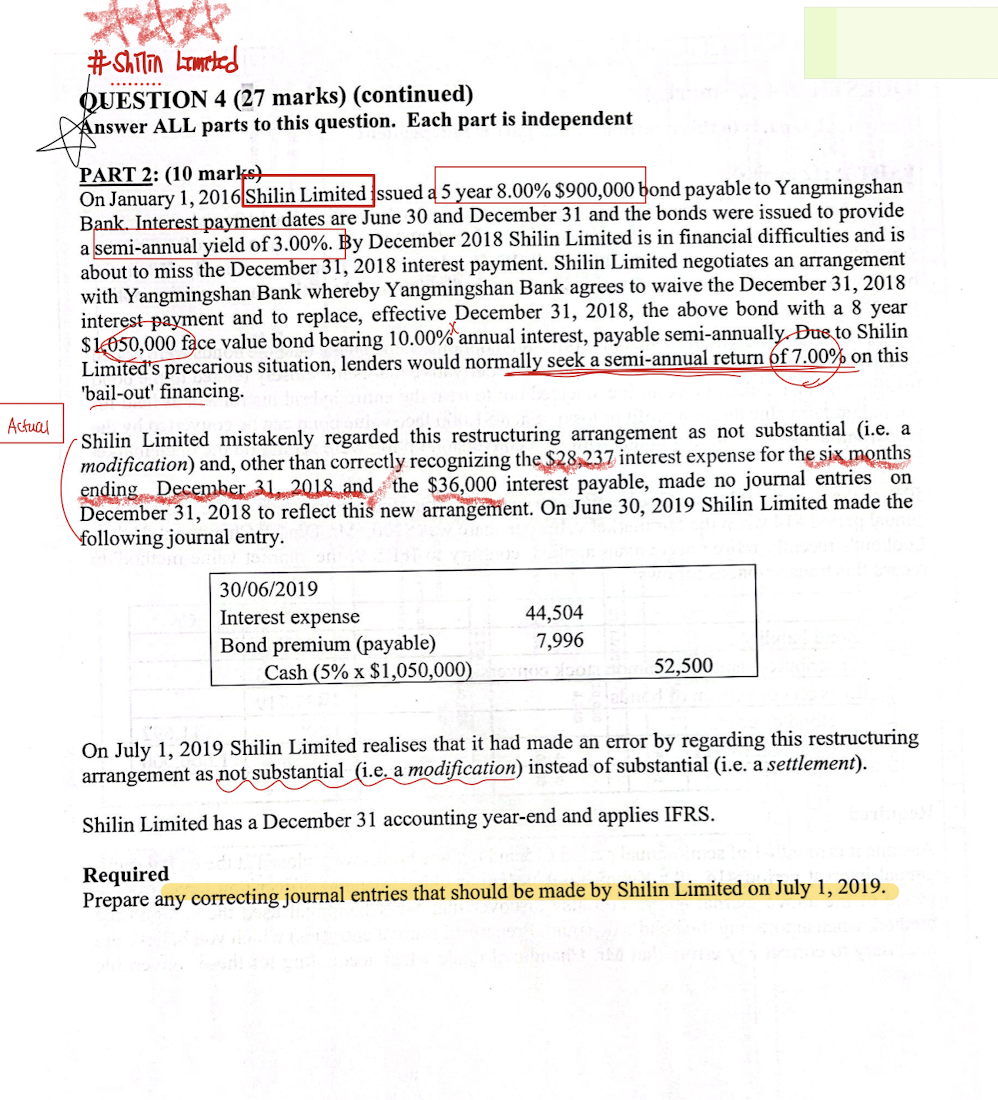

Question: # Shilin Limeted QUESTION 4 (27 marks) (continued) Answer ALL parts to this question. Each part is independent PART 2: (10 marks) On January 1,

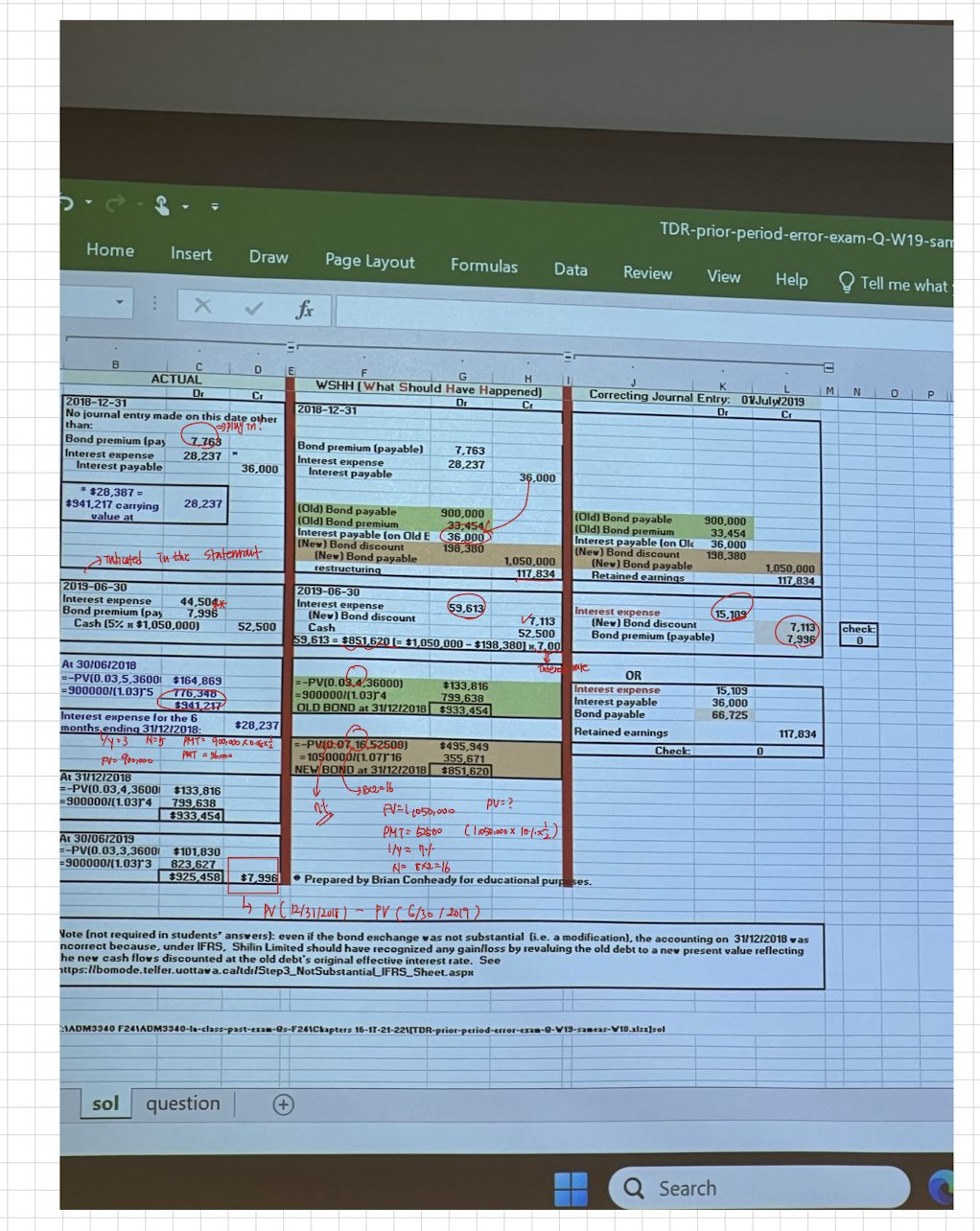

# Shilin Limeted QUESTION 4 (27 marks) (continued) Answer ALL parts to this question. Each part is independent PART 2: (10 marks) On January 1, 2016 Shilin Limited Issued a 5 year 8.00% $900,000 bond payable to Yangmingshan Bank. Interest payment dates are June 30 and December 31 and the bonds were issued to provide semi-annual yield of 3.00%. By December 2018 Shilin Limited is in financial difficulties and is about to miss the December 31, 2018 interest payment. Shilin Limited negotiates an arrangement with Yangmingshan Bank whereby Yangmingshan Bank agrees to waive the December 31, 2018 interest payment and to replace, effective December 31, 2018, the above bond with a 8 year $16050,000 face value bond bearing 10.00% annual interest, payable semi-annually. Due to Shilin Limited's precarious situation, lenders would normally seek a semi-annual return of 7.00% on this 'bail-out' financing. Actual Shilin Limited mistakenly regarded this restructuring arrangement as not substantial (i.e. a modification) and, other than correctly recognizing the $28,237 interest expense for the six months ending December 31 2018 and the $36,000 interest payable, made no journal entries on December 31, 2018 to reflect this new arrangement. On June 30, 2019 Shilin Limited made the following journal entry. 30/06/2019 Interest expense 44,504 Bond premium (payable) 7,996 Cash (5% x $1,050,000) 52,500 On July 1, 2019 Shilin Limited realises that it had made an error by regarding this restructuring arrangement as not substantial (i.e. a modification) instead of substantial (i.e. a settlement). Shilin Limited has a December 31 accounting year-end and applies IFRS. Required Prepare any correcting journal entries that should be made by Shilin Limited on July 1, 2019.TDR-prior-period-error-exam-Q-W19-sam Home Insert Draw Page Layout Formulas Data Review View Help Tell me what X V fix B ACTUAL G WSHH [ What Should Have Happened] M N Dr Correcting Journal Entry: OvJuly2019 2018-12-31 2018-12-31 No journal entry made on this date other than: Bond premium (pay Bond premium (payable] 7,763 Interest expense 28,237 Interest expense Interest payable 28.237 36,000 Interest payable 36.000 $28,387 = $941,217 carrying 28,237 (Old) Bond payable 300,000 (Old) Bond payable 900,000 value at (Old] Bond premium 23.454/ (Old) Bond premium Interest payable (on Old E (36,000 33,454 Interest payable (on Ok 36,000 (New) Bond discount 198,380 (New ] Bond discount 198.380 Tunicated in the statement (New ) Bond payable 1,050.000 (New) Bond payable 1,050,000 restructuring 117 834 Retained earnings 117 834 2019-06-30 2019-06-30 Interest expense 44,504X Interest expense 59,613 Interest expense 15.109 Bond premium [pay 7.996 (New) Bond discount 7.113 (New ] Bond discount 7,113 Cash (5%% x $1,050,000) 52,500 Cash 52,500 Bond premium (payable] 7,996 check 59 613 = $851 620 (= $1.050 000 - $198 3801 x 7,00 At 30/06/2018 OR =-PV(0.03,5,36001 $164.869 =-PV(0.06.4/36000) $133,816 Interest expense 15,109 =900000/(1.03)5 776,348 =900000/(1.03)4 799.638 Interest payable $6.000 $941 217 OLD BOND at 31/12/2018 $933,454 Bond payable 66.725 Interest expense for the 6 months, ending 31/12/2018: $28,237 Retained earnings 117,834 /4 . 3 PMT: 900/010 *0-45RX =-PVC.9\\ 16 52508) $495,949 Check PV= 9102000 PMT = 3bros = 1050000/[1.07)16 355,671 NEW BOND at 31/12/2018 $851.620 At 31/12/2018 =-PV(0.03.4,3600 $133,816 -900000/(1.03)4 799 638 AV= 1 1050, 010 PV : ? $933.454 PMT : 576560 At 30/06/2019 -PV(0.03,3,36001 $101,830 Hy = 71 - 900000/(1.03)3 823,627 12 8 * 2 = 16 $925.458 $7.996) . Prepared by Brian Conheady for educational purpo 4 PV ( 12 / 3 1 / 20IF ) - PV ( 6/ 30 / 2019 ) Note (not required in students' answers): even if the bond exchange was not substantial (i.e. a modification], the accounting on 31/12/2018 was ncorrect because, under IFRS. Shilin Limited should have recognized any gainiloss by revaluing the old debt to a new present value reflecting he new cash flows discounted at the old debt's original effective interest rate. attps://bomode.telfer.uottawa.caltdr/Step3_NotSubstantialIFRS_Sheet.aspx :ADM3340 F24\\ADM3340-Is-class-past-exam.@s-F24\\Chapters 16-17-21-22 meas-V18.xlsx]sol sol question + Q Search

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!