Suppose a Financial Institution has a portfolio which consists of +240 pounds(+ means long) of Copper and

Fantastic news! We've Found the answer you've been seeking!

Question:

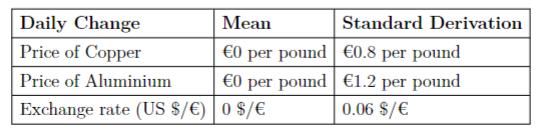

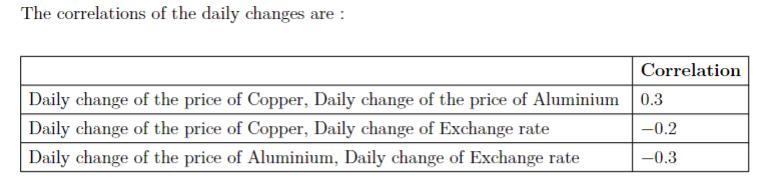

Suppose a Financial Institution has a portfolio which consists of +240 pounds(+ means long) of Copper and -135 pounds(negative means short) of Aluminium. The prices of Copper and Aluminium are both denominated in Euro(€). The current price of Copper and Aluminium are €210 per pound and €195 per pound respectively. The current exchange rate between Euro and US is 1.20 $/€. The daily change of the price of Copper, the price of Aluminium, and the exchange rate($/€), follows the normal distribution, the means and standard deviations are as follows:

Using the RiskMetrics model, find the 99% DEAR of the portfolio in USD.

Expert Answer:

The Daily Earnings at Risk DEAR for a portfolio in the RiskMetrics model is typically calculated as DEAR ValueatRisk VaR z Standard Deviation of the Portfolio where z is the zscore corresponding to th... View the full answer

Related Book For

Posted Date: