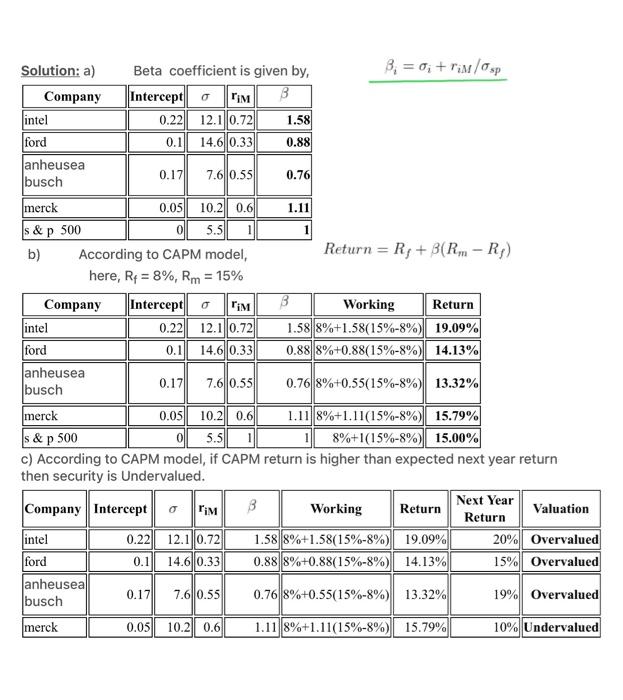

Question: sorry I accidentally post this. can you please cancel this try? Please explain how part (a) should be l calculated. Solution: a) Beta coefficient is

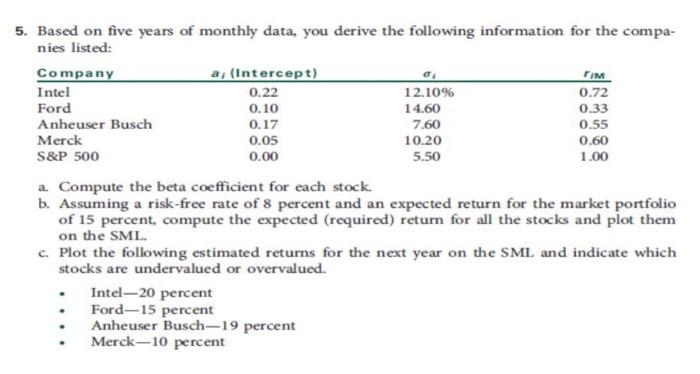

Solution: a) Beta coefficient is given by, i=i+riM/sp b) According to CAPM model, Return=Rf+(RmRf) here, Rf=8%,Rm=15% c) According to CAPM model, if CAPM return is higher than expected next year return then security is Undervalued. Based on five years of monthly data, you derive the following information for the companies listed: a. Compute the beta coefficient for each stock. b. Assuming a risk-free rate of 8 percent and an expected return for the market portfolio of 15 percent, compute the expected (required) return for all the stocks and plot them on the SML. c. Plot the following estimated returns for the next year on the SML and indicate which stocks are undervalued or overvalued. - Intel-20 percent - Ford-15 percent - Anheuser Busch-19 percent - Merck-10 percent

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts