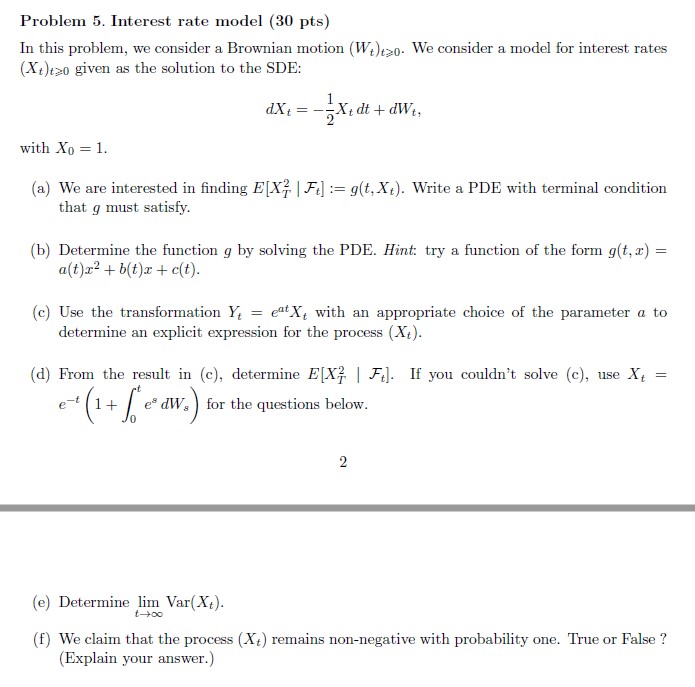

Question: Stochastic calculus Problem 5. Interest rate model (30 pts) In this problem, we consider a Brownian motion (Wt)(20. We consider a model for interest rates

Stochastic calculus

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

To solve these problems lets break them down step by step a Formulating the PDE Since gt Xt mathbbEX... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock