Question: Solve in Matlab!! 3. In Problem 2, we can compute an option price, V, given an implied volatility, o. In this problem, we compute o

Solve in Matlab!!

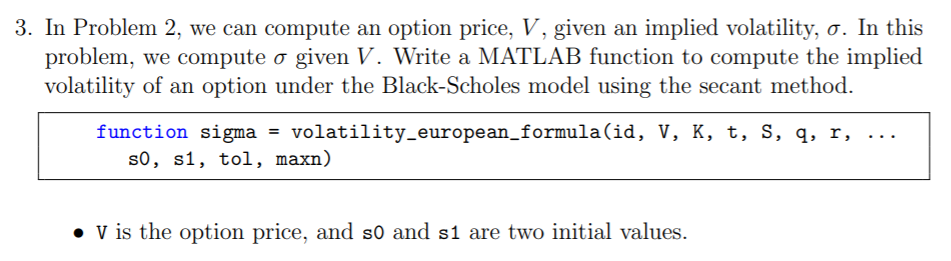

3. In Problem 2, we can compute an option price, V, given an implied volatility, o. In this problem, we compute o given V. Write a MATLAB function to compute the implied volatility of an option under the Black-Scholes model using the secant method. function sigma volatility_european_formula(id, V, K, t, s, q, r, so, s1, tol, maxn) V is the option price, and so and s1 are two initial values. 3. In Problem 2, we can compute an option price, V, given an implied volatility, o. In this problem, we compute o given V. Write a MATLAB function to compute the implied volatility of an option under the Black-Scholes model using the secant method. function sigma volatility_european_formula(id, V, K, t, s, q, r, so, s1, tol, maxn) V is the option price, and so and s1 are two initial values

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts