Question: Since the SUTA rates changes are made at the end of each year and there is much discussion about changes to the FUTA rate, the

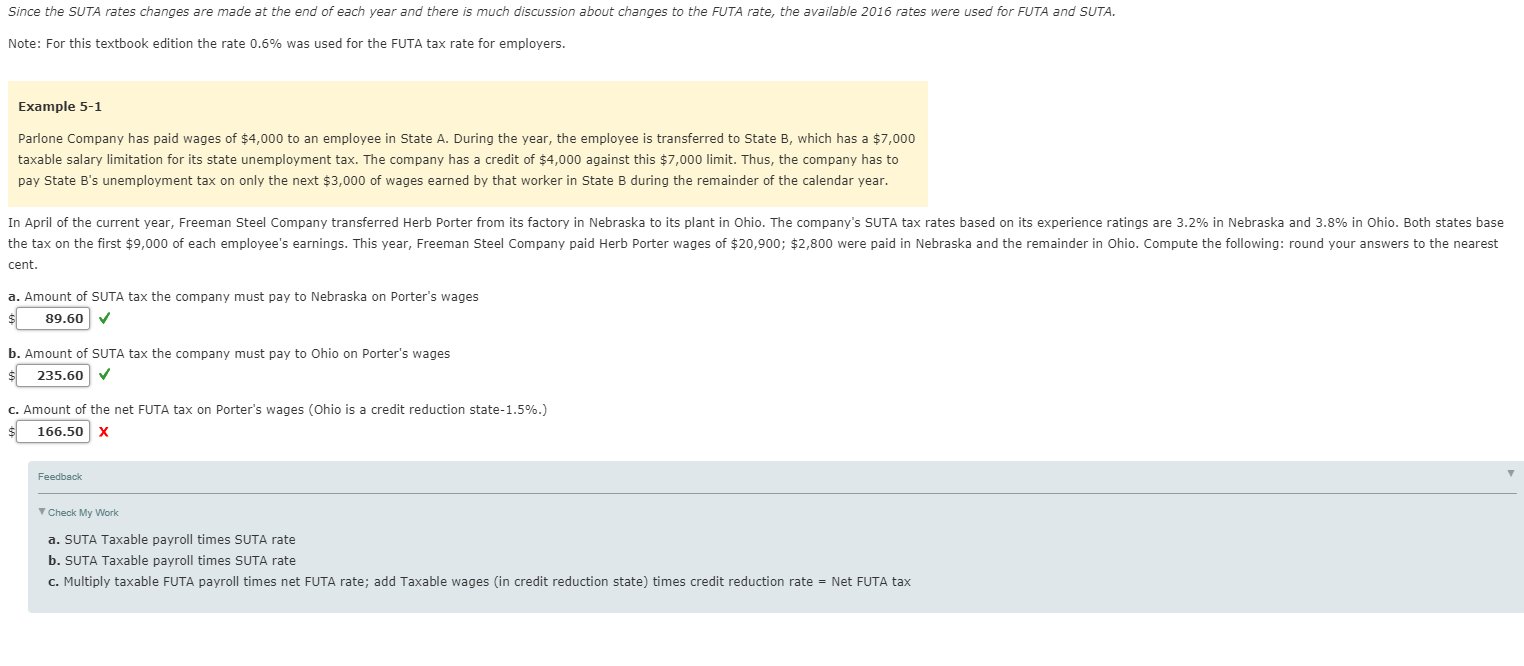

Since the SUTA rates changes are made at the end of each year and there is much discussion about changes to the FUTA rate, the available 2016 rates were used for FUTA and SUTA. Note: For this textbook edition the rate 0.6% was used for the FUTA tax rate for employers. Example 5-1 Parlone Company has paid wages of $4,000 to an employee in State A. During the year, the employee is transferred to State B, which has a $7,000 taxable salary limitation for its state unemployment tax. The company has a credit of $4,000 against this $7,000 limit. Thus, the company has to pay State B's unemployment tax on only the next $3,000 of wages earned by that worker in State B during the remainder of the calendar year. In April of the current year, Freeman Steel Company transferred Herb Porter from its factory in Nebraska to its plant in Ohio. The company's SUTA tax rates based on its experience ratings are 3.2% in Nebraska and 3.8% in Ohio. Both states base the tax on the first $9,000 of each employee's earnings. This year, Freeman Steel Company paid Herb Porter wages of $20,900; $2,800 were paid in Nebraska and the remainder in Ohio. Compute the following: round your answers to the nearest cent. a. Amount of SUTA tax the company must pay to Nebraska on Porter's wages $ 89.60 b. Amount of SUTA tax the company must pay to Ohio on Porter's wages $ 235.60 c. Amount of the net FUTA tax on Porter's wages (Ohio is a credit reduction state-1.5%.) $ 166.50 x Feedback Check My Work a. SUTA Taxable payroll times SUTA rate b. SUTA Taxable payroll times SUTA rate c. Multiply taxable FUTA payroll times net FUTA rate; add Taxable wages (in credit reduction state) times credit reduction rate = Net FUTA tax Since the SUTA rates changes are made at the end of each year and there is much discussion about changes to the FUTA rate, the available 2016 rates were used for FUTA and SUTA. Note: For this textbook edition the rate 0.6% was used for the FUTA tax rate for employers. Example 5-1 Parlone Company has paid wages of $4,000 to an employee in State A. During the year, the employee is transferred to State B, which has a $7,000 taxable salary limitation for its state unemployment tax. The company has a credit of $4,000 against this $7,000 limit. Thus, the company has to pay State B's unemployment tax on only the next $3,000 of wages earned by that worker in State B during the remainder of the calendar year. In April of the current year, Freeman Steel Company transferred Herb Porter from its factory in Nebraska to its plant in Ohio. The company's SUTA tax rates based on its experience ratings are 3.2% in Nebraska and 3.8% in Ohio. Both states base the tax on the first $9,000 of each employee's earnings. This year, Freeman Steel Company paid Herb Porter wages of $20,900; $2,800 were paid in Nebraska and the remainder in Ohio. Compute the following: round your answers to the nearest cent. a. Amount of SUTA tax the company must pay to Nebraska on Porter's wages $ 89.60 b. Amount of SUTA tax the company must pay to Ohio on Porter's wages $ 235.60 c. Amount of the net FUTA tax on Porter's wages (Ohio is a credit reduction state-1.5%.) $ 166.50 x Feedback Check My Work a. SUTA Taxable payroll times SUTA rate b. SUTA Taxable payroll times SUTA rate c. Multiply taxable FUTA payroll times net FUTA rate; add Taxable wages (in credit reduction state) times credit reduction rate = Net FUTA tax

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts