Question: Step 2:Record the 11 adjusting journal entries based on the information below. Record all AJE's on the Excel spreadsheet using the tab labeled AJEs and

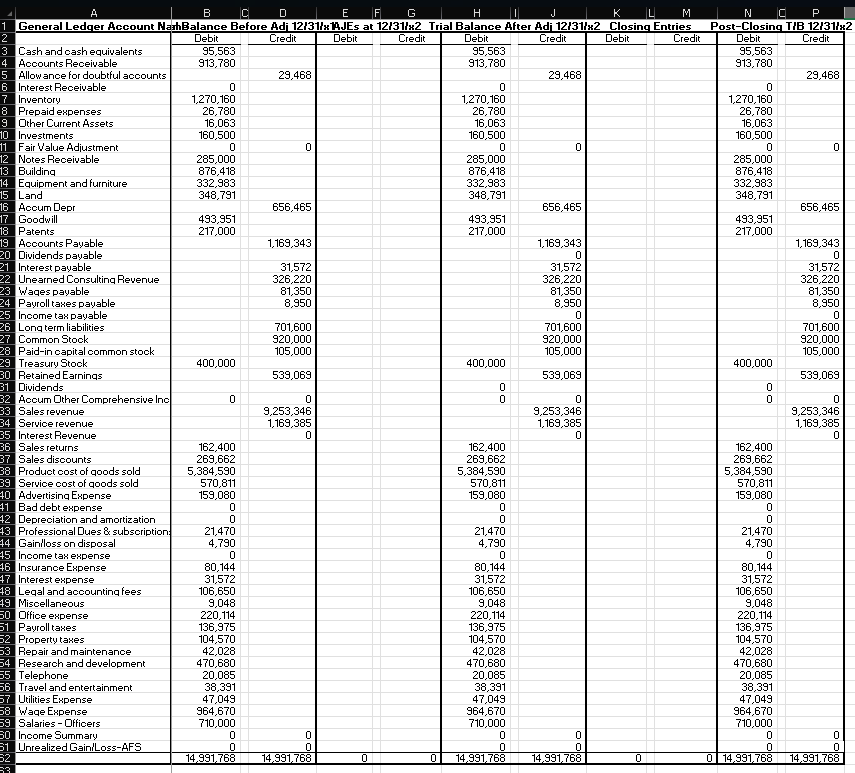

Step 2:Record the 11 adjusting journal entries based on the information below. Record all AJE's on the Excel spreadsheet using the tab labeled "AJEs and Closing Entries." Post to the Trial Balance (second tab at the bottom of the spreadsheet) in the two columns labeled AJE's (Columns E & G). SC uses a perpetual inventory system, which means that when they record the sale of a product (at the selling price), they also update COGS and Inventory (at cost). Recommendation: use cell referencing when posting to the Trial Balance to eliminate potential typos and follow-through errors.

Step 3: Once all AJE's have been recorded & posted to the Trial Balance, check your work with the "CHECK FIGURES FOR Accounting Cycle Project." If your spreadsheet agrees with the Check Figures, you can move to Step 4.

Step 4: Record the 5 Closing entries on the tab labeled "AJE's & Closing." Post to the Trial Balance in columns K & M.

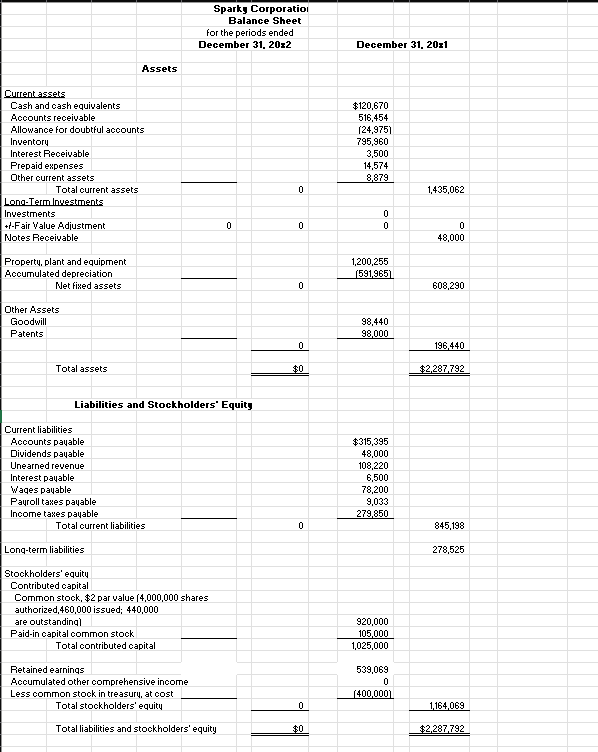

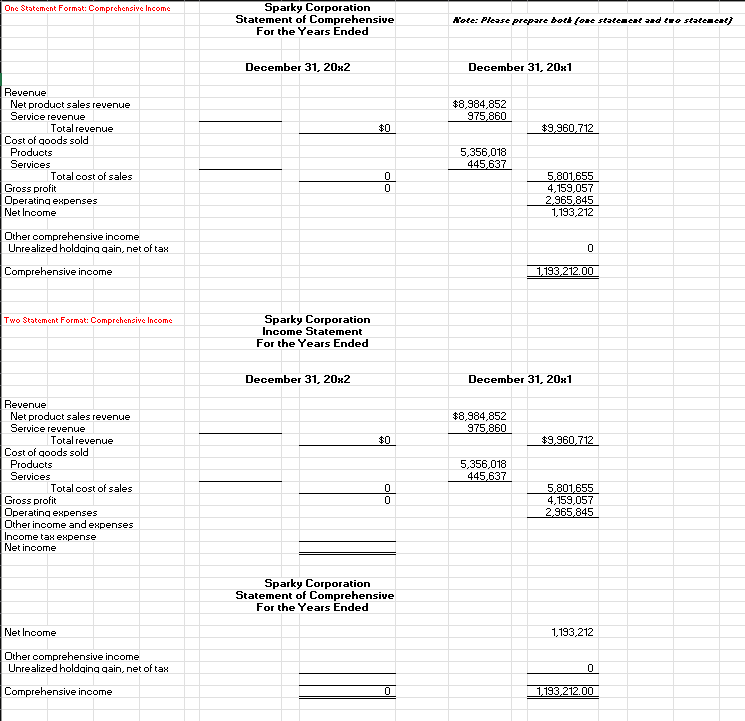

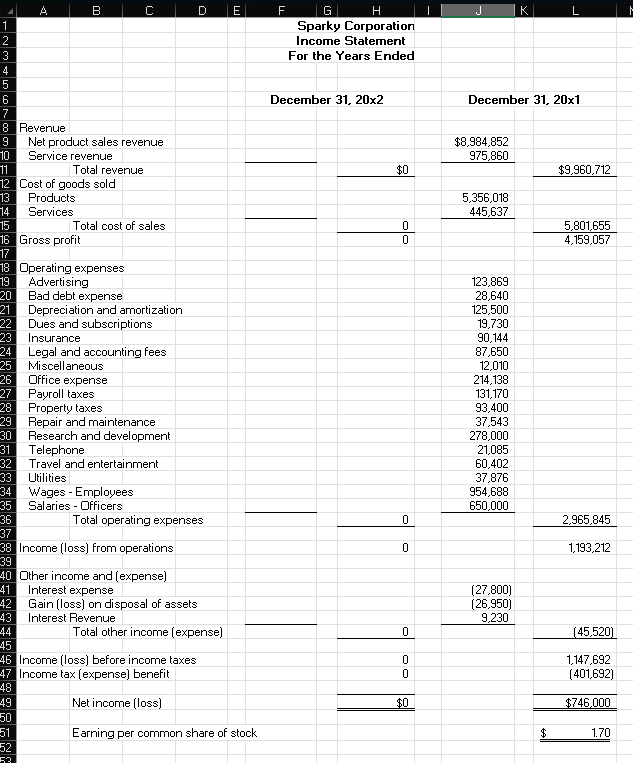

Step 5: Complete the Income Statement, Comprehensive Income Statement, Statement of Retained Earnings, and Balance Sheet in good form.

Step 6: Once all financial statements are complete, you can answer the questions in Canvas labeled Accounting Cycle Project-Sparky Corporation (i.e., Quiz). You do not have to submit your Excel file; use the information to answer the questions. You will have two un-timed attempts.

Additional information to use in recording the necessary Adjusting Journal Entries (AJE's):

1. As of December 31, wages of $39,800 should be accrued; associated payroll taxes on these wages are $2,900. (Record in two separate adjusting entries. The payroll taxes are an expense to the company for unemployment benefits and are recorded as payroll taxes payable to the state & federal taxing authority.) 2. The Unearned Consulting Revenue account has a balance before adjustment of $326,220 as of December 31, 20x2. Of this balance, 65% of the work was completed by year-end. 3. You discover that a sale of a product was made on the account and SC recorded the sale in December for $86,400. However, the product has not yet been shipped, therefore it is not considered to be "delivered to the customer." The cost of the product was 55% of its selling price. SC uses the perpetual inventory method. (Simply reverse the original journal entry!) 4. At year-end, the CFO asks you to review the Accounts Receivables to determine if any customer accounts should be written off as uncollectible. Based on your review, you determine that the Account Receivable from Shift, Co. has been past due for over 18 months, and Shift recently declared bankruptcy. The CFO instructs you to write off the account balance of $18,450. Directly following this action, you can now record bad debt expense, estimated to be 5% of ending Accounts Receivable. (Round to the nearest whole dollar.) 5. SC prepays for its property & casualty insurance. As of December 31, 20x2, 80% of the prepayments have now been consumed. (Round to the nearest whole dollar.) 6. SC records depreciation and amortization expenses annually. They do not use an accumulated amortization account. (i.e., Amortization Expense is recorded with a debit to Amort. Exp and a credit to the Patent.) Annual depreciation rates are 5% for Buildings/Equipment/Furniture, with no salvage. (Round to the nearest whole dollar.) Annual Amortization rates are 10% of the original cost, straight- line method, no salvage. SC owns two patents: Patent #FJ101 has an original cost of $154,000, and Patent #CQ510 was acquired for $169,000. The last time depreciation & amortization were recorded was December 31, 20x1. 7. The long-term liabilities were outstanding for all of 20x1 and accrue interest at 6% APR. SC records accrued interest quarterly (interest was last updated on September 30.) The company is required to pay the interest annually each January 1. 8. SC often allows customers to finance the purchase of their products through long-term lending agreements and therefore reports Long-term Notes Receivable on their Balance Sheet. These notes are interest-bearing and earn SC interest revenue at 8% APR and were outstanding for all 20x2. Interest is payable to SC each January 1.

9. On December 15, SC declared a dividend of $220,000, to be paid on January 20, 20x3. The dividend declaration had not yet been recorded. Please record the debit to Dividends. 10. On December 31, the Long-Term Investments (Available-for-sale securities or "AFS") had a fair value of $172,900. The AFS Investment was initially purchased on June 1, 20x2, for $160,500. SC uses a "Fair Value Adjustment" account (an adjunct/contra account to the Investments) to mark-to-market the investment portfolio at year-end. (e.g., If the fair value of the Investment has increased at year-end, debit the Fair Value Adjustment account to increase the Carrying Value of the asset to equal its fair value on the balance sheet on December 31. This is an "unrealized" (holding) gain, which would require a credit to record it.) Note: See Chapter 3-Other Comprehensive Income to learn more about unrealized holding gains and comprehensive income statement. 11. SC's Income tax rate for 20x2 was determined to be 25%. (Hint: The income statement must be prepared to determine income tax expense!)

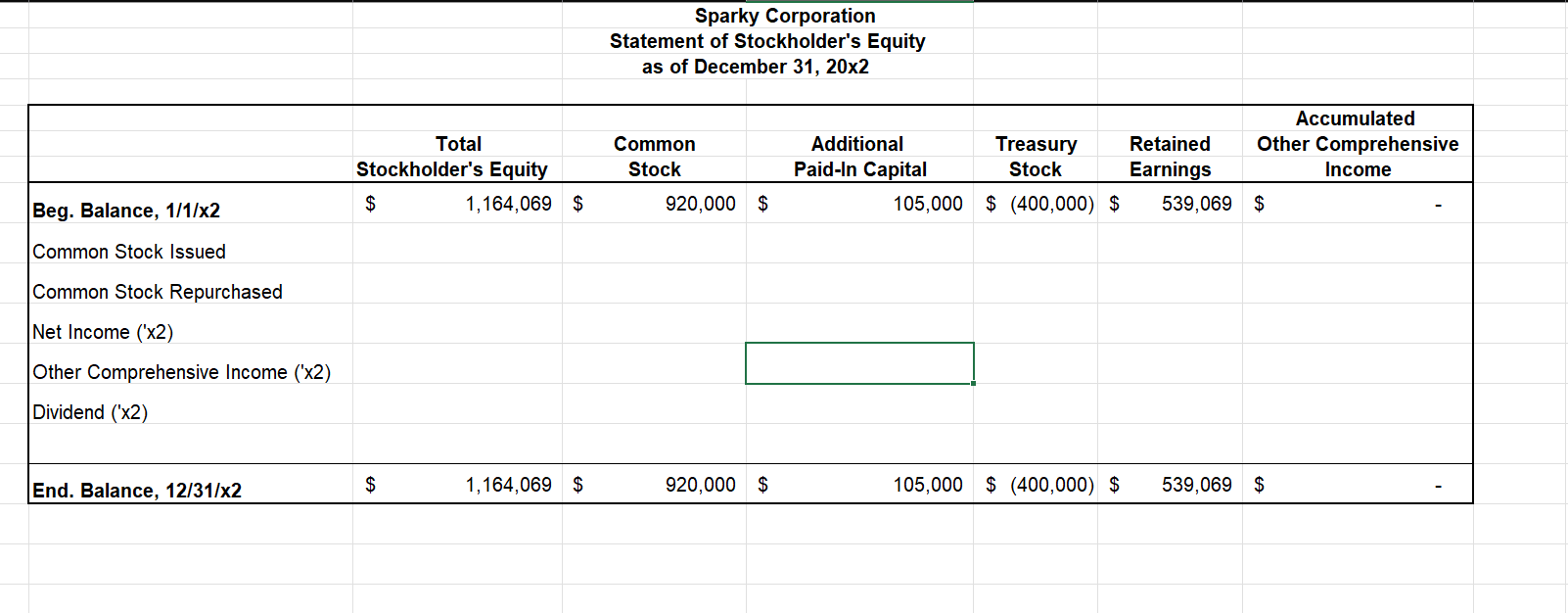

A B C E F G IH K AJE Account Name DB CB Closing Entries Account Name CB 2 2 3 4 5 6 7 8 9 5 10 11Sparky Corporation Balance Sheet for the periods ended December 31, 20:2 December 31. 20z1 Assets Current assets Cash and cash equivalents $120,670 Accounts receivable 516,454 Allowance for doubtful accounts [24,975) Inventory 795,960 Interest Receivable 3,500 Prepaid expenses 4.574 rrent assets 8.879 Total current assets 1,435,062 Long-Term Investments Investments +/-Fair Value Adjustment 0 0 Notes Receivable 48,000 Property, plant and equipment 1,200,255 Accumulated depreciation (591,965) Net fixed assets 608,290 Other Assets Goodwill 98,440 Patents 98,000 196,440 Total assets $0 $2 287,792 Liabilities and Stockholders' Equity Current liabilities Accounts payable $315,395 Dividends payable 48,000 Unearned revenue 108,220 Interest payable 6,500 Wages payable 78,200 Payroll taxes payable 9,03: Income taxes payable 279,850 Total current liabilities 845,198 Long-term liabilities 278,525 Stockholders equity Contributed capital Common stock, $2 par value (4,000,000 shares authorized,460,000 issued; 440,000 are outstandingl 920,000 Paid-in capital common stock 105,000 Total contributed capital 1,025,000 Retained earnings 539,069 Accumulated other comprehensive income Less common stock in treasury, at cost (400 000) Total stockholders' equity 0 1,164,069 Total liabilities and stockholders equity $0 $2,287,792One Statement Format: Comprehensive Income Sparky Corporation Statement of Comprehensive Note: Please prepare both fone statement and two statement) For the Years Ended December 31, 20*2 December 31, 20x1 Revenue Net product sales revenue $8,984.852 Service revenue 975.860 Total revenue FO $9.360.712 Cost of goods sold Products 5,356,018 Services 445.637 Total cost of sales 5.801.655 Gross profit 4,159,057 Operating expenses 2.965.845 Net Income 1,193,212 Other comprehensive income Unrealized holdging gain, net of tax Comprehensive income 1.193.212.00 Two Statement Format: Comprehensive Income Sparky Corporation Income Statement For the Years Ended December 31, 20:2 December 31, 20x1 Revenue Net product sales revenue $8,984.852 Service revenue 975.860 Total revenue $0 $9.960.712 Cost of goods sold Product 5,356,016 Services 445.637 Total cost of sales 5.801.655 Gross profit 4.159,057 Operating expenses 2.965.845 Other income and expenses Income tax expense Net income Sparky Corporation Statement of Comprehensive For the Years Ended Net Income 1,193,212 Other comprehensive income Unrealized holdging gain, net of tax Comprehensive income 1.193.212.00B C D E F G H J K Sparky Corporation Income Statement For the Years Ended December 31, 20x2 December 31, 20x1 Revenue Net product sales revenue $8.984.852 Service revenue 175.860 Total revenue $0 $9,960,712 Cost of goods sold Products 5.356.018 Services 445.637 Total cost of sales 5,801,655 Gross profit 4.159,057 Operating expenses Advertising 123,869 Bad debt expense 28,640 Depreciation and amortization 125,500 Ques and subscriptions 19,730 Insurance 90,144 Legal and accounting fees 87,650 Miscellaneous 12,010 Office expense 214.138 Payroll taxes 131,170 Property taxes 93.400 Repair and maintenance 37.543 Research and development 278,000 Telephone 21.085 Travel and entertainment 60,402 Utilities 37.876 Wages - Employees 354,688 Salaries - Officers 650,000 Total operating expenses 2.965.845 Income ( loss) from operations 0 1,193.212 Other income and [expense) Interest expense 27 800) Gain [loss] on disposal of assets (26,9501 Interest Revenue 9,230 Total other income [expense) [45.520) Income [loss) before income taxes 1,147.692 Income tax [expense) benefit [401,692) 19 Net income [ loss) $0 746 000 Earning per common share of stock $ 1.70Sparky Corporation Statement of Stockholder's Equity as of December 31, 20x2 Accumulated Total Common Additional Treasury Retained Other Comprehensive Stockholder's Equity Stock Paid-In Capital Stock Earnings Income Beg. Balance, 1/1/x2 $ 1,164,069 $ 920,000 % 105,000 $ (400,000) 5 539,069 $ - Common Stock Issued Common Stock Repurchased Net Income ('x2) Other Comprehensive Income ('x2) i Dividend ('x2) End. Balance, 12/31/x2 $ 1,164,069 $ 920,000 105,000 $ (400,000) $ 539,069 $ - B E F G H M N C P General Ledger Account NashBalance Before Adj 12131/x1JEs at 12131/x2 Trial Balance After Adj 12131/:2 Closing Entries Post-Closing TIB 12131/x2 Llebit redi Debit Credit Llebit Credit Debit Credit Debit Credit Cash and cash equivalents 95,563 95,563 95,563 Accounts Receivable 313,780 313.780 913.780 Allow ance for doubtful accounts 29,468 29,468 29,468 Interest Receivable Inventory 1,270.160 1,270,160 1,270,160 Prepaid expenses 26.780 26.780 26,780 Other Current Assets 16,063 16,063 16,063 Investments 160.500 160,500 160,500 Fair Value Adjustment 0 Notes Receivable 285,000 285,000 285,000 Building 876,418 876,413 876,418 Equipment and furniture 332.983 332,983 332,983 Land 348.791 348.791 348.791 Accum Lepr 656.465 656,465 656.465 Goodwill 493,951 493,951 493.951 Patents 217,000 217,000 217,000 Accounts Payable 1,169,343 1,169,343 1,169,343 Dividends payable Interest payable 31,572 31,572 31.572 Unearned Consulting Revenue 326,220 326,220 326.220 Wages payable 81,350 81,350 31.350 Payroll takes payable 8.950 8.950 8.950 Income tax payable Long term liabilities 701,600 701,600 701,600 Common Stock 920,000 920,001 320,000 Paid-in capital common stock 105,000 105,000 105,000 Treasury Stock 400,000 400,000 400,000 Retained Earnings 539,069 539,065 539,069 Dividends Accum Other Comprehensive Inc Sales revenue 9.253,346 3.253.346 3.253,346 Service revenue 1,169.385 1.169.385 1,169,385 nterest Revenue Sales returns 162.400 162,400 162,400 Sales discounts 263,662 269,662 269,662 Product cost of goods sold 5,384,590 5,384,590 5.384,530 Service cost of goods sold 570,811 570,811 570,811 Advertising Expense 159,080 159,080 159,080 Bad debt expense Depreciation and amortization 0 Professional Dues & subscription: 21,470 21,470 21,470 Gainiloss on disposal 4.790 4,790 4,790 Income tax expense Insurance Expense 30,144 80,144 80,144 Interest expense 31,572 31,572 31,572 Legal and accounting fees 06,650 106,650 106,650 Miscellaneous 9,048 9.048 9.048 Office expense 220,114 220,114 220,114 Payroll taxes 136,975 136,975 136,975 Property taxes 104.570 104,570 104,570 Repair and maintenance 42,028 42.028 42,028 Research and development 470,680 470,680 470,680 Telephone 20.085 20.085 20,085 Travel and entertainment 38,391 38,391 38,391 Utilities Expense 47,049 47,049 47,049 Wage Expense 364,670 964.670 964,670 Salaries - Officers 710,000 710,000 710,000 Income Summary Unrealized Gain Loss-AFS 14.991.768 14.931.768 14.991.768 14.931,768 0 14.991.768 14.991.768

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!