Question: Self-Study Problem 6.3 EFG Corporation is owned 40 percent by Ed, 20 percent by Frank, 20 percent by Gene, and 20 percent by X Corporation.

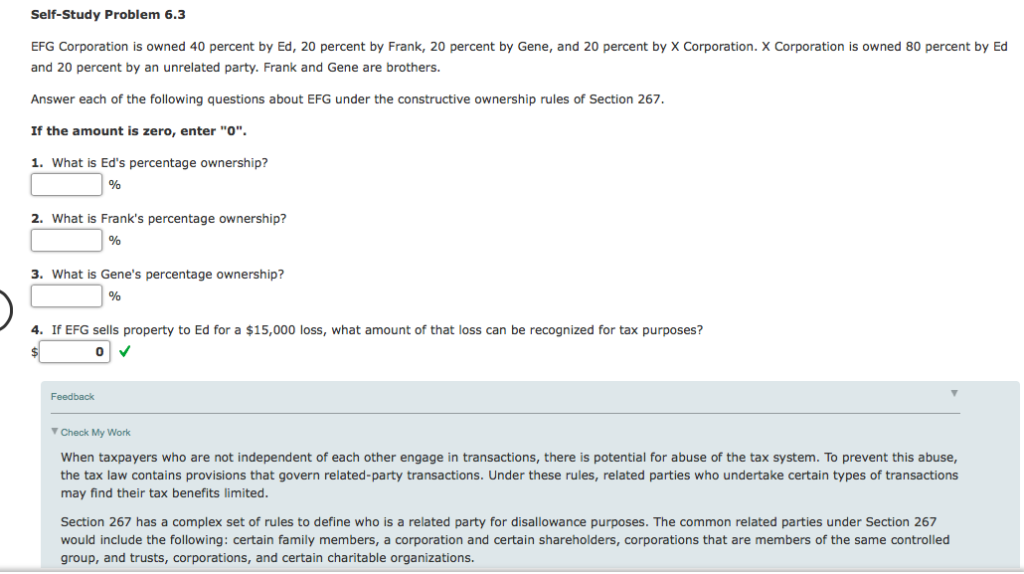

Self-Study Problem 6.3 EFG Corporation is owned 40 percent by Ed, 20 percent by Frank, 20 percent by Gene, and 20 percent by X Corporation. X Corporation is owned 80 percent by Ed and 20 percent by an unrelated party. Frank and Gene are brothers. Answer each of the following questions about EFG under the constructive ownership rules of Section 267. If the amount is zero, enter "O". 1. What is Ed's percentage ownership? 2. What is Frank's percentage ownership? . What is Gene's percentage ownership? 4 If EFG sells property to Ed for a $15,000 loss, what amount of that loss can be recognized for tax purposes? 0 Feedback Check My Work When taxpayers who are not independent of each other engage in transactions, there is potential for abuse of the tax system. To prevent this abuse, the tax law contains provisions that govern related-party transactions. Under these rules, related parties who undertake certain types of transactions may find their tax benefits limited. Section 267 has a complex set of rules to define who is a related party for disallowance purposes. The common related parties under Section 267 would include the following: certain family members, a corporation and certain shareholders, corporations that are members of the same controlled group, and trusts, corporations, and certain charitable organizations. Self-Study Problem 6.3 EFG Corporation is owned 40 percent by Ed, 20 percent by Frank, 20 percent by Gene, and 20 percent by X Corporation. X Corporation is owned 80 percent by Ed and 20 percent by an unrelated party. Frank and Gene are brothers. Answer each of the following questions about EFG under the constructive ownership rules of Section 267. If the amount is zero, enter "O". 1. What is Ed's percentage ownership? 2. What is Frank's percentage ownership? . What is Gene's percentage ownership? 4 If EFG sells property to Ed for a $15,000 loss, what amount of that loss can be recognized for tax purposes? 0 Feedback Check My Work When taxpayers who are not independent of each other engage in transactions, there is potential for abuse of the tax system. To prevent this abuse, the tax law contains provisions that govern related-party transactions. Under these rules, related parties who undertake certain types of transactions may find their tax benefits limited. Section 267 has a complex set of rules to define who is a related party for disallowance purposes. The common related parties under Section 267 would include the following: certain family members, a corporation and certain shareholders, corporations that are members of the same controlled group, and trusts, corporations, and certain charitable organizations

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts