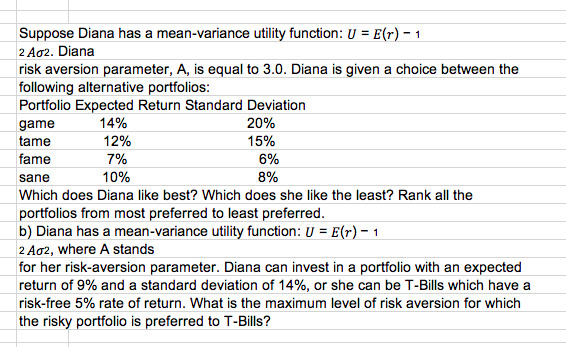

Question: Suppose Diana has a mean - variance utility function: U = E ( r ) - 1 2 A 2 . Diana risk aversion parameter,

Suppose Diana has a meanvariance utility function:

Diana

risk aversion parameter, is equal to Diana is given a choice between the

following alternative portfolios:

Portfolio Expected Return Standard Deviation

Which does Diana like best? Which does she like the least? Rank all the

portfolios from most preferred to least preferred.

b Diana has a meanvariance utility function:

where A stands

for her riskaversion parameter. Diana can invest in a portfolio with an expected

return of and a standard deviation of or she can be TBills which have a

riskfree rate of return. What is the maximum level of risk aversion for which

the risky portfolio is preferred to TBil

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock