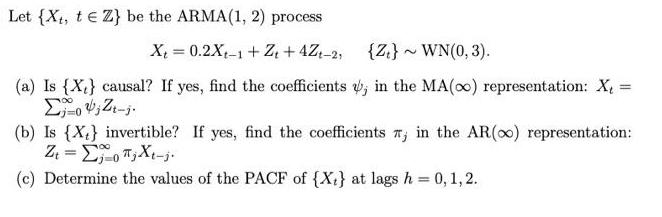

Question: Let {X4, t Z} be the ARMA(1, 2) process X = 0.2X,-1+ Z, + 4Z-2, {Z.}~WN(0, 3). (a) Is {X} causal? If yes, find

Let {X4, t Z} be the ARMA(1, 2) process X = 0.2X,-1+ Z, + 4Z-2, {Z.}~WN(0, 3). (a) Is {X} causal? If yes, find the coefficients v, in the MA(oo) representation: X, = %3D (b) Is {X} invertible? If yes, find the coefficients n; in the AR(0) representation: Z = Eo T,Xi-j. (c) Determine the values of the PACF of {X:} at lags h = 0, 1, 2.

Step by Step Solution

★★★★★

3.37 Rating (153 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

check the answer i have given below Let Xt EE2 ARMA ... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock