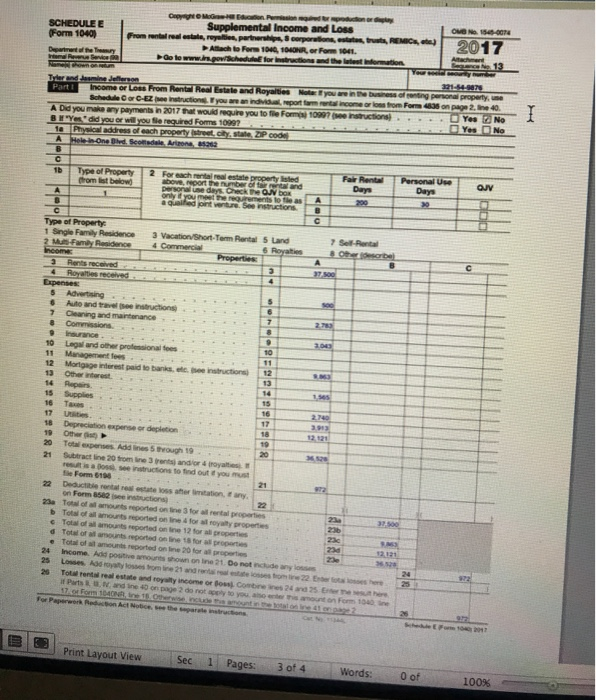

Question: Spilker Chapter 14 assignment, due 1007 up to 3 points, default grade for good/acceptable work is 2.55 points (B) This assignment builds on some of

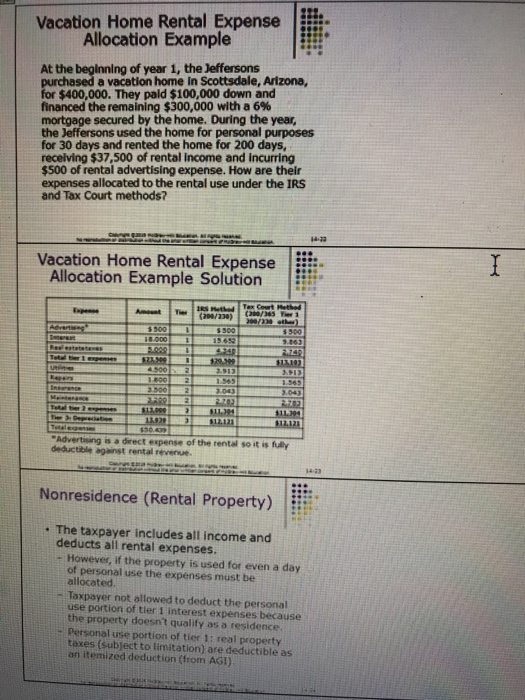

Spilker Chapter 14 assignment, due 1007 up to 3 points, default grade for good/acceptable work is 2.55 points (B) This assignment builds on some of the concepts in the Chs MC set relating to rental of vacation homes. Actually the same concepts also apply for rental of your own home for Airbnb. When you rent out your home for more than 14 days per year, you have to declare your income and may have to pay taxes. However, it is not as bad as it sounds. This is because certain costs of running a home that would otherwise not be deductible, such as utilities and insurance, become partially deductible when the home is used to produce rental income. The textbook on page 14-18 (see PPTS below) gives an example of a home that generated $37,500 of rental income. As schedule E (exhibit 14-5, page 14-20, copied below) shows, the total income reported from these rents is only $972. It actually gets even better. The taxpayer can still itemize thousands of additional interest and real property tax deductions on Schedule A (almost as much as if the home was not used for rent). There are actually two allowable methods to calculate rental income. The method used here is the Tax Court Method. The other method is the IRS Method. The IRS Method actually results in zero rental income but allows less additional itemized deductions. The logic of the Tax Court method is that interest and real-estate taxes should be allocated based on the percentage of the whole year rather than the percentage of actual use. To understand the background: the IRS wanted to give a bigger deduction for interest and taxes, but the taxpayer successfully appealed to the tax court to lower the deduction. Why would the taxpayer do that? The answer is that the remainder of the interest and taxes would have been deducted anyway as an itemized deduction on schedule A. The advantage of the Tax Court Method is that it increases income before depreciation, therefore allowing a larger depreciation deduction (depreciation cannot be taken as an itemized deduction on schedule A). You do not need to know the details, but what you should understand is that the IRS method calculates the percentage of rental use based on the number of days the building is actually occupied. On the other hand, the Tax Court Method is based on 365 days. Therefore the IRS Method applies a greater percentage of the costs to the rental revenue. The result is that under the IRS method you report lower rental income (usually zero). However, you also have less itemized deductions than under the Tax Court Method. Questions: Questions: 1. If a property is available for rent 200 days and is used for personal purposes 30 days, what is the percentage used for rental under (a) IRS Method and (b) Tax Court Method? 2. Which method will result in lower rental income on line 26 of schedule E, and why? 3. Which method will give you more itemized deductions, and why? 4. Which method will you likely use if you take the standard deduction, and why? 5. (Optional) Which method will you likely use if you itemized deductions and paid more than $10,000 in state and local income taxes, and why (hint: TCJA) SCHEDULE E Form 1040) COM Supplemental Income and Loss From rental real estate, r es partes, corporations, state, REMIC Allach to For 106, 100NR, or for 1041 Go to www.rgowichedule for const ant Wormation OMB No 1540- 2017 Ben Tyler anderine Jersen 321-44-9078 Part Income or Les From Rental Real Estate and Royalties Mote you are inte ressofonong personal property Schedule Corcere instruction, you are an individ porta t a income or from for 495 on page 2 ne 40 A Did you make any payments in 2017 that would require you to fee Form 10997 e instructions Yes No BW "Yes" did you or will you se required Forms 1099? Yes No 10 Physical address of each property street.citysta ZIP code A Hole in-One Bed Setdale, Arton 22 Type of Property Thomist below) 2 For each t e state property listed above, report the number of ro n d personal use days. Check T ONDOK only you moeterguruments to as a fied joint venture See instructions A 3 DOO Type of Property 1 Single Family Residence 2 MS Family Residence 3 Vacation Short Term Rental 4 Commercia and Royal 7 Se Rent Rents received Lupenses 5 Advertising 6 Auto and le ction Cleaning and maintenance 8 Commissions 10 Legs and other profesionales 11 Management 12 Mortgage interest paid to bank 13 Other interest 14 Repas 15 Supplies 16 Taxes 17 U 18 Depron expense or deletion 19 Other 20 To n Add nes 5 rough 19 21 Subtractine 20 trominer andorry a is c tions to find out you must Form 6196 22 Ded o s hermation any on Form 52 se ctions 23 Too t ed on to a real properties Tots of amounts or online for properties Total amounts reported on line 12 for properties Total of a mounts reported online for properties Total o u ported on 20 for a proporties 24 income Add powe r shown on line 21. Do not include any loss 888888 12121 26 Torrestate and royalty income or Boscone w Parts and line on page 2 note to you 24 and 25 Eu r ont on Form 100 in Print Layout View Sec 1 Pages: 3 of 4 Words: O of 100% Vacation Home Rental Expense Allocation Example At the beginning of year 1, the Jeffersons purchased a vacation home in Scottsdale, Arizona, for $400,000. They pald $100,000 down and financed the remaining $300,000 with a 6% mortgage secured by the home. During the year, the Jeffersons used the home for personal purposes for 30 days and rented the home for 200 days, receiving $37,500 of rental income and incurring $500 of rental advertising expense. How are their expenses allocated to the rental use under the IRS and Tax Court methods? Vacation Home Rental Expense Allocation Example Solution Advertising is a direct expense of the rental so it is fully deductible against rental revenue Nonresidence (Rental Property) The taxpayer includes all income and deducts all rental expenses. However, if the property is used for even a day of personal use the expenses must be allocated Taxpayer not allowed to deduct the personal use portion of tier 1 interest expenses because the property doesn't qualify as a residence Personal use portion of tier 1: real property taxes (subject to limitation) are deductible as an itemized deduction (from AGI) Spilker Chapter 14 assignment, due 1007 up to 3 points, default grade for good/acceptable work is 2.55 points (B) This assignment builds on some of the concepts in the Chs MC set relating to rental of vacation homes. Actually the same concepts also apply for rental of your own home for Airbnb. When you rent out your home for more than 14 days per year, you have to declare your income and may have to pay taxes. However, it is not as bad as it sounds. This is because certain costs of running a home that would otherwise not be deductible, such as utilities and insurance, become partially deductible when the home is used to produce rental income. The textbook on page 14-18 (see PPTS below) gives an example of a home that generated $37,500 of rental income. As schedule E (exhibit 14-5, page 14-20, copied below) shows, the total income reported from these rents is only $972. It actually gets even better. The taxpayer can still itemize thousands of additional interest and real property tax deductions on Schedule A (almost as much as if the home was not used for rent). There are actually two allowable methods to calculate rental income. The method used here is the Tax Court Method. The other method is the IRS Method. The IRS Method actually results in zero rental income but allows less additional itemized deductions. The logic of the Tax Court method is that interest and real-estate taxes should be allocated based on the percentage of the whole year rather than the percentage of actual use. To understand the background: the IRS wanted to give a bigger deduction for interest and taxes, but the taxpayer successfully appealed to the tax court to lower the deduction. Why would the taxpayer do that? The answer is that the remainder of the interest and taxes would have been deducted anyway as an itemized deduction on schedule A. The advantage of the Tax Court Method is that it increases income before depreciation, therefore allowing a larger depreciation deduction (depreciation cannot be taken as an itemized deduction on schedule A). You do not need to know the details, but what you should understand is that the IRS method calculates the percentage of rental use based on the number of days the building is actually occupied. On the other hand, the Tax Court Method is based on 365 days. Therefore the IRS Method applies a greater percentage of the costs to the rental revenue. The result is that under the IRS method you report lower rental income (usually zero). However, you also have less itemized deductions than under the Tax Court Method. Questions: Questions: 1. If a property is available for rent 200 days and is used for personal purposes 30 days, what is the percentage used for rental under (a) IRS Method and (b) Tax Court Method? 2. Which method will result in lower rental income on line 26 of schedule E, and why? 3. Which method will give you more itemized deductions, and why? 4. Which method will you likely use if you take the standard deduction, and why? 5. (Optional) Which method will you likely use if you itemized deductions and paid more than $10,000 in state and local income taxes, and why (hint: TCJA) SCHEDULE E Form 1040) COM Supplemental Income and Loss From rental real estate, r es partes, corporations, state, REMIC Allach to For 106, 100NR, or for 1041 Go to www.rgowichedule for const ant Wormation OMB No 1540- 2017 Ben Tyler anderine Jersen 321-44-9078 Part Income or Les From Rental Real Estate and Royalties Mote you are inte ressofonong personal property Schedule Corcere instruction, you are an individ porta t a income or from for 495 on page 2 ne 40 A Did you make any payments in 2017 that would require you to fee Form 10997 e instructions Yes No BW "Yes" did you or will you se required Forms 1099? Yes No 10 Physical address of each property street.citysta ZIP code A Hole in-One Bed Setdale, Arton 22 Type of Property Thomist below) 2 For each t e state property listed above, report the number of ro n d personal use days. Check T ONDOK only you moeterguruments to as a fied joint venture See instructions A 3 DOO Type of Property 1 Single Family Residence 2 MS Family Residence 3 Vacation Short Term Rental 4 Commercia and Royal 7 Se Rent Rents received Lupenses 5 Advertising 6 Auto and le ction Cleaning and maintenance 8 Commissions 10 Legs and other profesionales 11 Management 12 Mortgage interest paid to bank 13 Other interest 14 Repas 15 Supplies 16 Taxes 17 U 18 Depron expense or deletion 19 Other 20 To n Add nes 5 rough 19 21 Subtractine 20 trominer andorry a is c tions to find out you must Form 6196 22 Ded o s hermation any on Form 52 se ctions 23 Too t ed on to a real properties Tots of amounts or online for properties Total amounts reported on line 12 for properties Total of a mounts reported online for properties Total o u ported on 20 for a proporties 24 income Add powe r shown on line 21. Do not include any loss 888888 12121 26 Torrestate and royalty income or Boscone w Parts and line on page 2 note to you 24 and 25 Eu r ont on Form 100 in Print Layout View Sec 1 Pages: 3 of 4 Words: O of 100% Vacation Home Rental Expense Allocation Example At the beginning of year 1, the Jeffersons purchased a vacation home in Scottsdale, Arizona, for $400,000. They pald $100,000 down and financed the remaining $300,000 with a 6% mortgage secured by the home. During the year, the Jeffersons used the home for personal purposes for 30 days and rented the home for 200 days, receiving $37,500 of rental income and incurring $500 of rental advertising expense. How are their expenses allocated to the rental use under the IRS and Tax Court methods? Vacation Home Rental Expense Allocation Example Solution Advertising is a direct expense of the rental so it is fully deductible against rental revenue Nonresidence (Rental Property) The taxpayer includes all income and deducts all rental expenses. However, if the property is used for even a day of personal use the expenses must be allocated Taxpayer not allowed to deduct the personal use portion of tier 1 interest expenses because the property doesn't qualify as a residence Personal use portion of tier 1: real property taxes (subject to limitation) are deductible as an itemized deduction (from AGI)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts