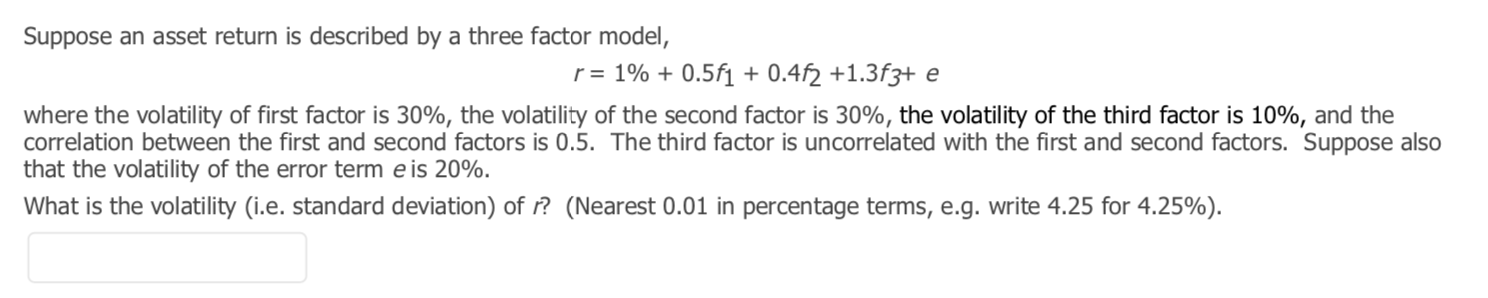

Question: Suppose an asset return is described by a three factor model, r = 1% + 0.5f1 + 0.462 +1.3f3+ e where the volatility of first

Suppose an asset return is described by a three factor model, r = 1% + 0.5f1 + 0.462 +1.3f3+ e where the volatility of first factor is 30%, the volatility of the second factor is 30%, the volatility of the third factor is 10%, and the correlation between the first and second factors is 0.5. The third factor is uncorrelated with the first and second factors. Suppose also that the volatility of the error term eis 20%. What is the volatility (i.e. standard deviation) of r? (Nearest 0.01 in percentage terms, e.g. write 4.25 for 4.25%)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock