July 2020) of 28,000 were sold for 24,000 cash. iii. Depreciation for the year is to be calculated as follows: Buildings to be depreciated on a straight-line basis of 2% per annum (assume no residual value). Machinery is to be depreciated at 20% per annum on a reducing balance basis (assume no residual value). 1 . Required: a) Calculate the adjusted profit or loss and the total comprehensive income or loss for the year to 30 June 2021. b) Prepare the statement of changes in equity for the year to 30 June 2021. c) Prepare the statement of financial position as at 30 June 2021. d) Differentiate between the accounting treatment of the revaluation of non-current assets at the beginning and the end of the year. Explain how each will affect both the statement of comprehensive income and the statement of financial position taking 'buildings' as an example. [Word count: 500 words maximum] You are required to show all workings

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts