Question: solve the problem im stuck in the question Following data of two securities is available: Stock E(Ri) Std. Deviation A 10 08 B 20 .16

solve the problem im stuck in the question

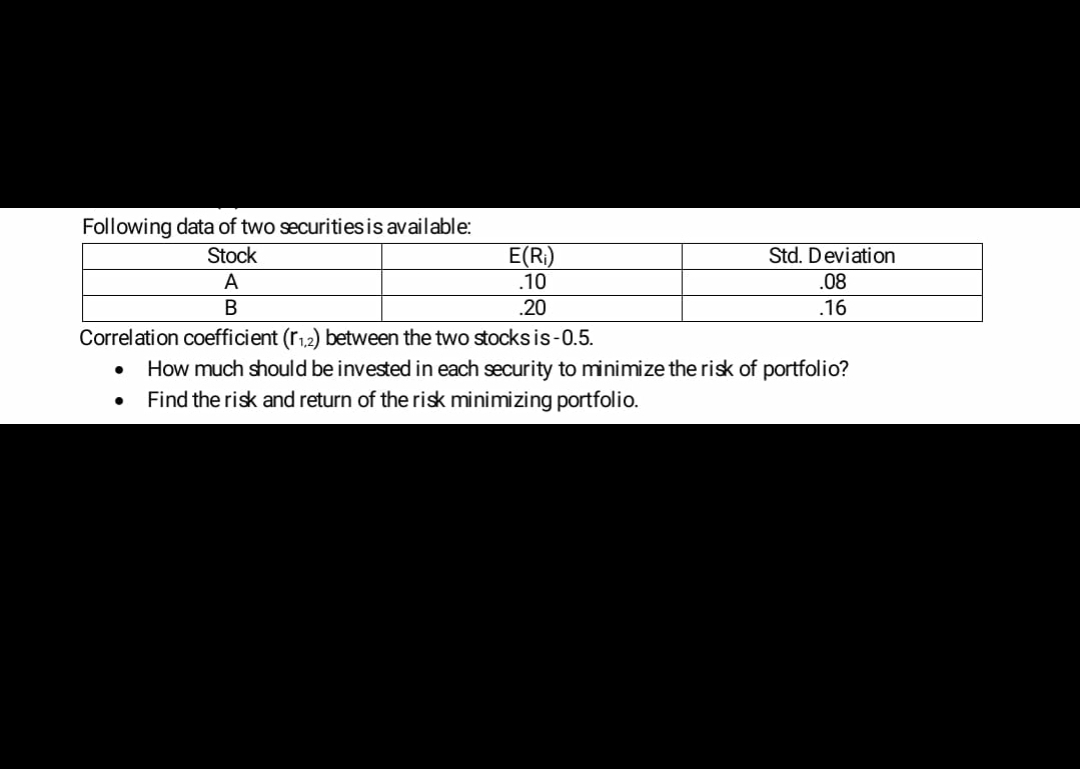

Following data of two securities is available: Stock E(Ri) Std. Deviation A 10 08 B 20 .16 Correlation coefficient (1 1,2) between the two stocks is -0.5. . How much should be invested in each security to minimize the risk of portfolio? . Find the risk and return of the risk minimizing portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock