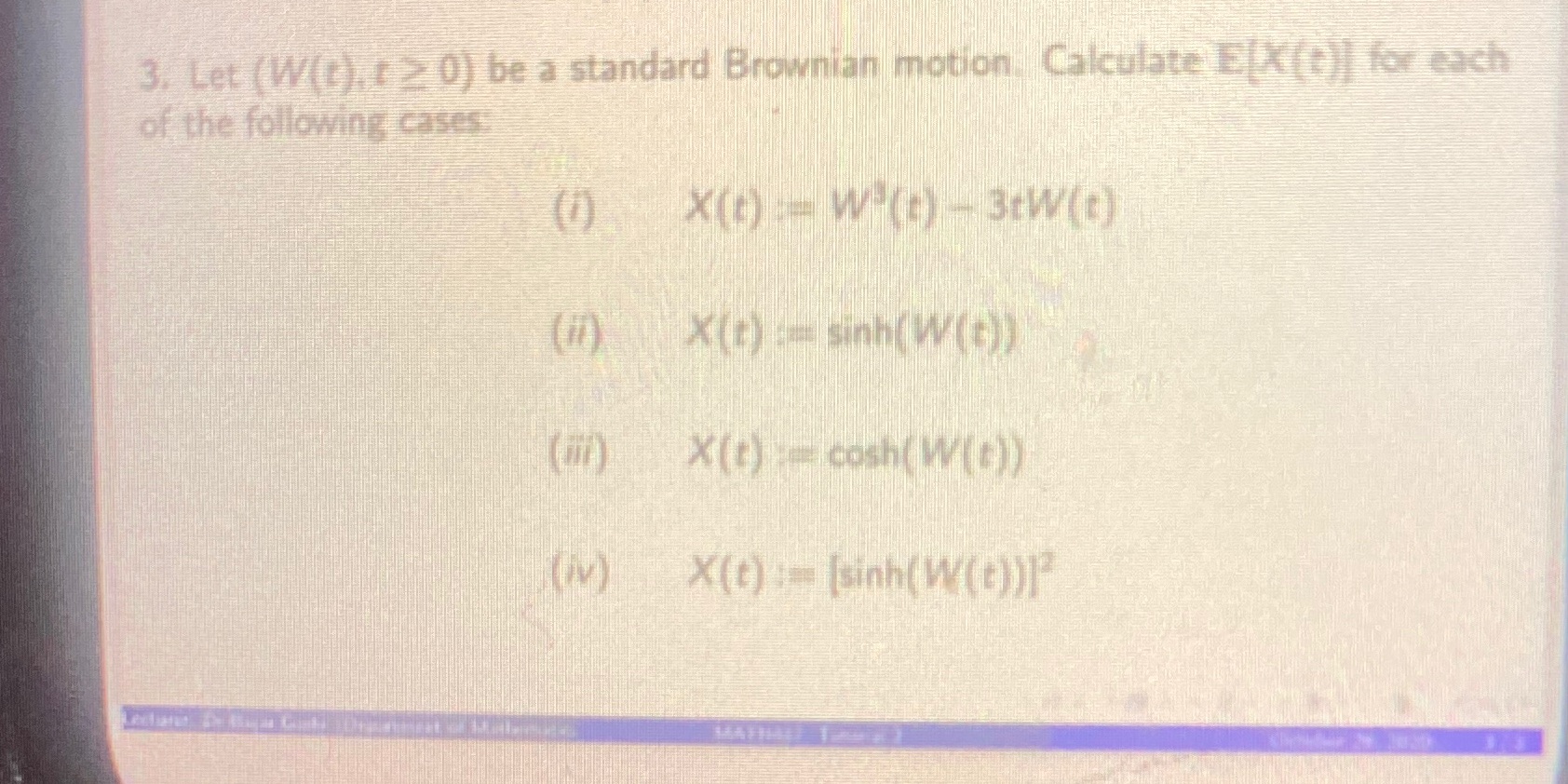

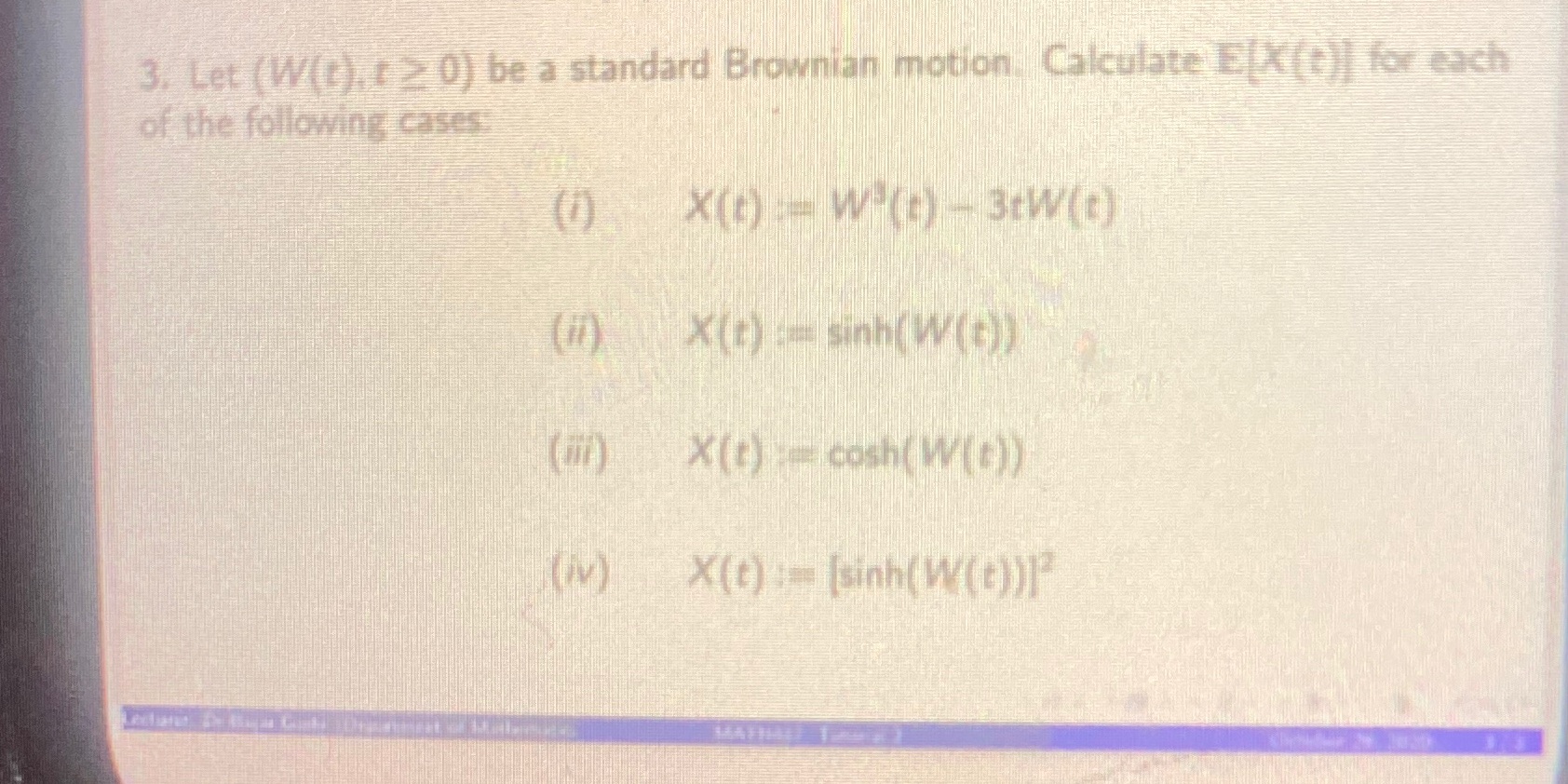

Question: Stochastic modelling in finance 3. Let (W(t), r > 0) be a standard Brownian motion. Calculate E X (t)) for each of the following cases

Stochastic modelling in finance

3. Let (W(t), r > 0) be a standard Brownian motion. Calculate E X (t)) for each of the following cases (1) X(0) = W ()- 3:W() (i1) X(+) : sinh (W(5) (in) X(t) - cosh (W(t)) (IV) X(t) = [sinh (W())P

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock