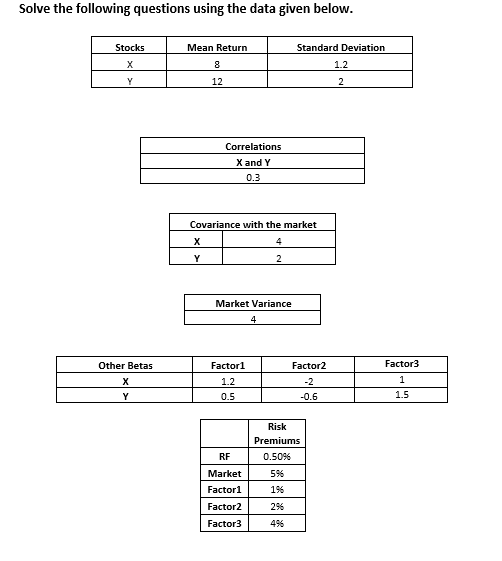

Solve the following questions using the data given below. Stocks X Y Other Betas X Y...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Corporate Finance

ISBN: 978-0077861759

10th edition

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe

Posted Date: