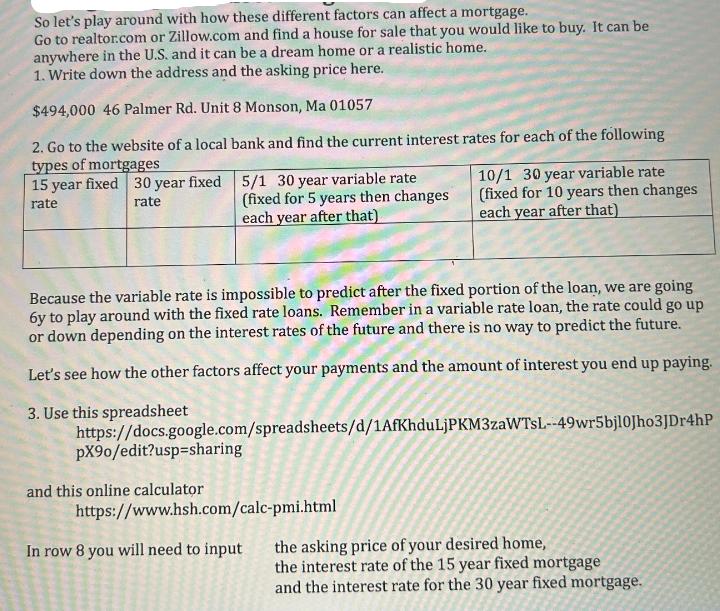

So let's play around with how these different factors can affect a mortgage. Go to realtor.com...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

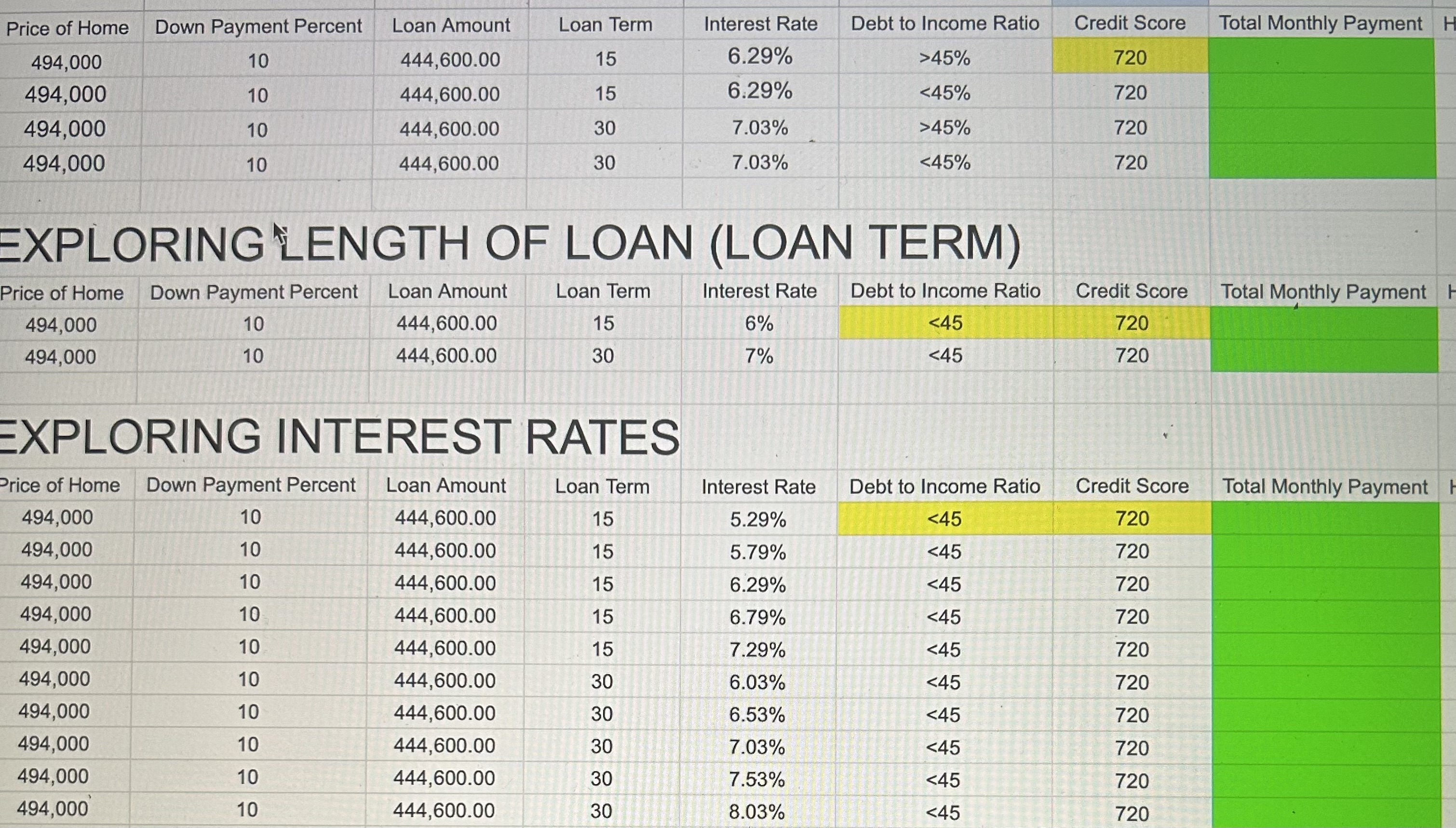

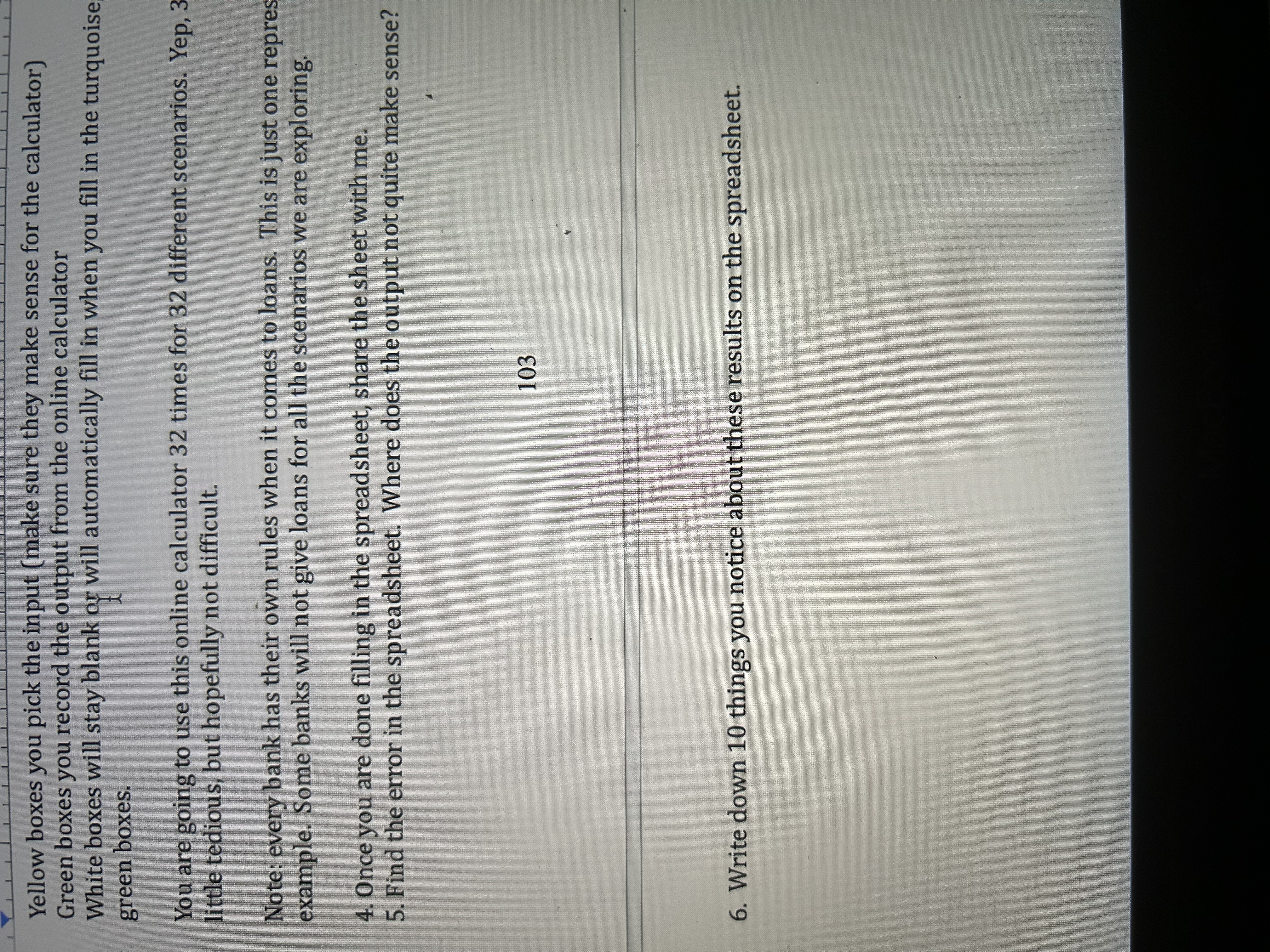

So let's play around with how these different factors can affect a mortgage. Go to realtor.com or Zillow.com and find a house for sale that you would like to buy. It can be anywhere in the U.S. and it can be a dream home or a realistic home. 1. Write down the address and the asking price here. $494,000 46 Palmer Rd. Unit 8 Monson, Ma 01057 2. Go to the website of a local bank and find the current interest rates for each of the following types of mortgages 15 year fixed 30 year fixed 5/1 30 year variable rate (fixed for 5 years then changes each year after that) rate rate 10/1 30 year variable rate (fixed for 10 years then changes each year after that) Because the variable rate is impossible to predict after the fixed portion of the loan, we are going 6y to play around with the fixed rate loans. Remember in a variable rate loan, the rate could go up or down depending on the interest rates of the future and there is no way to predict the future. Let's see how the other factors affect your payments and the amount of interest you end up paying. 3. Use this spreadsheet https://docs.google.com/spreadsheets/d/1AfKhduLjPKM3zaWTSL--49wr5bj10Jho3JDr4hP pX90/edit?usp=sharing and this online calculator https://www.hsh.com/calc-pmi.html In row 8 you will need to input the asking price of your desired home, the interest rate of the 15 year fixed mortgage and the interest rate for the 30 year fixed mortgage. Price of Home 494,000 494,000 Down Payment Percent Loan Amount Loan Term Interest Rate Debt to Income Ratio Credit Score Total Monthly Payment H 10 444,600.00 15 6.29% >45% 720 10 444,600.00 15 6.29% <45% 720 494,000 494,000 10 444,600.00 30 7.03% >45% 720 10 444,600.00 30 7.03% <45% 720 EXPLORING LENGTH OF LOAN (LOAN TERM) Price of Home Down Payment Percent Loan Amount 494,000 494,000 10 10 Loan Term Interest Rate Debt to Income Ratio Credit Score Total Monthly Payment H 444,600.00 444,600.00 15 6% <45 720 30 7% <45 720 EXPLORING INTEREST RATES Price of Home Down Payment Percent Loan Amount Loan Term Interest Rate Debt to Income Ratio Credit Score Total Monthly Payment H 494,000 10 444,600.00 15 5.29% <45 720 494,000 10 444,600.00 15 5.79% <45 720 494,000 10 444,600.00 15 6.29% <45 720 494,000 10 444,600.00 15 494,000 10 444,600.00 15 55 6.79% <45 720 7.29% <45 720 494,000 10 444,600.00 30 6.03% <45 720 494,000 10 444,600.00 30 6.53% <45 720 494,000 10 444,600.00 30 7.03% <45 720 494,000 10 444,600.00 30 7.53% <45 720 494,000 10 444,600.00 30 8.03% <45 720 Yellow boxes you pick the input (make sure they make sense for the calculator) Green boxes you record the output from the online calculator White boxes will stay blank or will automatically fill in when you fill in the turquoise, green boxes. You are going to use this online calculator 32 times for 32 different scenarios. Yep, 3 little tedious, but hopefully not difficult. Note: every bank has their own rules when it comes to loans. This is just one repres example. Some banks will not give loans for all the scenarios we are exploring. 4. Once you are done filling in the spreadsheet, share the sheet with me. 5. Find the error in the spreadsheet. Where does the output not quite make sense? 103 6. Write down 10 things you notice about these results on the spreadsheet. So let's play around with how these different factors can affect a mortgage. Go to realtor.com or Zillow.com and find a house for sale that you would like to buy. It can be anywhere in the U.S. and it can be a dream home or a realistic home. 1. Write down the address and the asking price here. $494,000 46 Palmer Rd. Unit 8 Monson, Ma 01057 2. Go to the website of a local bank and find the current interest rates for each of the following types of mortgages 15 year fixed 30 year fixed 5/1 30 year variable rate (fixed for 5 years then changes each year after that) rate rate 10/1 30 year variable rate (fixed for 10 years then changes each year after that) Because the variable rate is impossible to predict after the fixed portion of the loan, we are going 6y to play around with the fixed rate loans. Remember in a variable rate loan, the rate could go up or down depending on the interest rates of the future and there is no way to predict the future. Let's see how the other factors affect your payments and the amount of interest you end up paying. 3. Use this spreadsheet https://docs.google.com/spreadsheets/d/1AfKhduLjPKM3zaWTSL--49wr5bj10Jho3JDr4hP pX90/edit?usp=sharing and this online calculator https://www.hsh.com/calc-pmi.html In row 8 you will need to input the asking price of your desired home, the interest rate of the 15 year fixed mortgage and the interest rate for the 30 year fixed mortgage. Price of Home 494,000 494,000 Down Payment Percent Loan Amount Loan Term Interest Rate Debt to Income Ratio Credit Score Total Monthly Payment H 10 444,600.00 15 6.29% >45% 720 10 444,600.00 15 6.29% <45% 720 494,000 494,000 10 444,600.00 30 7.03% >45% 720 10 444,600.00 30 7.03% <45% 720 EXPLORING LENGTH OF LOAN (LOAN TERM) Price of Home Down Payment Percent Loan Amount 494,000 494,000 10 10 Loan Term Interest Rate Debt to Income Ratio Credit Score Total Monthly Payment H 444,600.00 444,600.00 15 6% <45 720 30 7% <45 720 EXPLORING INTEREST RATES Price of Home Down Payment Percent Loan Amount Loan Term Interest Rate Debt to Income Ratio Credit Score Total Monthly Payment H 494,000 10 444,600.00 15 5.29% <45 720 494,000 10 444,600.00 15 5.79% <45 720 494,000 10 444,600.00 15 6.29% <45 720 494,000 10 444,600.00 15 494,000 10 444,600.00 15 55 6.79% <45 720 7.29% <45 720 494,000 10 444,600.00 30 6.03% <45 720 494,000 10 444,600.00 30 6.53% <45 720 494,000 10 444,600.00 30 7.03% <45 720 494,000 10 444,600.00 30 7.53% <45 720 494,000 10 444,600.00 30 8.03% <45 720 Yellow boxes you pick the input (make sure they make sense for the calculator) Green boxes you record the output from the online calculator White boxes will stay blank or will automatically fill in when you fill in the turquoise, green boxes. You are going to use this online calculator 32 times for 32 different scenarios. Yep, 3 little tedious, but hopefully not difficult. Note: every bank has their own rules when it comes to loans. This is just one repres example. Some banks will not give loans for all the scenarios we are exploring. 4. Once you are done filling in the spreadsheet, share the sheet with me. 5. Find the error in the spreadsheet. Where does the output not quite make sense? 103 6. Write down 10 things you notice about these results on the spreadsheet.

Expert Answer:

Related Book For

Posted Date:

Students also viewed these finance questions

-

must be based on the document. What are the Different Pricing Strategies? By QuickBooks Canada Team It's no secret that small businesses play a vital role in the Canadian economy. However, revenue...

-

Planning is one of the most important management functions in any business. A front office managers first step in planning should involve determine the departments goals. Planning also includes...

-

Ms. Esperanto obtained a $40,000 home equity loan at 7.5% compounded monthly. a. What will she pay monthly if the amortization period is 15 years? b. How much of the payment made at the end of the...

-

Explain why the common assumption that larger families reduce child-rearing quality, resulting in less intelligent children, is mistaken.

-

Calculate the predetermined over head rate assuring sandhill company estimates total manufacturing overhead costs of 1 0 0 8 0 0 0.

-

What are some reasons a potential prospect might not be readily accessible? How far should you go to try to overcome such an accessibility problem before you move to the next lead?

-

One year ago, your company purchased a machine used in manufacturing for $110,000. You have learned that a new machine is available that offers many advantages; you can purchase it for $150,000...

-

In Walker's multiple-step income statement, gross profit? Walker, Inc. has the following information is available: Cost of goods sold $150300 Dividend revenue 3600 Income tax expense 3200 Operating...

-

Solve the below Bernoulli equation. Answer questions 1-8 for full marks. 4 y'+=y=xy X v=yl-n Note: 1. determine n (5 mark) 2. determine y (5 mark) 3. determine y' (5 mark) 4. determine p(x) (5 mark)...

-

The main problem of this study is what is the effect of the lecturer's perception of the practice of orientation multidimensional leadership by the head of the academic department on the...

-

One potential source of error is allowing the Cu to coat the Mg turnings, trapping Mg inside a protective layer of Cu, which prevents the Mg from being completely oxidized by the HCI added in step...

-

Is monogamy considered the optimal or ideal relational structure for contemporary relationships in the 21st century, given the evolving socio-cultural landscape and diverse perspectives on...

-

Sam and Esterina are married, file a joint return, and have two children, ages 9 and 12. Their combined AGI is $67,000. Sam's earned income is $43,000; Esterina's is $27,000. They incur $6,900 of...

-

How do sociological inquiries into social movements, collective behavior, and social control shed light on the mechanisms through which individuals mobilize for social justice, resistance, or...

-

Evaluate the major stakeholder groups that influence and are influenced by small companies and discuss the primary responsibilities of small companies in Malaysia. In addition analyze how a small...

-

Borrowing costs should be recognised as an expense and charged to the profit and loss account of the period in which they are incurred : A. If the borrowing costs relate to qualifying asset B. If the...

-

Many states have lotteries that involve the random selection of digits 0, 1, 2, ,

-

Is the distribution of those digits a normal distribution? Why or why not?

-

Birth weights in the United States are normally distributed with a mean (in grams) of 3420 g and a standard deviation of 495 g. If you graph this normal distribution, the area to the right of 4000 g...

Study smarter with the SolutionInn App