Question: Section III: Calculation Questions Instruction: 1. Show your calculation steps sufficiently clear. 2. Round your answers with 4 decimals. 2. Assuming an interest rate volatility

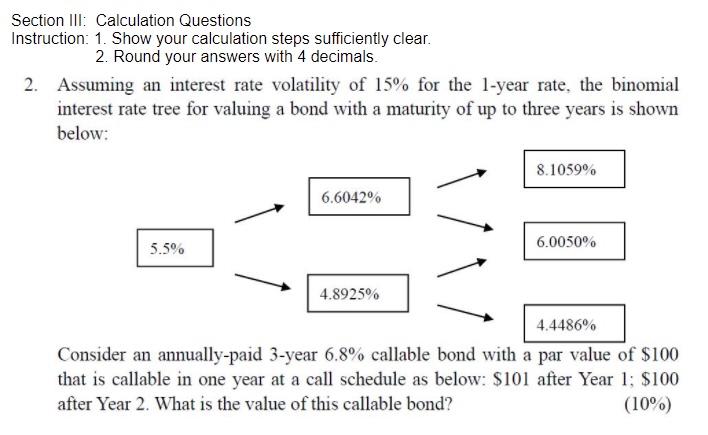

Section III: Calculation Questions Instruction: 1. Show your calculation steps sufficiently clear. 2. Round your answers with 4 decimals. 2. Assuming an interest rate volatility of 15% for the 1-year rate, the binomial interest rate tree for valuing a bond with a maturity of up to three years is shown below: 8.1059% 6.6042 5.5% 6.0050% 4.8925% 4.4486% Consider an annually-paid 3-year 6.8% callable bond with a par value of $100 that is callable in one year at a call schedule as below: $101 after Year 1: $100 after Year 2. What is the value of this callable bond? (10%)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock