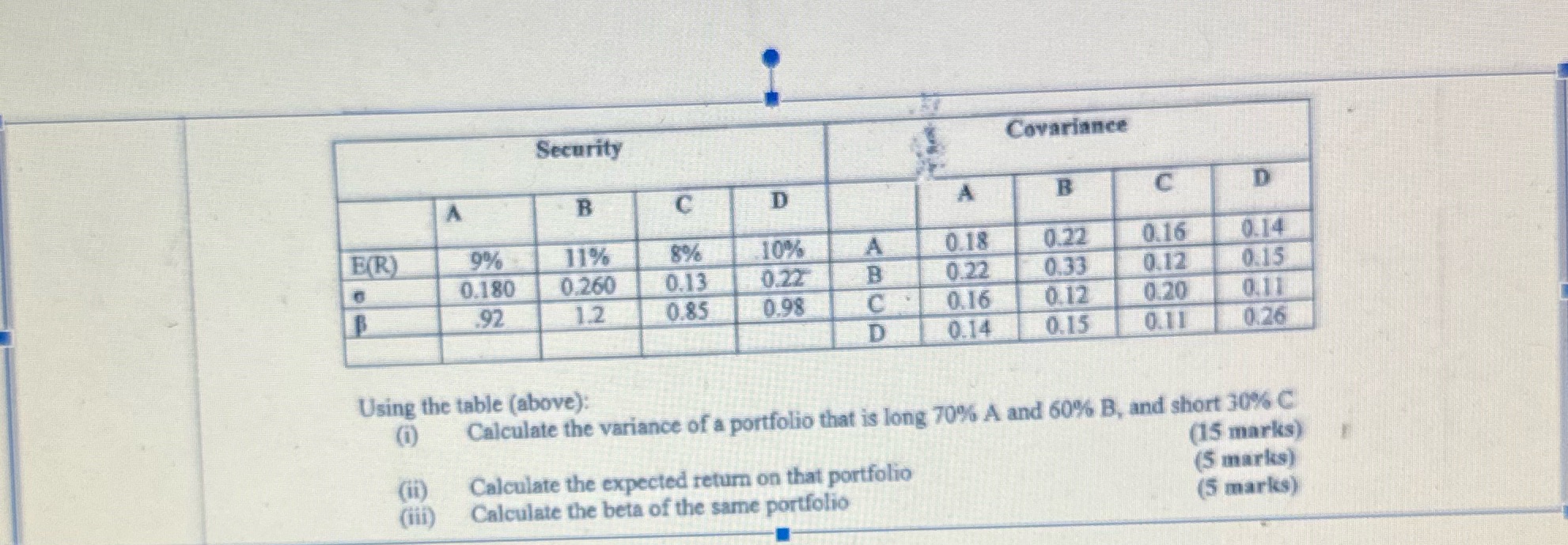

Question: Security Covariance A B C D A B C D E(R) 9% 11% 8% 10% 0.180 0.260 0.13 0.22 B 92 1.2 0.85 0.98

Security Covariance A B C D A B C D E(R) 9% 11% 8% 10% 0.180 0.260 0.13 0.22 B 92 1.2 0.85 0.98 ABCD A 0.18 0.22 0.16 0.14 0.22 0.33 0.12 0.15 C 0.16 0.12 0.20 0.11 0.14 0.15 0.11 0.26 Using the table (above): (i) Calculate the variance of a portfolio that is long 70% A and 60% B, and short 30% C (ii) Calculate the expected return on that portfolio (iii) 88 Calculate the beta of the same portfolio (15 marks) (5 marks) (5 marks)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock