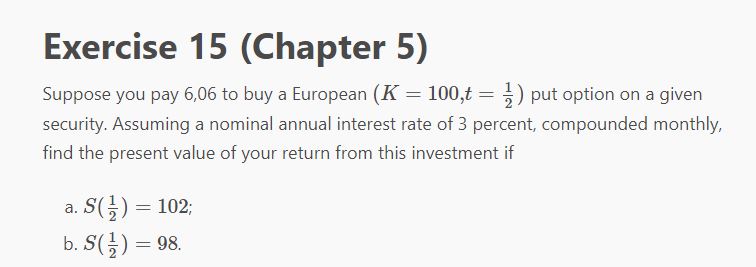

Question: See below: Exercise 15 (Chapter 5) Suppose you pay 6H6 to lou),r a European (K = 100,t = %) put option on a given security.

See below:

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock