Question: summarize (only the main or important point) the lesson (each point) below and briefly explain it in a simple way, easy to understand and if

summarize (only the main or important point) the lesson (each point) below and briefly explain it in a simple way, easy to understand and if it has formula please put it too.

Value Drivers

Financial managers sometimes refer to the basic determinants of an investment's cash flows and, consequently, its performance-as value drivers. For example, a key value driver for a manufacturing firm would be its inventory turnover because high inventory turnover ratios indicate the efficient use of the firm's investment in inventories. Identification of an investment's value drivers is crucial to the success of an investment project because it allows the financial manager to:

Allocate more time and money toward refining forecasts of these key variables.

Monitor the key value drivers throughout the life of the project, so corrective action can be taken in the event that the project does not function as planned.

Value drivers for investment cash flows consist of the fundamental determinants of project revenues (e.g., market size, market share, and unit price) and costs (e.g., variable costs and cash fixed costs, which exclude depreciation expense).

Sensitivity Analysis

When conducting a sensitivity analysis, a financial manager evaluates the effect of each value driver on the investment's NPV. To illustrate the use of sensitivity analysis as a tool of risk analysis, consider the investment opportunity faced by Longhorn Enterprises, Inc., which has the opportunity to manufacture and sell a novelty third brake light for automobiles. The light, which

is mounted in the rear window of an automobile to replace the factory-installed third brake light can be shaped into the logos of university mascots or other preferred symbols. Producing the light requires an initial investment of $500,000 in manufacturing equipment, which depreciates over a five-year time period toward a $50,000 salvage value, plus an investment of $20.000 in net operating working capital (the increase in receivables and inventory less the increase in accounts payable).

The discount rate used to analyze the project cash flows is 10 percent. This rate, as we will discuss in Chapter 14 when we

discuss the cost of capital, is the opportunity cost of investing in the proposed investment and should reflect the risk of the investment. We can summarize other pertinent information for the investment opportunity as follows:

Initial cost of equipment

$(500,000)

Project and equipment life

5 years

Salvage value of equipment

$ 50,000

Working-capital requirement

$ 20,000

Depreciation method

Straight line

Depreciation expense

$ (90,000)

Discount

10%

Tax rate

30%

Longhorn's management estimates that it can sell 15,000 units per year for the next five years and expects to sell them for $200 each. Longhorn's management team has identified four key value drivers for the project: unit sales, price per unit, variable cost per unit, and cash fixed cost (that is, fixed cost other than depreciation) per year. The expected values for the value drivers, along with corresponding estimates for the best- and worst-case scenarios, are summarized as follows:

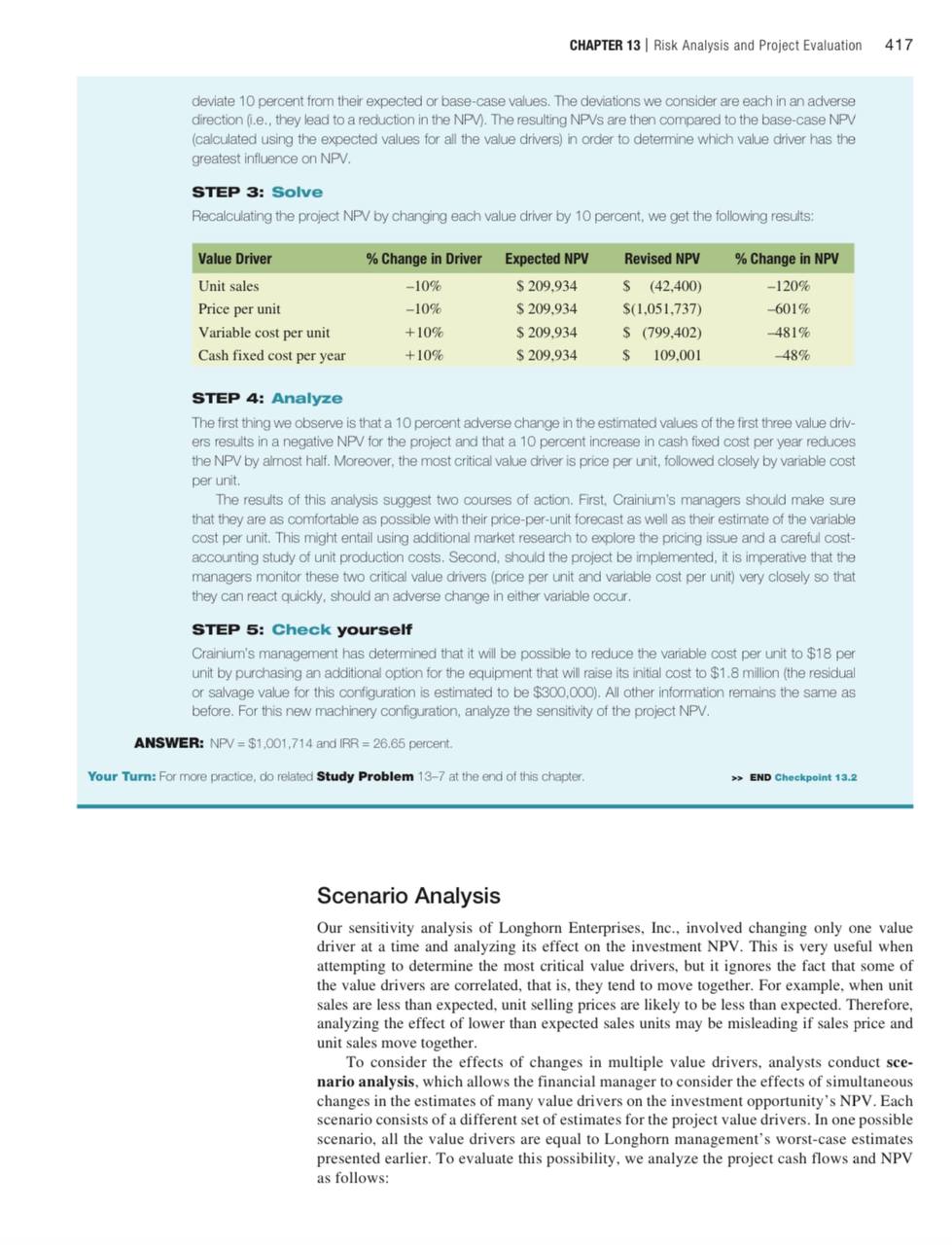

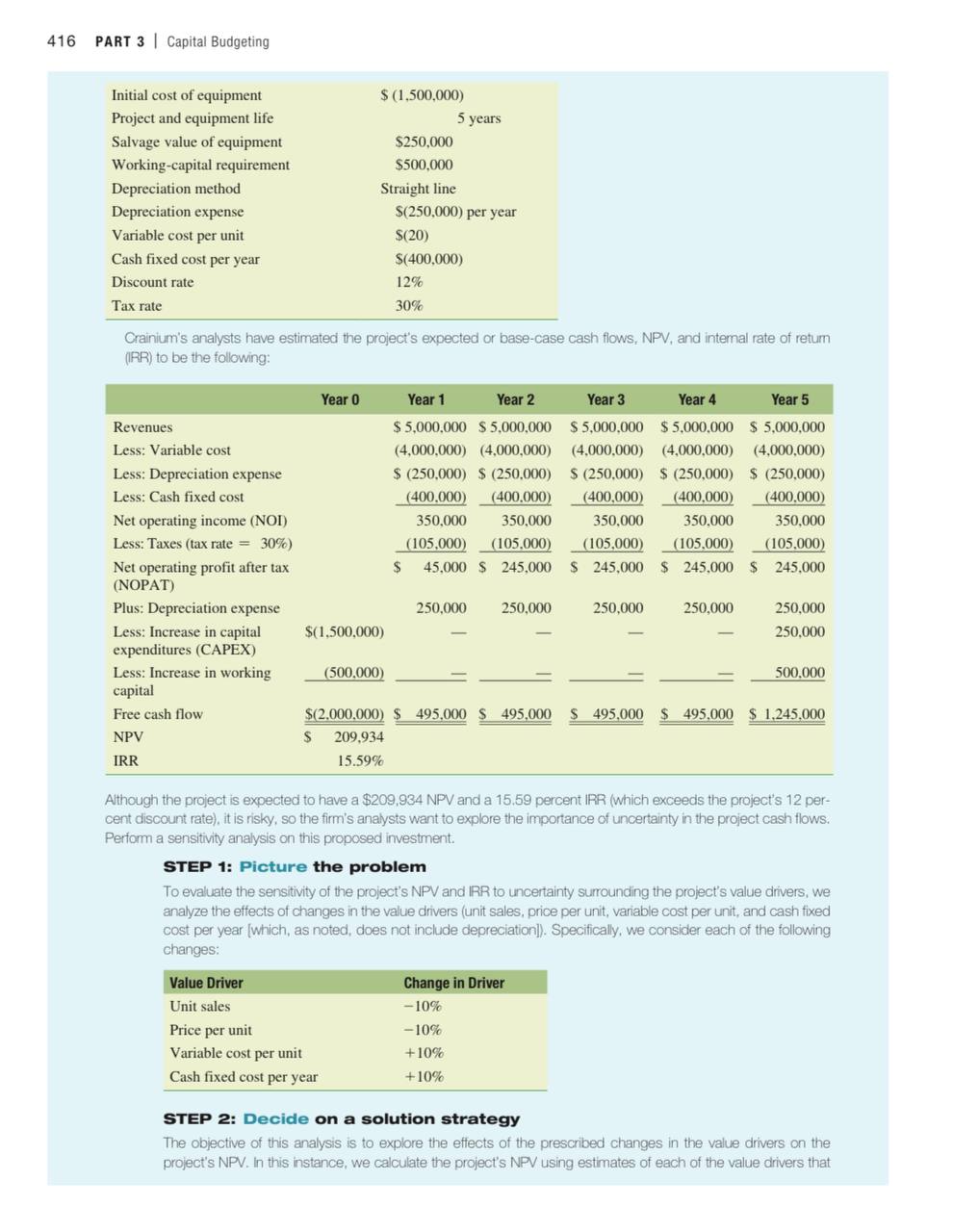

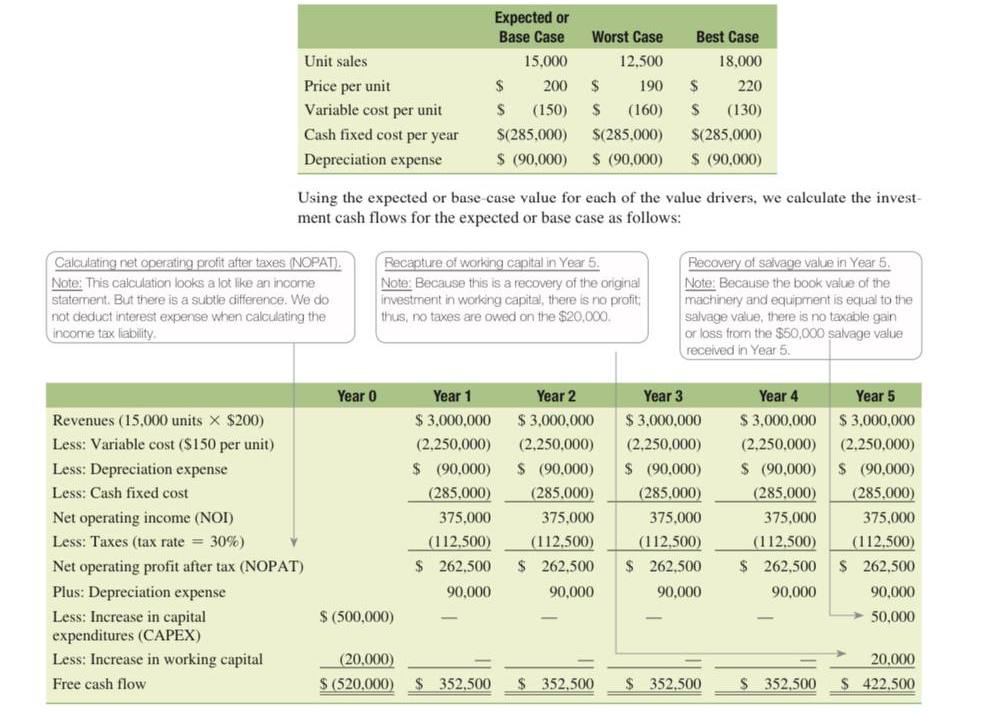

CHAPTER 13 | Risk Analysis and Project Evaluation 417 deviate 10 percent from their expected or base-case values. The deviations we consider are eachin an adverse direction (i.e., they lead to a reduction in the NPV). The resulting NPVs are then compared to the base-case NPV (calculated using the expected values for all the value drivers) in order to determine which value driver has the greatest influence on NPV, STEP 3: Solve Recalculating the project NPV by changing each value driver by 10 percent, we get the following results: Unit sales -10% $209,934 5 (42.400) -120% Price per unit -10% $209,934 $(1,051,737) 601% Variable cost per unit +10% $ 209,934 $ (799.402) 481% Cash fixed cost per year +10% $ 209,934 5 109,001 48% STEP 4: Analyze The first thing we cbsenve is that a 10 percent adverse change in the estimated values of the first three value driv- ers results in a negative NPV for the project and that a 10 percent increase in cash fixed cost per year reduces the NPV by aimost half. Maoreover, the most critical value driver is price per unit, followed closely by vanable cost per unit, The results of this analysis suggest two courses of action, First, Crainium's managers should make sure that they are as comfortable as possible with their price-per-unit forecast as well as their estimate of the variable cost per unit. This might entail using additional market research 1o explore the pricing issue and a careful cost- accounting study of unit production costs. Second, should the project be implemented, it is imperative that the managers monitor these two critical value drivers (price per unit and variable cost per unit) very closely so that they can react quickly, should an adverse change in either variable occur, STEP 5: Check yourself Crainium's management has determined that it will be possible to reduce the variable cost per unit to $18 per unit by purchasing an additional option for the equipment that will raise its initial cost 1o $1.8 million (the residual or salvage value for this configuration is estimated to be $300,000). All other information remains the same as before. For this new machinery configuration, analyze the sensitivity of the project NPV. ANSWER: NPV = 31,001,714 and IRR = 26.65 percent. Your Turn: For more practice, do related Study Problem 13-7 at the end of this chapler. END Checkpoint 13.2 Scenario Analysis Our sensitivity analysis of Longhorn Enterprises, Inc.. involved changing only one value driver at a time and analyzing its effect on the investment NPV. This is very useful when attempling to determine the most critical value drivers, but it ignores the fact that some of the value drivers are correlated, that is. they tend to move together. For example, when unit sales are less than expected, unit selling prices are likely to be less than expected. Therefore, analyzing the effect of lower than expected sales units may be misleading if sales price and unit sales move together. To consider the effects of changes in multiple value drivers, analysts conduct sce- nario analysis, which allows the financial manager 1o consider the effects of simultaneous changes in the estimates of many value drivers on the investment opportunity's NPV. Each scenario consists of a different set of estimates for the project value drivers. In one possible scenario, all the value drivers are equal to Longhorn management's worst-case estimates presented earlier. To evaluate this possibility, we analyze the project cash flows and NPV as follows: 416 PART 3 | Capital Budgeting Initial cost of equipment $ (1.500.,000) Project and equipment life 5 years Salvage value of equipment $250,000 Working-capital requirement $500,000 Depreciation method Straight line Depreciation expense $(250,000) per year Variable cost per unit $(20) Cash fixed cost per year $(400,000) Discount rate 12% Tax rate 30% Crainium's analysts have estimated the project's expected or base-case cash fiows, NPV, and internal rate of retum (IRR) to be the following: Revenues $ 5,000,000 $5.000,000 $5,000.000 5.000,000 $ 5000000 Less: Variable cost (4,000,000) (4,000,000) (4,000,000) (4,000,000) (4,000,000) Less: Depreciation expense $ (250,000) $ (250,000) 5 (250,000) % (250,000) $ (250.000) Less: Cash fixed cost (400.000) _ (400.,000) (400,000) (400,000) (400.,000) Net operating income (NOI) 350.000 350.000 350.000 350.000 350,000 Less: Taxes (tax rate = 30%) (105,000) (105.000) (105,000) (105.000) (105,000) Net operating profil after tax $ 45000 245000 245000 245000 $ 245,000 (NOPAT) Plus: Depreciation expense 250,000 250,000 250,000 250,000 250,000 Less: Increase in capital $(1.500.000) _ _ _ _ 250,000 expenditures (CAPEX) Less: Increase in working (500.000) 500.000 capital Free cash flow 2,000.000) 495000 495000 S 495000 S 495000 1,245.000 NPV $ 209934 IRR 15.59% Although the project is expacted to have a $209,934 NPV and a 15.59 percent IRR (which exceeds the project's 12 per- cent discount rate), it is risky, so the firm's analysts want to explore the importance of uncertainty in the project cash flows. Perform a sensitivity analysis on this proposed investment. STEP 1: Picture the problem To evaluate the sensitivity of the project's NPV and IRR to uncertainty surounding the project's value drivers, we analyze the effects of changes in the value drivers (unit sales, price per unit, vanable cost per unit, and cash fixed cost per year [which, as noted, does not include depreciation]). Specifically, we consider each of the following changes: Unit sales -10% Price per unit =10% Variable cost per unit +10% Cash fixed cost per year +10% STEP 2: Decide on a solution strategy The objective of this analysis is to explore the effects of the prescribed changes in the value drivers on the project's NPV. In this instance, we calculate the project's NPV using estimates of each of the value drivers that Expected or Base Case Worst Case Best Case Unit sales 15,000 12.500 18,000 Price per unit 200 $ 190 220 Variable cost per unit (150) (160) (130) Cash fixed cost per year $(285,000) $(285.000) $(285,000) Depreciation expense $ (90,000) $ (90,000) $ (90,000) Using the expected or base case value for each of the value drivers, we calculate the invest- ment cash flows for the expected or base case as follows: Calculating net operating profit after taxes (NOPAT). Recapture of working capital in Year 5. Recovery of salvage value in Year 5. Note: This calculation looks a lot like an income Note: Because this is a recovery of the original Note: Because the book value of the statement. But there is a subtle difference. We do investment in working capital, there is no profit; machinery and equipment is equal to the not deduct interest expense when calculating the thus, no taxes are owed on the $20,000. salvage value, there is no taxable gain income tax liability. or loss from the $50,000 salvage value received in Year 5. Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Revenues (15,000 units X $200) $ 3.000,000 $ 3,000,000 $ 3.000,000 $ 3,000,000 $ 3.000,000 Less: Variable cost ($150 per unit) (2.250.000) (2.250,000) (2,250,000) (2,250.000) (2.250,000) Less: Depreciation expense $ (90.000) $ (90,000) $ (90,000) $ (90,000) $ (90,000) Less: Cash fixed cost (285.000) (285.000) (285,000) (285.000) (285.000) Net operating income (NOT) 375,000 375.000 375.000 375.000 375.000 Less: Taxes (tax rate = 30%) (112.500) (112.500) (112,500) (1 12.500) (112.500) Net operating profit after tax (NOPAT) $ 262,500 $ 262.500 $ 262.500 $ 262.500 $ 262.500 Plus: Depreciation expense 90.000 90.000 90.000 90,000 90.000 Less: Increase in capital $ (500.000) 50,000 expenditures (CAPEX) Less: Increase in working capital (20.000) 20,000 Free cash flow $ (520.000) $ 352,500 $ 352.500 $ 352.500 $ 352.500 $ 422,500

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!