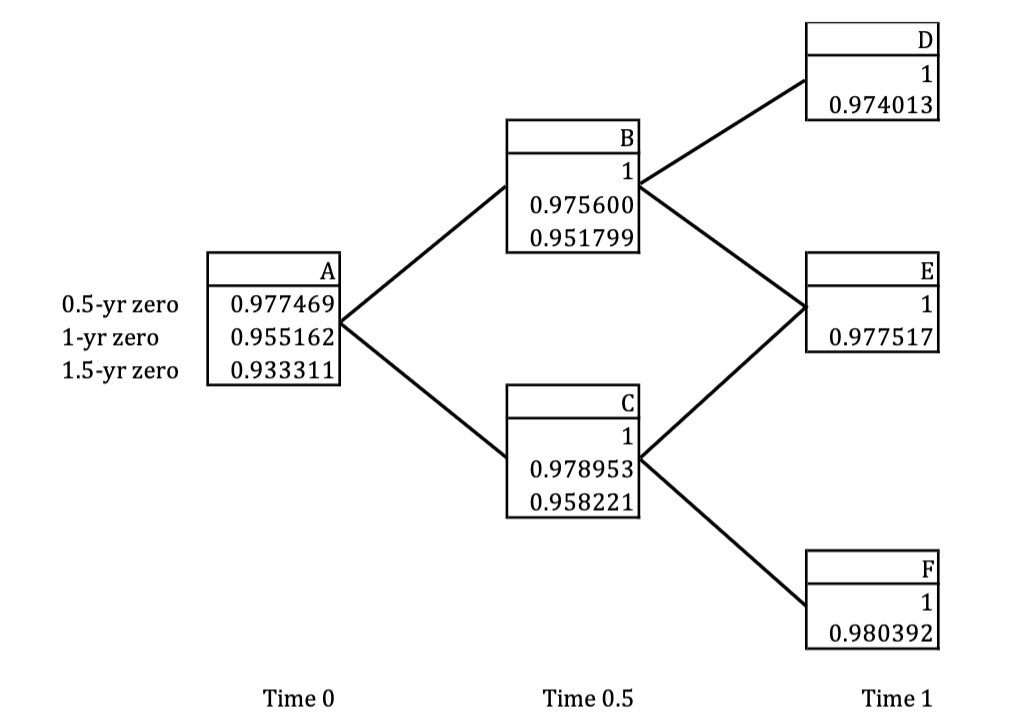

Question: Suppose a put option with 1 - year maturity on a $ 1 , 0 0 0 par, 1 . 5 - year zero coupon

Suppose a put option with year maturity on a $ par, year zero coupon bond is to be valued using the bondpricing tree below. This put option has a strike price of $

A What are the payoffs of the put option at nodes D E and F

B What are the riskneutral probabilities for the up and the down states implied by the prices of the zerocoupon bonds between time and

C What are the riskneutral probabilities for the up and the down states implied by the prices of the zerocoupon bonds between time and

D Using the riskneutral probabilities, what are the values of the put option at nodes B and C

E Using the riskneutral probabilities, what is the value of the put option at node A Time

Time

Time

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock