Question: Solve for mini case Solving for the Optimal International Portfolio Suppose you are a financial adviser and your client, who is currently investing only in

Solve for mini case

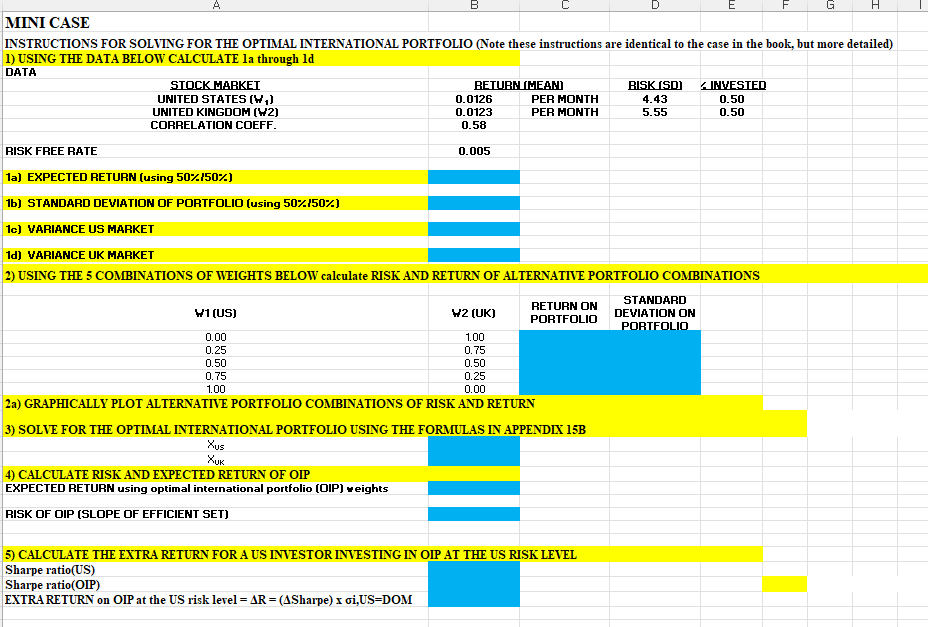

Solving for the Optimal International Portfolio Suppose you are a financial adviser and your client, who is currently investing only in the U.S. stock market, is considering diversifying into the U.K. stock market. At the moment, there are neither particular barriers nor restrictions on investing in the U.K. stock market. Your client would like to know what kinds of benefits can be expected from doing so. Using the data provided in problem 6, solve the following problems: 1. Graphically illustrate various combinations of portfolio risk and return that can be generated by investing in the U.S. and U.K. stock markets with different proportions. Two extreme proportions are (a) investing 100 percent in the United States with no position in the U.K. market, and (b) investing 100 percent in the U.K. market with no position in the U.S. market. 2. Solve for the optimal international portfolio comprising the U.S. and U.K. markets. Assume that the monthly risk-free interest rate is 0.5 percent and that investors can take a short (negative) position in either market. This problem can be solved using the spreadsheet MPTSolver.xIs. 3. What is the extra return that U.S. investors can expect to capture at the U.S. equivalent risk level? Also trace out the efficient set. A Appendix 15.B provides an example. 6. Suppose we obtain the following data in dollar terms: MINI CASE INSTRUCTIONS FOR SOLVING FOR THE OPTIMAL INTERNATIONAL PORTFOLIO (Note these instructions are identical to the case in the book, but more detailed) 1) USING THE DATA BELOW CALCULATE la through ld DATA \begin{tabular}{ccc|c|c} SIOCK HARKEI & \multicolumn{2}{c}{ RETURN IHEAN } & BISKISDI & GINVESTED \\ \hline UNITED STATES (H1) & 0.0126 & PER MONTH & 4.43 & 0.50 \\ \hline UNITED KINGDOM (H2) & 0.0123 & PER MONTH & 5.55 & 0.50 \\ \hline CORRELATION COEFF. & 0.58 & & & \end{tabular} RISK FREE RATE 0.005 1a) EXPECTED RETURN (using 50%150% ) 1b) STANDARD DEVATION OF PORTFOLIO (using 50\%150\%) Ic) VARIANCE US MARKET Id) VARIANCE UK MARKET 2) USING THE 5 COMBINATIONS OF WEIGHTS BELOW calculate RISK AND RETURN OF ALTERNATIVE PORTFOLIO COMBINATIONS 2a) GRAPHICALLY PLOT ALTERNATIVE PORTFOLIO COMBINATIONS OF RISK AND RETURN 3) SOLVE FOR THE OPTIMAL INTERNATIONAL PORTFOLIO USING THE FORMULAS IN APPENDIX 15B xUs xUK 4) CALCULATE RISK AND EXPECTED RETURN OF OIP EXPECTED RETURN using optimal international portfolio (DIP) veights RISK OF OIP (SLOPE OF EFFICIENT SET) 5) CALCULATE THE EXTRA RETURN FOR A US INVESTOR INVESTING IN OIP AT THE US RISK LEVEL Sharpe ratio(US) Sharpe ratio(OIP) EXTRARETURN on OIP at the US risk lerel =R=( Sharpe )xi,US=DOM

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts