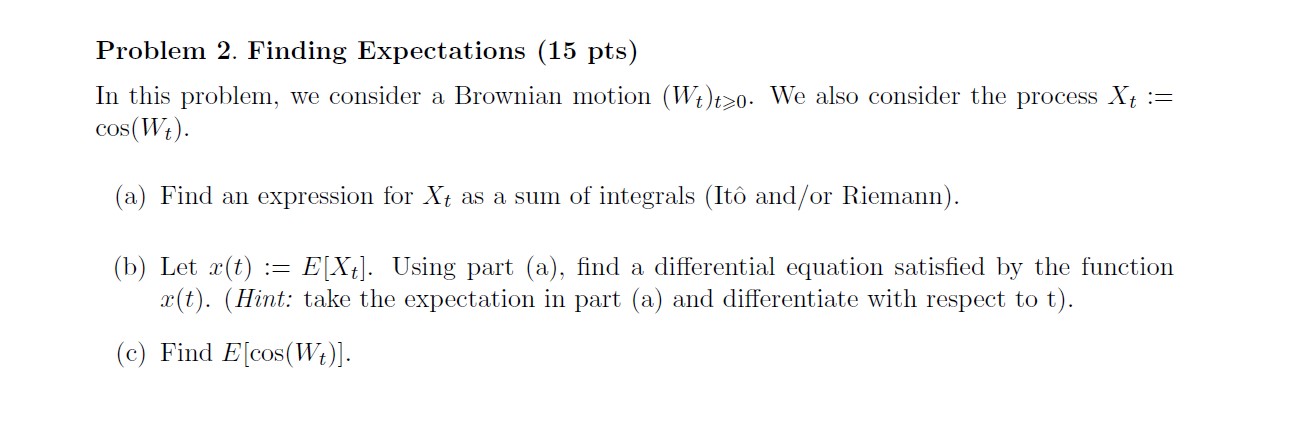

Question: Stochastic calculus, brownian motions, ito integral Problem 2. Finding Expectations (15 pts) In this problem, we consider a Brownian motion (Wt)tzo. We also consider the

Stochastic calculus, brownian motions, ito integral

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock