Question: Solve the question below Let R; denote the return on security i given by the following multifactor model K; =di + bill + bal2 +

Solve the question below

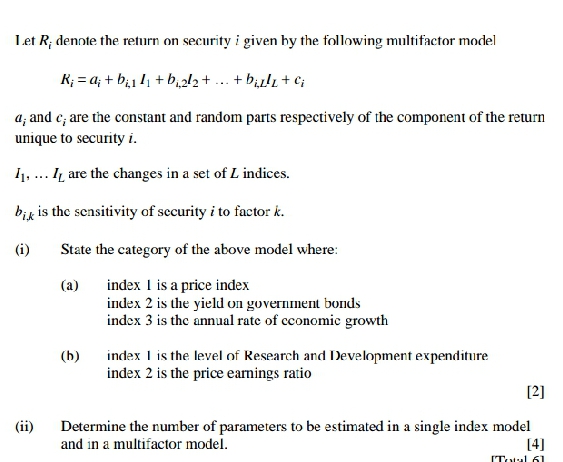

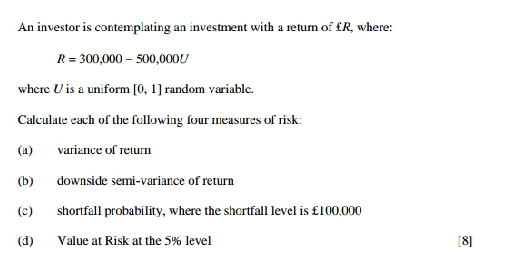

Let R; denote the return on security i given by the following multifactor model K; =di + bill + bal2 + ... + bizz + c; a; and c; are the constant and random parts respectively of the component of the return unique to security i. 1, ... It are the changes in a set of L indices. bax is the sensitivity of security i to factor k. (i) State the category of the above model where: (a) index I is a price index index 2 is the yield on government bonds index 3 is the annual rate of economic growth (b) index I is the level of Research and Development expenditure index 2 is the price earnings ratio [2] (ii) Determine the number of parameters to be estimated in a single index model and in a multifactor model. [4]An investor is contemplating an investment with a return of fR, where: R = 300,000 - 500,000U where U is a uniform [0. 1] random variable. Calculate each of the following four measures of risk: (H) variance of return (b) downside semi-variance of return (C) shortfall probability, where the shortfall level is $100,000 (d) Value at Risk at the 5% level [8]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts