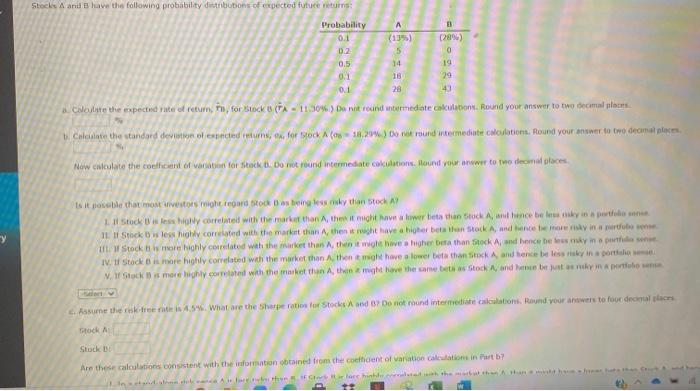

Question: Stocks and have the following probability danbons expected future returns: A (135) 5 Probability 0.1 D.2 0.5 0.1 01 14 (289) 0 19 79 43

Stocks and have the following probability danbons expected future returns: A (135) 5 Probability 0.1 D.2 0.5 0.1 01 14 (289) 0 19 79 43 18 28 a colate the expected as a resum, in for Stock B (A - 1990%) Do not round untermediate cakulation. Round your answer to two decimal places 1. Caleate the standard deviation of canced returns for stock (18) no round wrtermediate collation. Round your answer to two decimal places Now weate the concert of variation for steckt. Do root round Intermediate cakulations. Sound your answer to two decal places Is it possible that movestors might regardstock being less than stock 1. Il Stock less holy correlated with the market than then it might have a lower bets the Stock and hence been in a persona IL I Stock less highly correlated with the market than A, then it might have a higher beathan Stock A, and one more info Stock is more highly correlated with the market than then it wat have higher beathan Stock A, and hence bebes my in the IV. If Stock is more highly correlated with the market than then it molt have a lower breathan Stock A and hence be less riski portal Stock is more highly correlated with the market than the might have the same taas Stock A, and hence to per Assume the rise is 4.5%. What are the sharperiod for Stocks and B? Do not round intermediate calculations. Round your answers to four decimal places Stock Stock Are these calculations consistent with the formation obtained from the coefficient of waration calculation in Part 7

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts