Question: Select and write True (T) or False (F) for the following 1. If fair value of an impaired asset recovers after an impairment has been

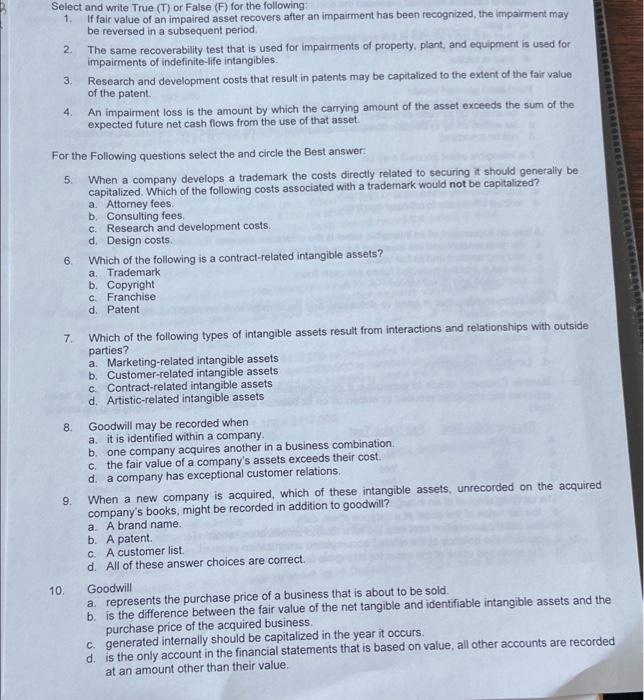

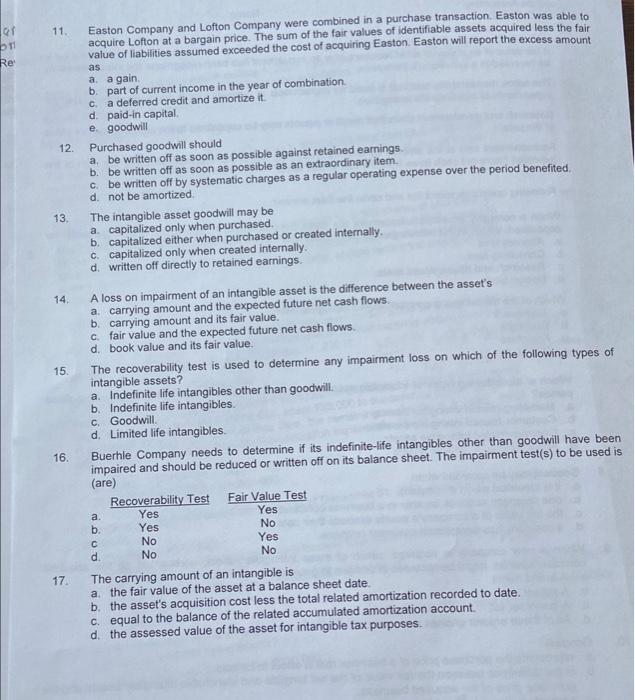

Select and write True (T) or False (F) for the following 1. If fair value of an impaired asset recovers after an impairment has been recognized, the impairment may be reversed in a subsequent period. 2. The same recoverability test that is used for impairments of property. plant, and equipment is used for impairments of indefinite-life intangibles. 3. Research and development costs that result in patents may be capitalized to the extent of the fair value of the patent. 4. An impairment loss is the amount by which the carrying amount of the asset exceeds the sum of the expected future net cash flows from the use of that asset. For the Following questions select the and circle the Best answer: 5. When a company develops a trademark the costs directly related to securing it should generally be capitalized. Which of the following costs associated with a trademark would not be capitalized? a. Attorney fees. b. Consulting fees. c. Research and development costs. d. Design costs. 6. Which of the following is a contract-related intangible assets? a. Trademark b. Copyright c. Franchise d. Patent 7. Which of the following types of intangible assets result from interactions and relationships with outside parties? a. Marketing-related intangible assets b. Customer-related intangible assets c. Contract-related intangible assets d. Artistic-related intangible assets 8. Goodwill may be recorded when a. it is identified within a company. b. one company acquires another in a business combination. c. the fair value of a company's assets exceeds their cost. d. a company has exceptional customer relations. 9. When a new company is acquired, which of these intangible assets, unrecorded on the acquired company's books, might be recorded in addition to goodwill? a. A brand name. b. A patent. c. A customer list. d. All of these answer choices are correct. 10. Goodwill a. represents the purchase price of a business that is about to be sold. b. is the difference between the fair value of the net tangible and identifiable intangible assets and the purchase price of the acquired business. c. generated internally should be capitalized in the year it occurs. d. is the only account in the financial statements that is based on value, all other accounts are recorded at an amount other than their value. 11. Easton Company and Lofton Company were combined in a purchase transaction. Easton was able to acquire Lofton at a bargain price. The sum of the fair values of identifiable assets acquired less the fair value of liabilities assumed exceeded the cost of acquiring Easton. Easton will report the excess amount as a. a gain. b. part of current income in the year of combination. c. a deferred credit and amortize it. d. paid-in capital. e. goodwill 12. Purchased goodwill should a. be written off as soon as possible against retained earnings. b. be written off as soon as possible as an extraordinary item. c. be written off by systematic charges as a regular operating expense over the period benefited. d. not be amortized. 13. The intangible asset goodwill may be a. capitalized only when purchased. b. capitalized either when purchased or created internally. c. capitalized only when created internally. d. written off directly to retained earnings. 14. A loss on impairment of an intangible asset is the difference between the asset's a. carrying amount and the expected future net cash flows. b. carrying amount and its fair value. c. fair value and the expected future net cash flows. d. book value and its fair value. 15. The recoverability test is used to determine any impairment loss on which of the following types of intangible assets? a. Indefinite life intangibles other than goodwill. b. Indefinite life intangibles. c. Goodwill. d. Limited life intangibles. 16. Buerhle Company needs to determine if its indefinite-life intangibles other than goodwill have been impaired and should be reduced or written off on its balance sheet. The impairment test(s) to be used is (are) 17. The carrying amount of an intangible is a. the fair value of the asset at a balance sheet date. b. the asset's acquisition cost less the total related amortization recorded to date. c. equal to the balance of the related accumulated amortization account. d. the assessed value of the asset for intangible tax purposes

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts