Question: solve 2. Forecasting Consider the following ARMA process. m= 0.5 + 0.444 + 0.71.2 + O.1ay-1 + 0.6a;-2 + at () a) What are the

solve

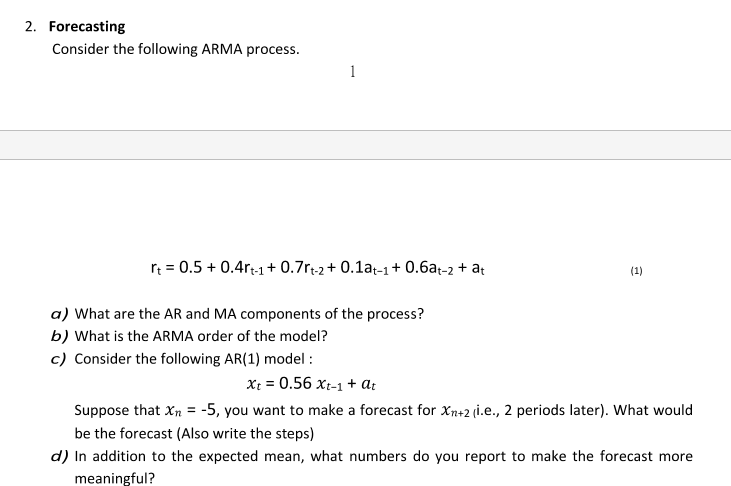

2. Forecasting Consider the following ARMA process. m= 0.5 + 0.444 + 0.71.2 + O.1ay-1 + 0.6a;-2 + at () a) What are the AR and MA components of the process? 45) What is the ARMA order of the model? ) Consider the following AR(1) model : xX, = 0.56 X11+ ar Suppose that Xn = -5, you want to make a forecast for Xn+2,i.e., 2 periods later). What would be the forecast (Also write the steps) d) |In addition to the expected mean, what numbers do you report to make the forecast more meaningful

2. Forecasting Consider the following ARMA process. m= 0.5 + 0.444 + 0.71.2 + O.1ay-1 + 0.6a;-2 + at () a) What are the AR and MA components of the process? 45) What is the ARMA order of the model? ) Consider the following AR(1) model : xX, = 0.56 X11+ ar Suppose that Xn = -5, you want to make a forecast for Xn+2,i.e., 2 periods later). What would be the forecast (Also write the steps) d) |In addition to the expected mean, what numbers do you report to make the forecast more meaningful

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock