Question: Show that a term structure model with flat yield curves and parallel yield curve shifts contains arbitrage opportunities as follows. Consider the following model: At

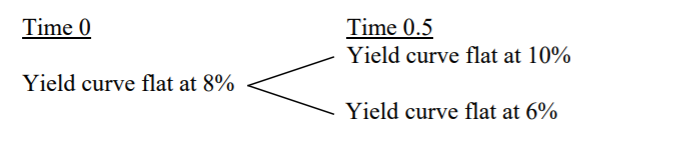

Show that a term structure model with flat yield curves and parallel yield curve shifts contains arbitrage opportunities as follows. Consider the following model: At time 0 the yield curve is flat at 8%. At time 0.5 there are two possible states, the yield curve is either flat at 10% or flat at 6%. This is depicted below:

a) Draw a tree containing the time 0 price and the two possible time 0.5 payoffs (or prices) for three different assets: a zero maturing at time 0.5, a zero maturing at time 10, and a zero maturing at time 30, $100 par value each.

b) Consider a portfolio of 0.5- and 30-year zeroes that replicates $100 par of the 10- year zero, or in other words, that has the same value as $100 par of the 10-year zero in both states at time 0.5.

(i) Determine the par amounts of the 0.5- and 30-year zeroes in this replicating portfolio.

(ii) What is the cost of this replicating portfolio at time 0?

c) Describe an arbitrage opportunity in this market and indicate the arbitrage profit.

d) Suppose we change the yield on the 10-year zero to eliminate the arbitrage opportunity. What would the yield have to be?

Time 0.5 Yield curve flat at 10% Yield curve flat at 8% Yield curve flat at 6% Time 0.5 Yield curve flat at 10% Yield curve flat at 8% Yield curve flat at 6%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts