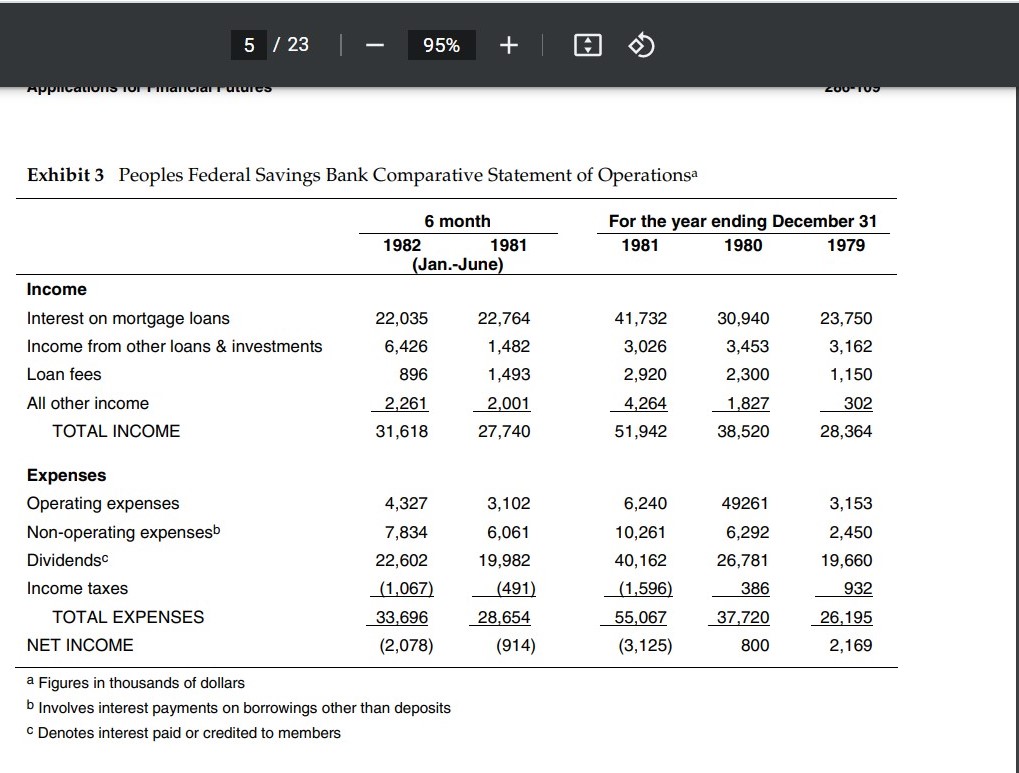

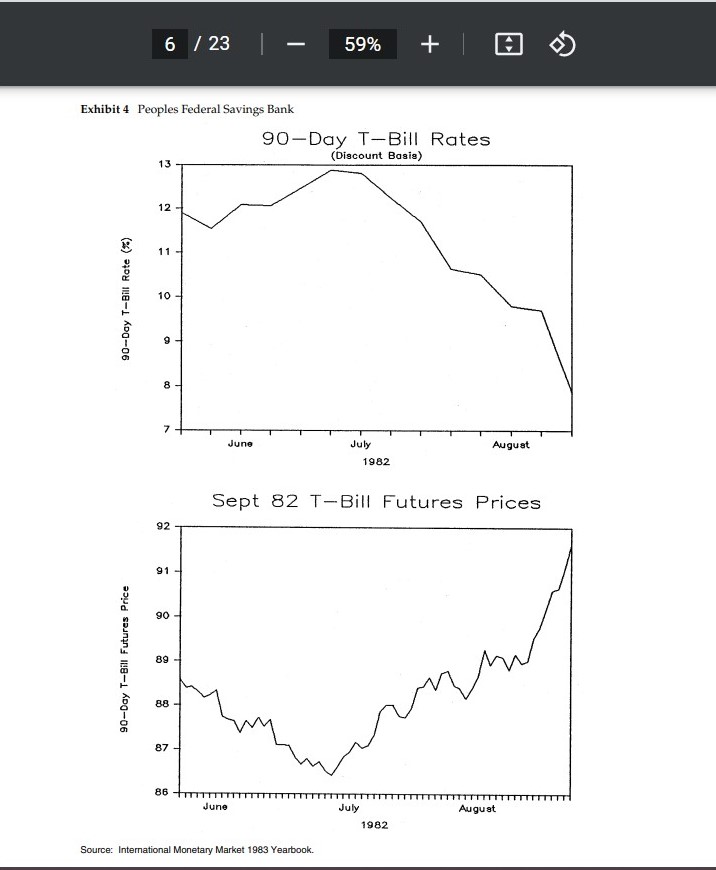

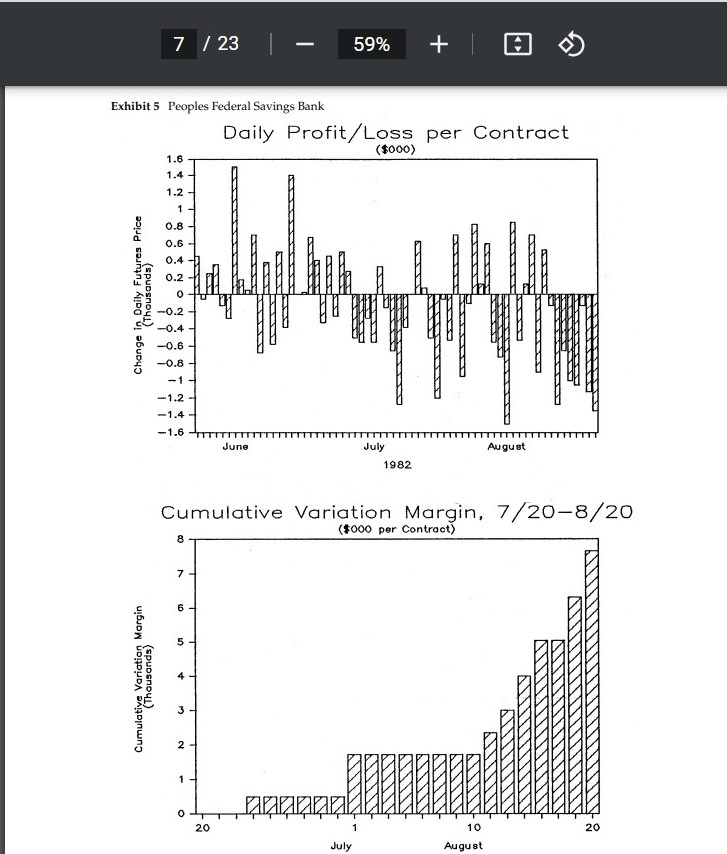

Should Peoples Federal Savings have hedged its September 1 savings certificate rollover? What would you have advised

Fantastic news! We've Found the answer you've been seeking!

Question:

- Should Peoples Federal Savings have hedged its September 1 savings certificate rollover?

- What would you have advised Mr. Myers to do on August 6?

- How should Mr. Myers explain his future losses to the board on August 27?

Expert Answer:

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date: