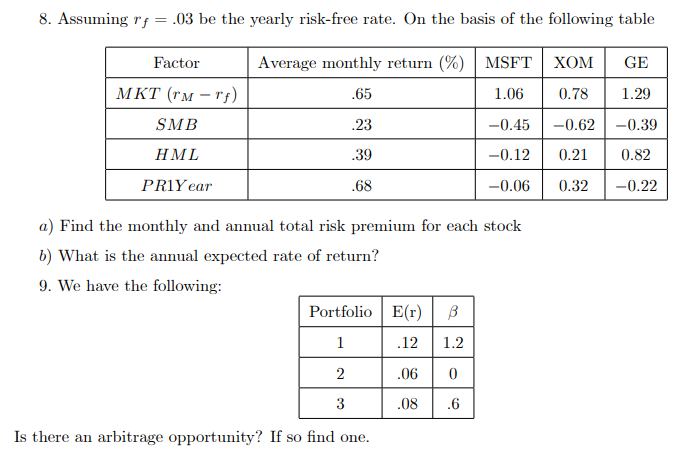

Question: step by step, no excel please 8. Assuming rf = .03 be the yearly risk-free rate. On the basis of the following table Factor MKT

step by step, no excel please

8. Assuming rf = .03 be the yearly risk-free rate. On the basis of the following table Factor MKT (rm -rf) SMB GE 1.29 .65 Average monthly return (%) MSFT 1.06 -0.45 39 -0.12 .68 -0.06 XOM 0.78 -0.62 0.21 0.32 -0.39 0.82 HML PRIY ear -0.22 a) Find the monthly and annual total risk premium for each stock b) What is the annual expected rate of return? 9. We have the following: Portfolio E(r) B | .12 1.2 .06 0 .08 .6 Is there an arbitrage opportunity? If so find one. 8. Assuming rf = .03 be the yearly risk-free rate. On the basis of the following table Factor MKT (rm -rf) SMB GE 1.29 .65 Average monthly return (%) MSFT 1.06 -0.45 39 -0.12 .68 -0.06 XOM 0.78 -0.62 0.21 0.32 -0.39 0.82 HML PRIY ear -0.22 a) Find the monthly and annual total risk premium for each stock b) What is the annual expected rate of return? 9. We have the following: Portfolio E(r) B | .12 1.2 .06 0 .08 .6 Is there an arbitrage opportunity? If so find one

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts