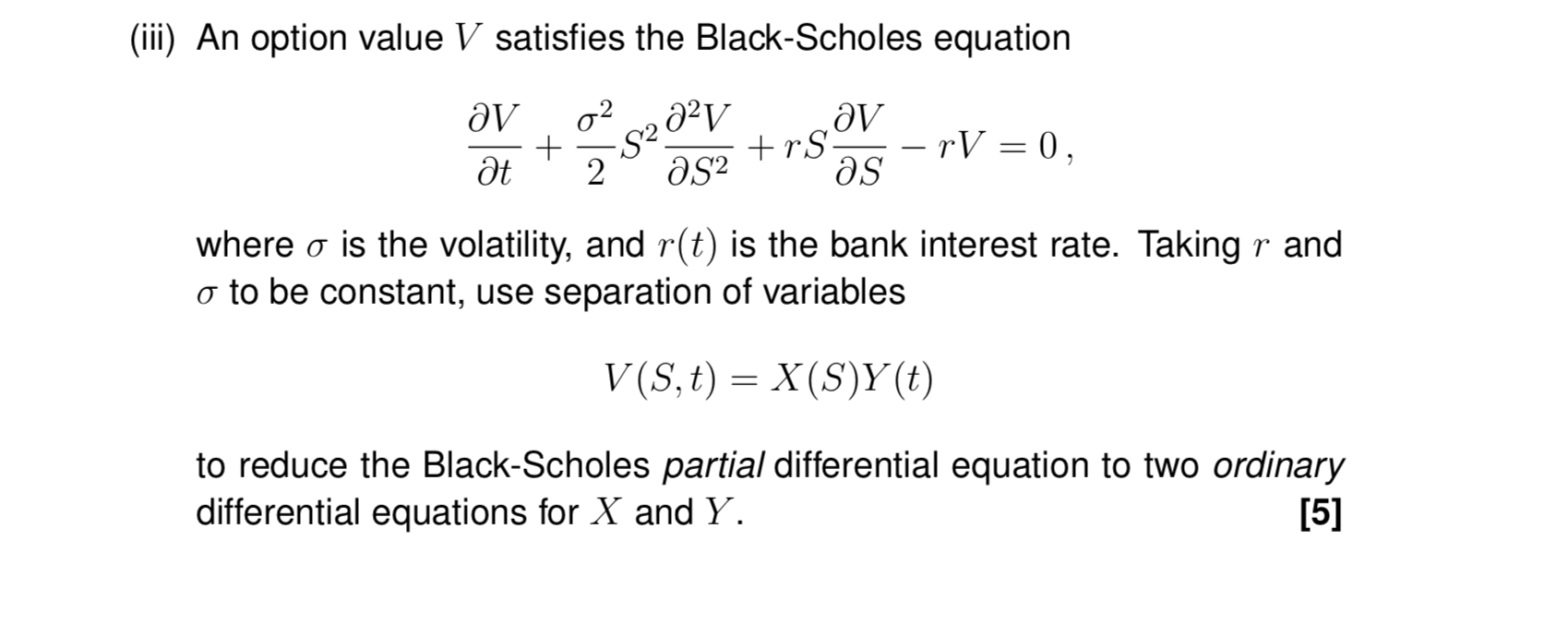

Question: See the question below (iii) An option value V satisfies the Black-Scholes equation av 022321/ av 5+388824TSTV0, where a is the volatility, and r(t) is

See the question below

(iii) An option value V satisfies the Black-Scholes equation av 022321/ av 5+388824TSTV0, where a is the volatility, and r(t) is the bank interest rate. Taking r and a to be constant, use separation of variables V(S, t) = X(S)Y(t) to reduce the Black-Scholes partial differential equation to two ordinary differential equations for X and Y. [5]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock