Question: Specifically need help with D , E , F , I've already answered A , B , C . A = $ 1 , 0

Specifically need help with D E F I've already answered ABC

A $

B $

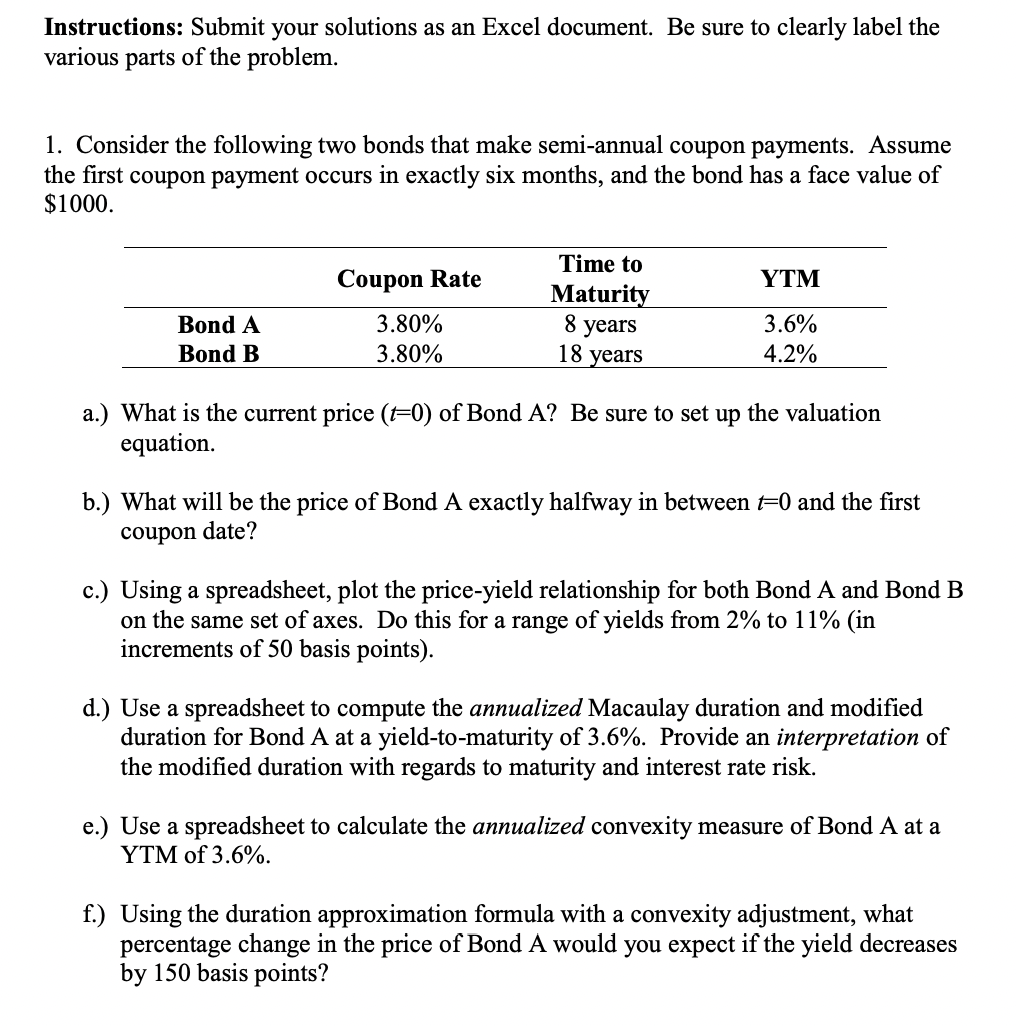

Submit your solutions as an Excel document. Be sure to clearly label the

various parts of the problem.

Consider the following two bonds that make semiannual coupon payments. Assume

the first coupon payment occurs in exactly six months, and the bond has a face value of

$

a What is the current price of Bond A Be sure to set up the valuation

equation.

b What will be the price of Bond A exactly halfway in between and the first

coupon date?

c Using a spreadsheet, plot the priceyield relationship for both Bond A and Bond B

on the same set of axes. Do this for a range of yields from to in

increments of basis points

d Use a spreadsheet to compute the annualized Macaulay duration and modified

duration for Bond A at a yieldtomaturity of Provide an interpretation of

the modified duration with regards to maturity and interest rate risk.

e Use a spreadsheet to calculate the annualized convexity measure of Bond A at a

YTM of

f Using the duration approximation formula with a convexity adjustment, what

percentage change in the price of Bond A would you expect if the yield decreases

by basis points?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock