Question: Solve the questions below. Consider the inverse demand function P = 6e'035'3. a. Use the total differential to nd the total derivative dTR/dQ, given the

Solve the questions below.

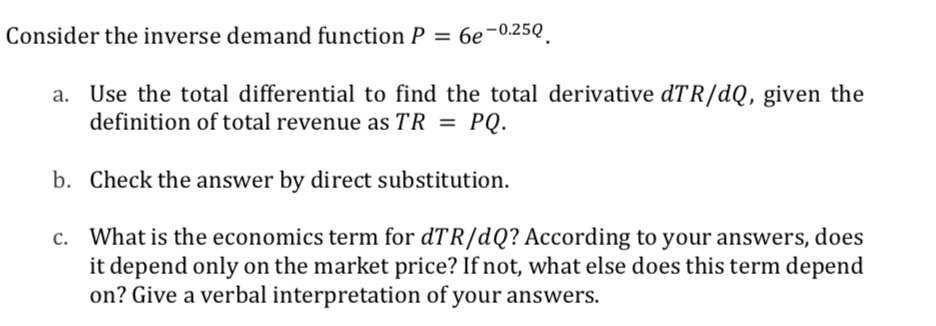

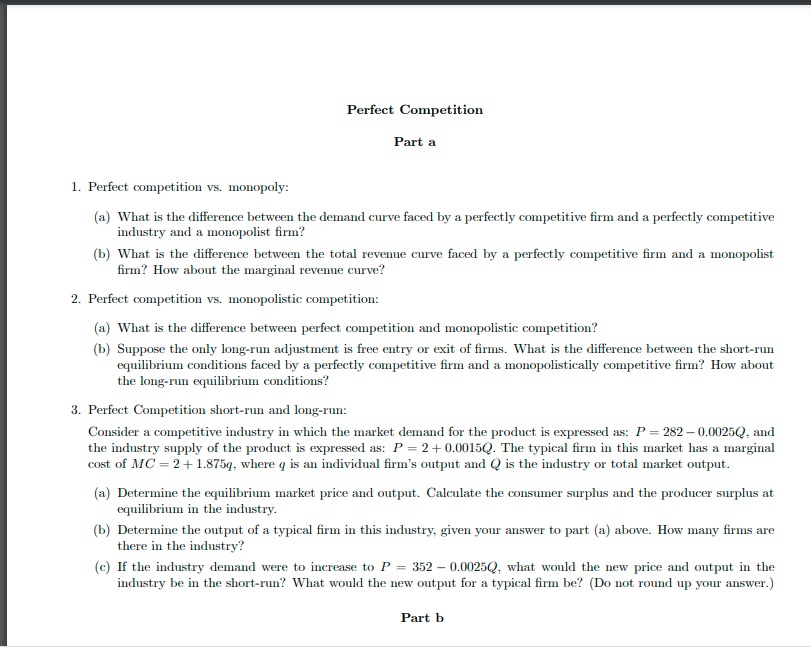

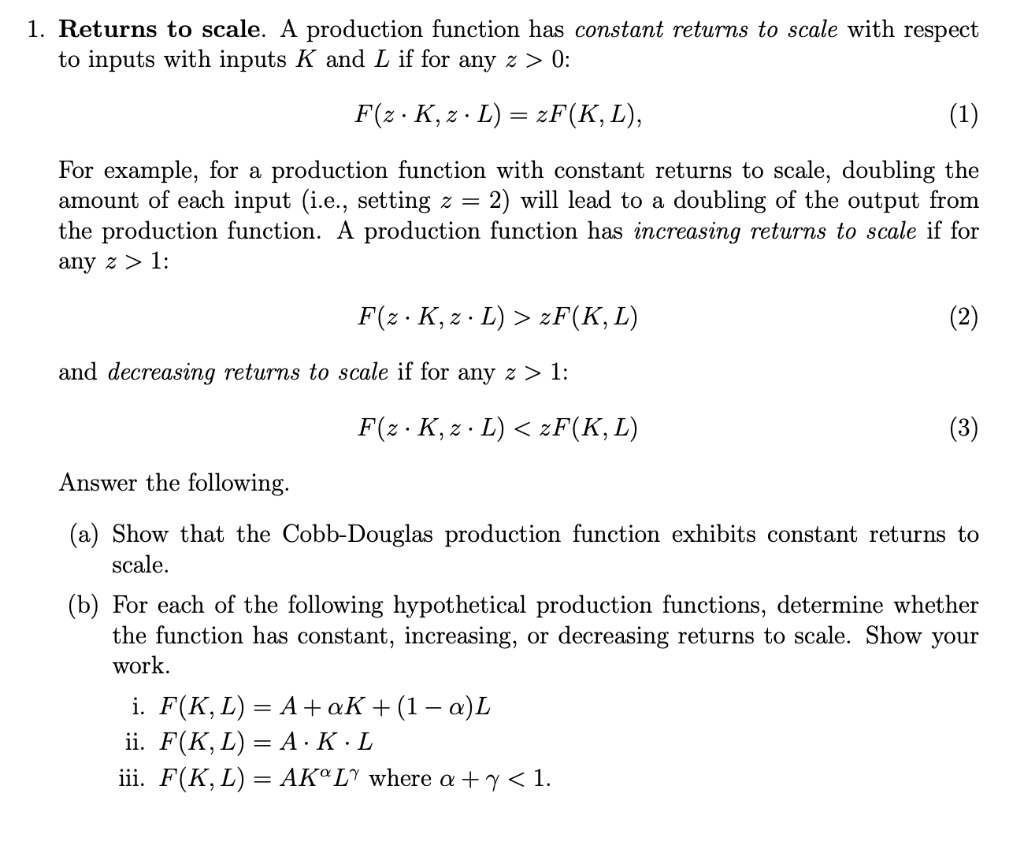

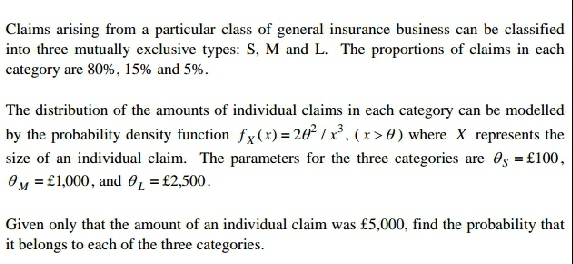

Consider the inverse demand function P = 6e'035'3. a. Use the total differential to nd the total derivative dTR/dQ, given the denition of total revenue as TR = PQ. b. Check the answer by direct substitution. c. What is the economics term for dTR [(1 Q? According to your answers, does it depend only on the market price? If not, what else does this term depend on? Give a verbal interpretation of your answers. Perfect Competition Part a 1. Perfect competition vs. monopoly: (a) What is the difference between the demand curve faced by a perfectly competitive firm and a perfectly competitive industry and a monopolist firm? (b) What is the difference between the total revenue curve faced by a perfectly competitive firm and a monopolist firm? How about the marginal revenue curve? 2. Perfect competition vs. monopolistic competition: (a) What is the difference between perfect competition and monopolistic competition? (b) Suppose the only long-run adjustment is free entry or exit of firms. What is the difference between the short-run equilibrium conditions faced by a perfectly competitive firm and a monopolistically competitive firm? How about the long-run equilibrium conditions? 3. Perfect Competition short-run and long-run: Consider a competitive industry in which the market demand for the product is expressed as: P = 282 -0.00250, and the industry supply of the product is expressed as: P = 2 + 0.00150. The typical firm in this market has a marginal cost of MC = 2 + 1.875q, where q is an individual firm's output and @ is the industry or total market output. (a) Determine the equilibrium market price and output. Calculate the consumer surplus and the producer surplus at equilibrium in the industry. (b) Determine the output of a typical firm in this industry, given your answer to part (a) above. How many firms are there in the industry? (c) If the industry demand were to increase to P = 352 - 0.0025@, what would the new price and output in the industry be in the short-run? What would the new output for a typical firm be? (Do not round up your answer.) Part b1. Returns to scale. A production function has constant returns to scale with respect to inputs with inputs K and L if for any z > 0: F( z . K, z . L) = zF( K, L), (1) For example, for a production function with constant returns to scale, doubling the amount of each input (i.e., setting z = 2) will lead to a doubling of the output from the production function. A production function has increasing returns to scale if for any z > 1: F ( z . K, z . L) > zF( K, L) (2) and decreasing returns to scale if for any z > 1: F( z . K, z . L) #) where X represents the size of an individual claim. The parameters for the three categories are 0, = $100, By = $1,000, and 07 = 12,500. Given only that the amount of an individual claim was f5,000, find the probability that it belongs to each of the three categories.Claims arising from a particular class of general insurance business can be classified into three mutually exclusive types: S. M and L. The proportions of claims in each category are 80%, 15% and 5%. The distribution of the amounts of individual claims in each category can be modelled by the probability density function fo(x)=20-/ x*, (x > #) where X represents the size of an individual claim. The parameters for the three categories are 0, = $100, By = $1,000, and 07 = 12,500. Given only that the amount of an individual claim was f5,000, find the probability that it belongs to each of the three categories

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts