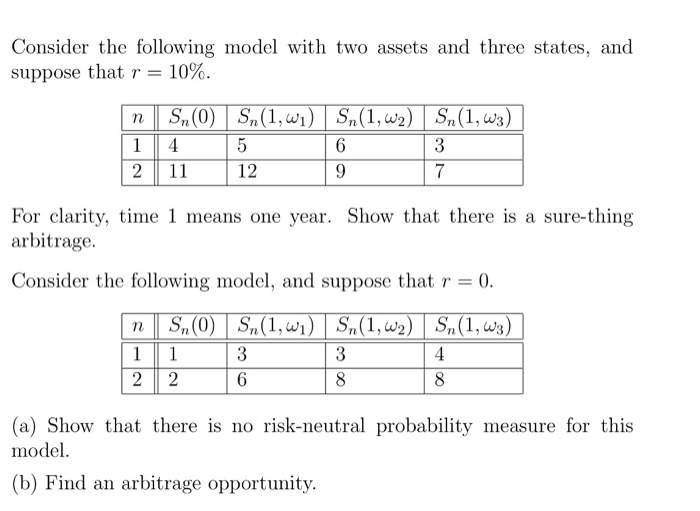

Question: some question about arbitrage Consider the following model with two assets and three states, and suppose that r-10%. 6 2 11 12 7 For clarity,

Consider the following model with two assets and three states, and suppose that r-10%. 6 2 11 12 7 For clarity, time 1 means one year. Show that there is a sure-thing arbitrage. Consider the following model, and suppose that r = 0. 6 (a) Show that there is no risk-neutral probability measure for this model (b) Find an arbitrage opportunity. Consider the following model with two assets and three states, and suppose that r-10%. 6 2 11 12 7 For clarity, time 1 means one year. Show that there is a sure-thing arbitrage. Consider the following model, and suppose that r = 0. 6 (a) Show that there is no risk-neutral probability measure for this model (b) Find an arbitrage opportunity

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts