Question: Let (N, F, P) be a probability space and Fn a filtration. Sup- pose that (Xn, Fn) and (Yn, Fn) are martingales and T

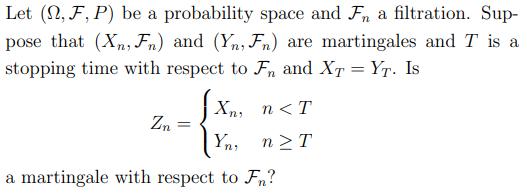

Let (N, F, P) be a probability space and Fn a filtration. Sup- pose that (Xn, Fn) and (Yn, Fn) are martingales and T is a stopping time with respect to Fn and XT = YT. Is %3D Xn, n T a martingale with respect to Fn?

Step by Step Solution

★★★★★

3.35 Rating (164 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock