Question: Statement /: The growth in total factor productivity is not directly observable. Statement 2: The growth factors must be stated in nominal (i.e., not inflation-adjusted)

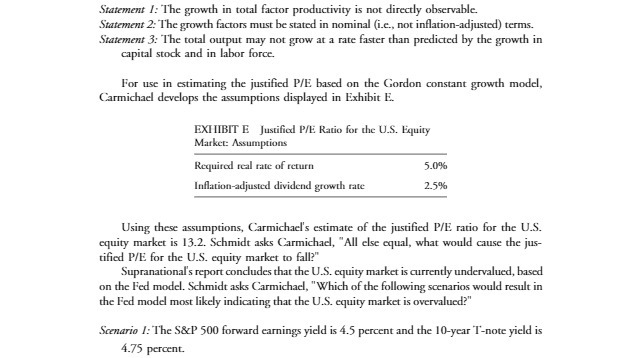

Statement /: The growth in total factor productivity is not directly observable. Statement 2: The growth factors must be stated in nominal (i.e., not inflation-adjusted) terms. Statement 3: The total output may not grow at a rate faster than predicted by the growth in capital stock and in labor force. For use in estimating the justified P/E based on the Gordon constant growth model, Carmichael develops the assumptions displayed in Exhibit E. EXIIIBIT E Justified P/E Ratio for the U.S. Equity Market: Assumptions Required real rate of return 5.0% Inflation-adjusted dividend growth rate 2.5% Using these assumptions, Carmichael's estimate of the justified P/E ratio for the U.S. equity market is 13.2. Schmidt asks Carmichael, "All else equal, what would cause the jus- tified P/E for the U.S. equity market to fall?" Supranational's report concludes that the U.S. equity market is currently undervalued, based on the Fed model. Schmidt asks Carmichael, "Which of the following scenarios would result in the Fed model most likely indicating that the U.S. equity market is overvalued?" Scenario /: The S&P 500 forward earnings yield is 4.5 percent and the 10-year T-note yield is 4.75 percent

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts