Question: Spreadsheet Problem 26. Markowitz Efficient Frontier (LO4, CFA5) Assume you are evaluating two stocks, Stock A and Stock B. Stock A has an expected return

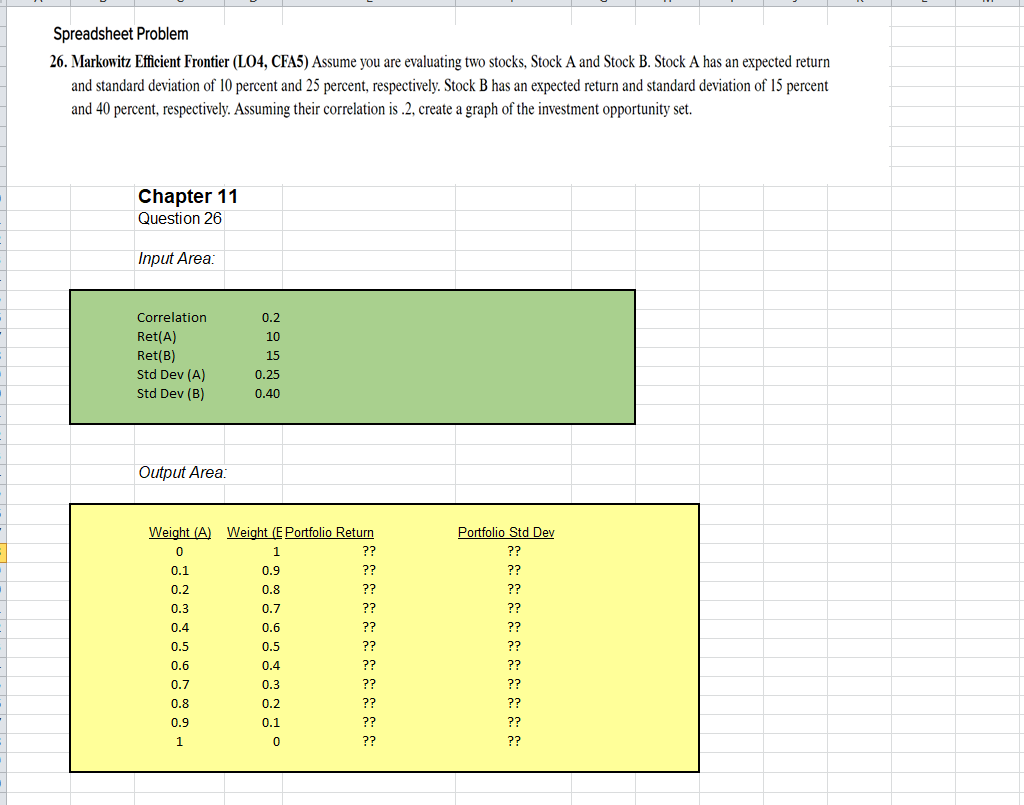

Spreadsheet Problem 26. Markowitz Efficient Frontier (LO4, CFA5) Assume you are evaluating two stocks, Stock A and Stock B. Stock A has an expected return and standard deviation of 10 percent and 25 percent, respectively. Stock B has an expected return and standard deviation of 15 percent and 40 percent, respectively. Assuming their correlation is.2, create a graph of the investment opportunity set. Chapter 11 Question 26 Input Area: Correlation Ret(A) Ret(B) Std Dev (A) Std Dev (B) 0.2 10 15 0.25 0.40 Output Area: Weight (A) Weight (E Portfolio Return 0 1 ?? 0.1 0.9 ?? 0.2 0.8 ?? 0.3 0.7 ?? 0.4 0.6 ?? 0.5 0.5 ?? 0.6 0.4 ?? 0.7 0.3 ?? 0.8 0.2 ?? 0.9 0.1 ?? 1 0 ?? Portfolio Std Dev

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts