Question: Sofas Company Pte Ltd ( SC ) is a manufacturer of ergonomic sofas for homes. The company adopts a first - in -

Sofas Company Pte Ltd SC is a manufacturer of ergonomic sofas for homes. The company adopts a firstinfirstout inventory valuation method and a perpetual inventory system to manage its inventories. The company's financial yearend is on December. SC calculates its product costs using a joborder costing system and assigns manufacturing overheads based on machine hours.

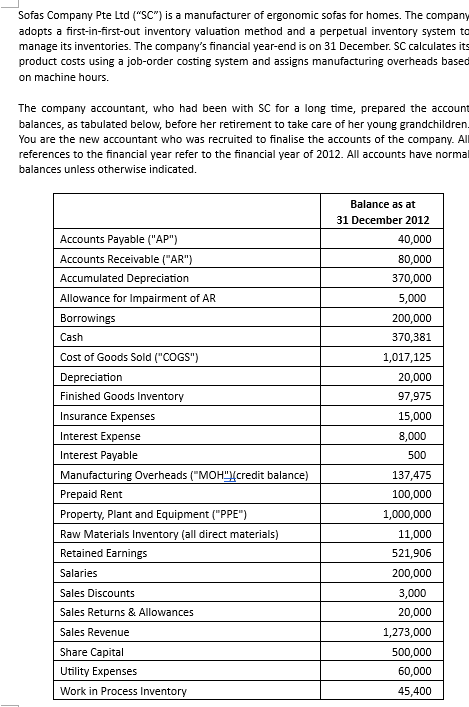

The company accountant, who had been with SC for a long time, prepared the account balances, as tabulated below, before her retirement to take care of her young grandchildren. You are the new accountant who was recruited to finalise the accounts of the company. Al references to the financial year refer to the financial year of All accounts have normal balances unless otherwise indicated.

begintabularlr

hline & begintabularc

Balance as at

December

endtabular

hline Accounts Payable AP &

hline Accounts Receivable AR &

hline Accumulated Depreciation &

hline Allowance for Impairment of AR &

hline Borrowings &

hline Cash &

hline Cost of Goods Sold COGS &

hline Depreciation &

hline Finished Goods Inventory &

hline Insurance Expenses &

hline Interest Expense &

hline Interest Payable &

hline Manufacturing Overheads MOHcredit balance &

hline Prepaid Rent &

hline Property, Plant and Equipment PPE &

hline Raw Materials Inventory all direct materials &

hline Retained Earnings &

hline Salaries &

hline Sales Discounts &

hline Sales Returns & Allowances &

hline Sales Revenue &

hline Share Capital &

hline Utility Expenses &

hline Work in Process Inventory &

hline

endtabular After extensive work on the accounts of SC you gathered the following information relating to possible omissions or errors:

The balances of selected accounts as at December are tabled below. All accounts have normal balances.

Budgeted manufacturing overhead was $ per annum. Budgeted and actual machine hours were hours and hours respectively per annum. Budgeted and actual direct labour hours were hours and hours respectively per annum. Actual labour rate is $ per hour.

Accounts payable was used by SC solely for raw material purchases and payments. All raw material purchases are on credit and these purchases are incurred evenly throughout the year. Payment to raw material suppliers was $ during the year. Out of all the raw materials purchased in the financial year, are indirect materials.

On December a customer discovered that sofas purchased on account total revenue: $ total cost: $ were of the wrong colour. The customer intended to return these sofas to the company but kept the units after SC sent a $ credit note to compensate the customer. No journal entries were made for the credit note of $

SC used two machines to manufacture a range of recliner sofas. The annual depreciation of the two machines was $ No journal entries were made for the depreciation of both machines for the financial year.

In December SC delivered a batch of sofas total cost: $ to a consignee at a markup At the end of the financial year, none of the sofas were sold by the consignee. SC has accounted for the consignment sale as a normal sale on account. The borrowings as at December relate to a year working capital borrowing those finances raw material purchases, labour payments and overheads used by the company to manufacture the sofas. SC took out a $ borrowing on October and the borrowing was repayable in three equal annual instalments beginning October The borrowing has an interest rate of per annum payable semiannually in arrears on every October and April. Hint: Such interest expense is not a product cost.

SC pays annual rent of $ in advance on every January $ of the annual rent is incurred to rent space for factory operations, while the rest is incurred to rent a warehouse to store completed sofas. SC has no other rented space.

On December SC received invoices for December s training expenses for its factory employees and utility expenses for December The training expenses totalled $ while the utility expenses totalled $ of the utility expenses are for the factory while the rest is for the office. No journal entries had been made for the training expenses and the utility bills.

Required

a Prepare SCs schedule of cost of goods manufactured for the financial year ended December

b Using the information provided in points to above, prepare the adjusting and correcting journal entries for the financial year ended December If no adjusting or correcting journal entry is required for a particular point, explain the reason. No narration or dates are required. Marks will be awarded for appropriate workings.

c Was the manufacturing overhead under or over applied? Write a journal entry to close the underover applied manufacturing overhead to the cost of g

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock