Question: Stochastic process problem, thank you! (12 points) Let pe (0, 1) and q = 1 -p. Consider the stochastic matrix P = p (] D

Stochastic process problem, thank you!

![q = 1 -p. Consider the stochastic matrix P = p (]](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2024/10/67084f211cda9_79367084f210c5df.jpg)

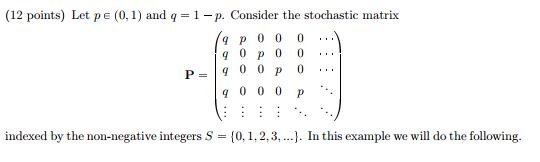

(12 points) Let pe (0, 1) and q = 1 -p. Consider the stochastic matrix P = p (] D indexed by the non-negative integers S = (0. 1. 2,3. ...). In this example we will do the following.(a) Show P is irreducible and aperiodic. (b) Show that P is positive recurrent and find E;[p;] for every je S. (c) Consider watching a (stationary discrete time Markov chain) process evolve with transition matrix P. Approximate the probability that, after watching for a long time, the process is in state 3. Does the answer depend on how the process was initially distributed over the states in S

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock