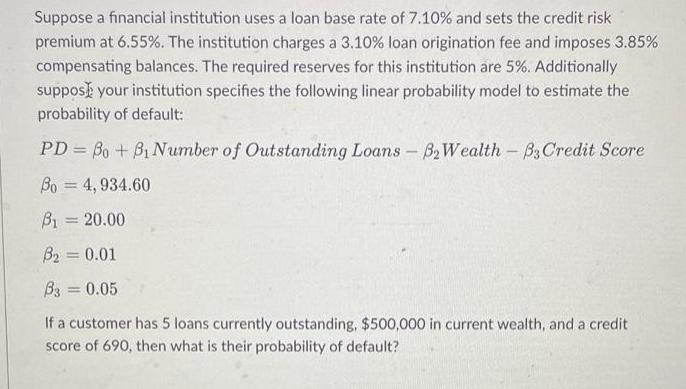

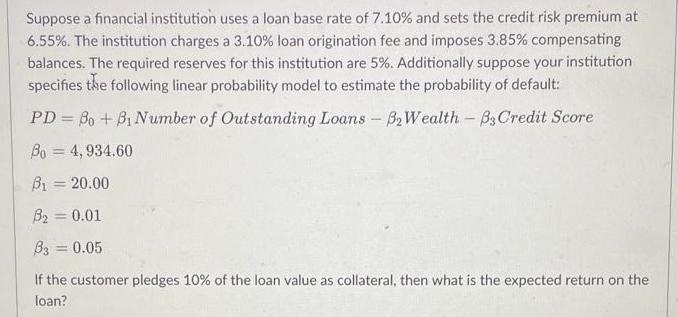

Suppose a financial institution uses a loan base rate of 7.10% and sets the credit risk...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To calculate the probability of default PD we can use the linear probability model specified PD Bo B ... View the full answer

Related Book For

Posted Date: