Question: show all work please! You are considering purchasing a portfolio of two stocks. XYZ has a variance of 0.04 and ABC has a variance of

show all work please!

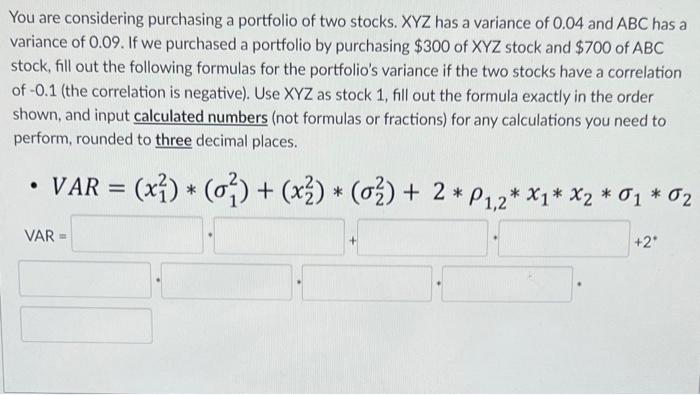

You are considering purchasing a portfolio of two stocks. XYZ has a variance of 0.04 and ABC has a variance of 0.09. If we purchased a portfolio by purchasing $300 of XYZ stock and $700 of ABC stock, fill out the following formulas for the portfolio's variance if the two stocks have a correlation of -0.1 (the correlation is negative). Use XYZ as stock 1, fill out the formula exactly in the order shown, and input calculated numbers (not formulas or fractions) for any calculations you need to perform, rounded to three decimal places. . VAR = (x}) * (0%) + (x}) * (0%) + 2*21,2* *1* x2 * 01 * O2 X1 * VAR + +2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock