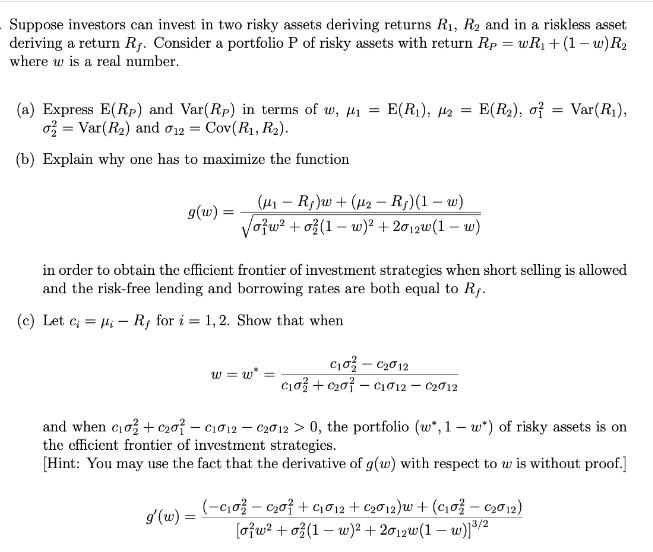

Suppose investors can invest in two risky assets deriving returns R, R2 and in a riskless...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a Expressions for ERp and VarRp in terms of w ER1 ER2 VarR1 VarR2 and CovR1 R2 Expected return of portfolio ... View the full answer

Related Book For

Posted Date: