Question: Straddle Practice Problem Consider a stock worth ( $ 4 9 ) . A call with an exercise price of (

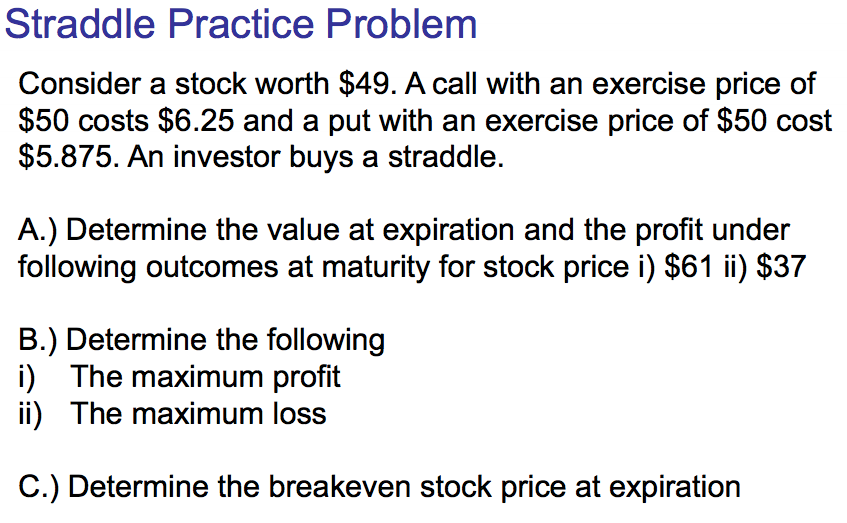

Straddle Practice Problem Consider a stock worth $ A call with an exercise price of $ costs $ and a put with an exercise price of $ cost $ An investor buys a straddle. A Determine the value at expiration and the profit under following outcomes at maturity for stock price i$ ii$ B Determine the following i The maximum profit ii The maximum loss C Determine the breakeven stock price at expiration

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock